Deutschland ist am weitesten in Richtung Japan

Erneut zitiere ich aus dem unentgeltlichen Newsletter der herausragenden John Authers von Bloomberg. Ich wollte das eigentlich eine Zeit lang nicht tun, auch um mich nicht bei Bloomberg unbeliebt zu machen. Aber er ist einfach so gut, dass ich ihn dennoch wieder zitiere. Diesmal weil er aufzeigt, wie sehr wir in Deutschland auf dem Weg in das “japanische Szenario” sind. Das ist

- interessant, weil andere wie zum Beispiel die Deutsche Bank in ihrer ausführlichen Studie die wir hier besprochen haben, eher Italien als Beispiel für die “Japanisierung” sehen. → Folgt Europa Japan in das deflationäre Szenario (I)?

- gefährlich, weil damit das Märchen vom reichen Land platzt.

- noch gefährlicher, weil der Euro damit massiv unter Druck kommt.

Doch schauen wir es uns an:

- “Germany(s) problem is now so extreme that before long Japan might have to start worrying about turning German. (…) the savage move in the bond market the last few months has pushed yields on German bunds not only significantly below JGBs for the first time, but significantly lower than JGB yields have ever been.” – bto: Wo war eigentlich der Aufschrei hierzulande? Klarer kann man nicht zeigen, wie sehr wir uns in Deutschland in eine Situation gebracht haben, die sehr gefährlich ist. Es drohen massive Vermögensverluste und soziale Konflikte.

Quelle: Bloomberg

- “Very disappointing data on German economic growth has acted as the most direct catalyst for the buying of long-dated U.S. Treasuries that briefly caused an inversion of the U.S. yield curve, with the 10-year yields falling below two-year yields for the first time in 12 years. (…) And virtually unnoticed amid the excitement, the 3-month/10-year curve in Germany also inverted.” – bto: Na ja, dass wir in einer Rezession stecken ist ja auch klar. Die Ausstrahlung geht natürlich weiter. Euro-Zonen-Bewohner flüchten aus verschiedensten Gründen in die deutschen Anleihen (Bonität, Eurozonen-Zerfall-Risiko) und drücken damit die Renditen. Danach dann die Flucht in den besten Schuldner der Welt (Waffen), der dazu auch noch positive Nominalzinsen zahlt. Logisch.

