Referendum vorbei – Krise bleibt

Nun haben die Italiener abgestimmt. Kurz- und mittelfristig dürften sich die Konsequenzen in Grenzen halten, egal wie die Finanzmärkte heute auch reagieren. Bekanntlich denke ich, das dürfte das Leiden verlängern, weil nun die Regeln gelockert werden und Europa alles tun wird, um die Stimmung in Italien zu bessern.

Nüchtern bleiben jedoch die Fakten, die deutlich zeigen, dass Italien eben nicht dauerhaft im Euro überleben kann. Nur zur Auffrischung: die Argumente von Ambroise Evans-Pritchard im Telegraph:

- “The moment of real danger for Italy will come as soon as the European Central Bank starts to taper bond purchases, or even hints at a change in course.” – bto: weil dann nämlich die Zinsen steigen (könnten!).

- “Italy’s problems never went away. They were disguised by quantitative easing and the artificial suppression of borrowing costs. The ECB’s €80bn purchases each month jammed the signalling system for sovereign credit risk.” – bto: natürlich nicht. Solange jedoch die Pleite des Landes ausgeschlossen wird, wären die Zinsen auch ohne EZB recht tief im heutigen Umfeld.

- “But even this has not been enough to stop the risk spread on Italian 10-year yields rising for several months as the banking crisis deepens, hitting a two-year high of 192 basis points earlier this week.” – bto: was aber mit einer allgemeinen Marktreaktion zu tun hat.

Quelle: IL SOLE, The Telegraph

- “The global reflation shock since the election of Donald Trump is bringing matters to a head faster than anybody could have imagined weeks ago. Italian borrowing costs have risen in lockstep with US Treasury yields, even though Italy is not reflating at all and is certainly not about to enjoy a fiscal shot in the arm.” – bto: Das stimmt. Es sind simpel nur höhere Zinsen für einen bankrotten Schuldner. Unangenehm.

- “Its banks own €400bn of Italian government bonds and these are suddenly worth less. (…) It is our old friend the ‘doom loop’. The banking crisis is driving up sovereign bond yields, and higher yields are in turn driving the banks into deeper trouble.” – bto: ein wirklicher Teufelskreislauf. Beide stützen sich gegenseitig oder ziehen sich in den Abgrund, je wie man es sehen will.

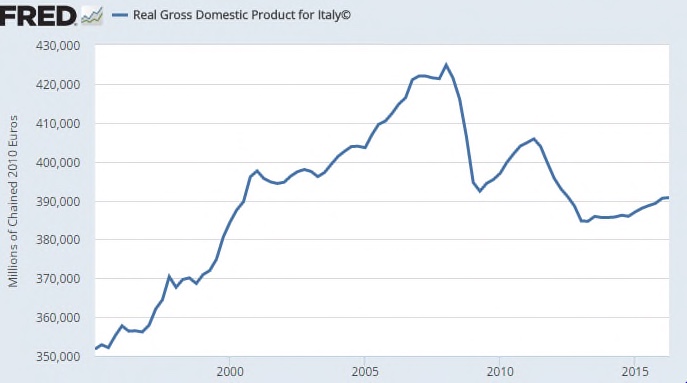

- “The country is stuck in a depressionary debt trap. Trend growth is below zero. GDP is still 9pc below its pre-Lehman peak. Industrial output is back to levels reached thirty-five years ago. (…) No large developed country in modern times has ever suffered such a fate.” – bto: was beweist, wie mächtig das Konstrukt des Euro ist.

- “(…) a vicious cycle of labour hysteresis as economic stagnation and weak productivity reinforce each other. Its exchange rate is overvalued by 20-30pc against Germany.” – bto: eine Lücke, die Italien nicht wird schließen können. Wie auch?

Quelle: ST LOUIS FED, The Telegraph

- “Italy cannot now deflate its way back to viability since this shrinks the underlying base of nominal GDP and automatically steepens the debt trajectory. It is impossible task for a country with a public debt ratio of 133pc of GDP, and is self-defeating in mechanical terms.(…) There is no plausible way out for Italy within the current contractionary structure of monetary union. Only ECB bond purchases forever can keep the lid on this pressure cooker.” – bto: was aber nur die Symptome bereinigt, nicht eine Heilung bewirkt.

- “Yet it is patently obvious that QE is nearing political, legal, and technical limits. The ECB already faces a lapidary attack by Otmar Issing, (…) ‚The no bailout clause is violated every day‘, he said.” – bto: was ja auch stimmt. Aber ohne die EZB wäre der Euro schon längst Geschichte.