Quelle: Bloomberg

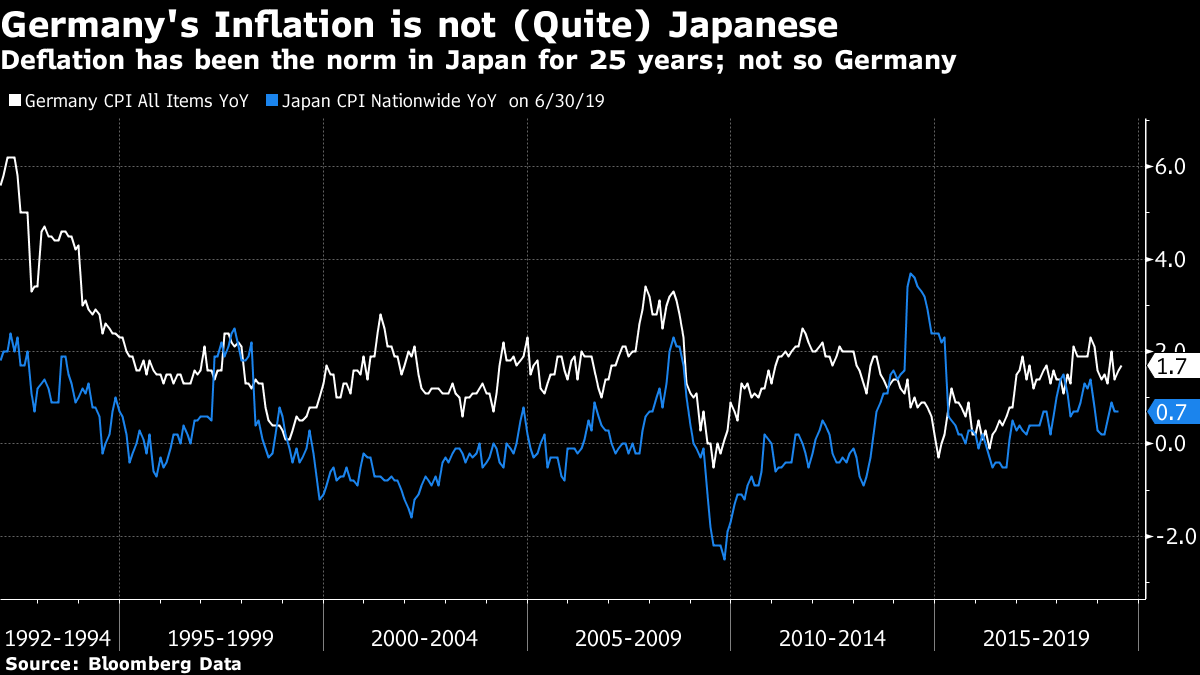

- “(…) it is worth looking at what exactly is ailing Germany and whether it really is similar to Japan. Both are large exporting nations that enjoyed quasi-miraculous growth after the second world war, and now have challenging demographics with an aging population. But while outright deflation (an actual sustained drop in consumer prices over time) has become a fact of life in Japan, German inflation has remained above zero (…).” – bto: Und das wohl dank des Euro. Ja, denn damit wurde ein deutlicher Anstieg der Deutschen Mark verhindert, die über sinkende Importpreise zu Deflation geführt hätte. Einen Vorteil hatte der Euro dann doch.

Quelle: Bloomberg

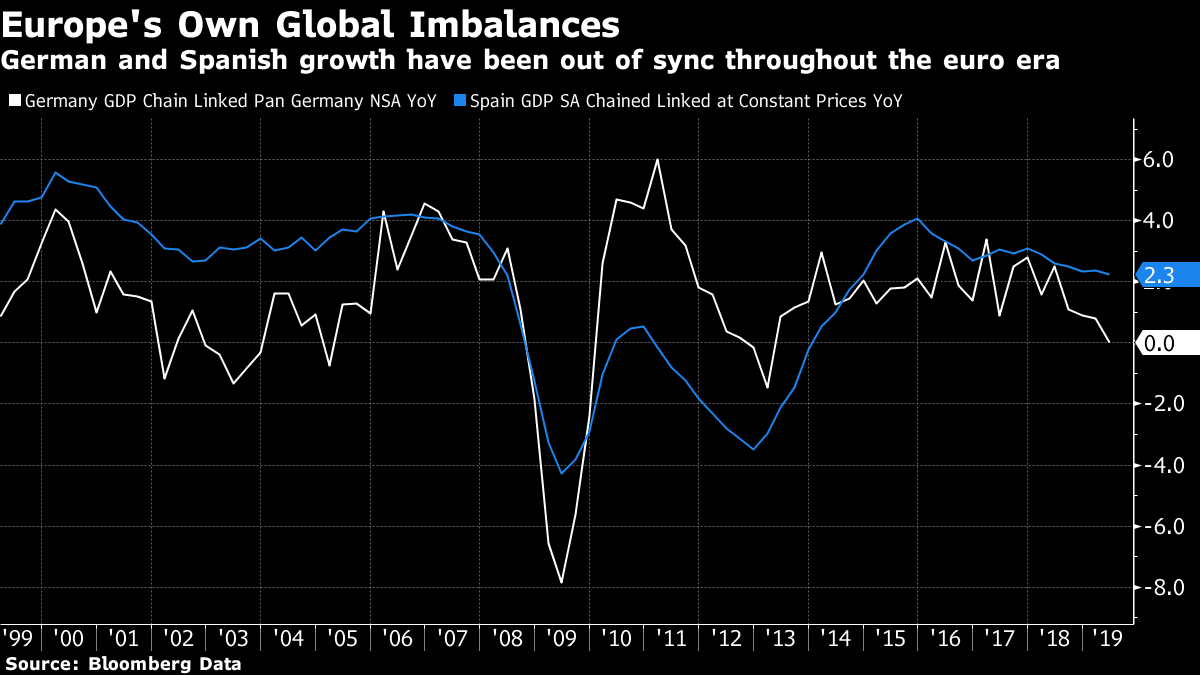

- “So the market sees Japanification coming, but Japanification is not yet an established fact in Germany.(…) Meanwhile, expectations for the future are dropping sharply, and are the lowest since the worst of the sovereign debt crisis in 2011. (…) its economy is out of sync with those of countries on the euro zone’s periphery. Before the global financial crisis, Spain was growing healthily and might have benefited from higher interest rates; Germany was growing more weakly. As one monetary policy had to fit all, Spain benefited from low rates aimed at Germany, and enjoyed an epic construction boom that would inflict a severe and enduring recession once the bubble burst.” – bto: Das stimmt und zeige ich übrigens auch in meinem Bilderbuch: “Die Krise … “. Und wie Leser von bto wissen, haben sich die Unterschiede zwischen den einzelnen Mitgliedsländern der Eurozone in den letzten Jahren vergrößert, nicht verkleinert!

Quelle: Bloomberg

- “A further problem (…) is its banking system. Europe’s banks were far more bloated and over-leveraged than their U.S. counterparts when the crisis hit. This has left them with a legacy of de-leveraging that has hurt their ability to lend. Banks remains far more central to financing businesses and people in Europe than they are in the U.S., so this matters greatly. (…) Weak banks imply a weak economy. That means investors will have less trust in the strength of banks’ balance sheets, so they will bid down the share price to trade at a lower multiple to the official book value of assets. That makes it harder for banks to raise equity financing. And as weak banks also diminish confidence in an economy, this causes the yield curve to flatten, and a flatter or inverted yield curve makes it harder for banks to generate profits. (…) The net effect is to make it harder for Europe or Germany to escape Japanification.” – bto: Auch diese Logik ist mittlerweile Allgemeingut – wird aber von den hiesigen Entscheidungsträgern verdrängt, während man sich mit allen anderen “wichtigen” Themen beschäftigt …

Quelle: Bloomberg

- “In one crucial respect, the American response to the Global Financial Crisis worked better than that of Europe. U.S. banks could be re-capitalized, and to the surprise of many that actually happened. In Europe, re-capitalization was harder, and the sovereign debt crisis brought on by the imbalances in the euro zone made it even harder. As a result, the European banking system has Japanified (…).” – bto: Und damit sind wir in einer verdammt schweren Situation, aus der es eben keinen einfachen Ausweg gibt.

Quelle: Bloomberg, Capital Economics

- “Immediately after the crisis, European banks commanded a slight premium, in terms of price-to-book multiples. That has steadily turned into a crushing discount.” – bto: Auch das leuchtet ein. Niemand, der einigermaßen bei Verstand ist, kann Aktien von Banken in Europa halten!

Quelle: Bloomberg

- “If ever there were a time to resort to fiscal stimulus, this is it. More German spending might ease the difficulties of keeping the countries of the euro zone together. And the market is making it easy for Germany to do. (…) The problem is that Germany is maddeningly averse to fiscal stimulus,(…)” – bto: Den Ruf nach mehr Staatsausgaben kennen wir ja schon. Japan fährt übrigens auch seit Jahren große Defizite ohne entsprechende Wirkung.

- “When sentiment is this weak, negative yields, flat yield curves and distrusted banks combine to make it almost impossible for the economy to turn around. (…) for the time being it is turning Germany Japanese. And that, in turn, becomes an issue for the rest of the world.” – bto: vor allem erstmal die Eurozone, die das nicht überleben wird.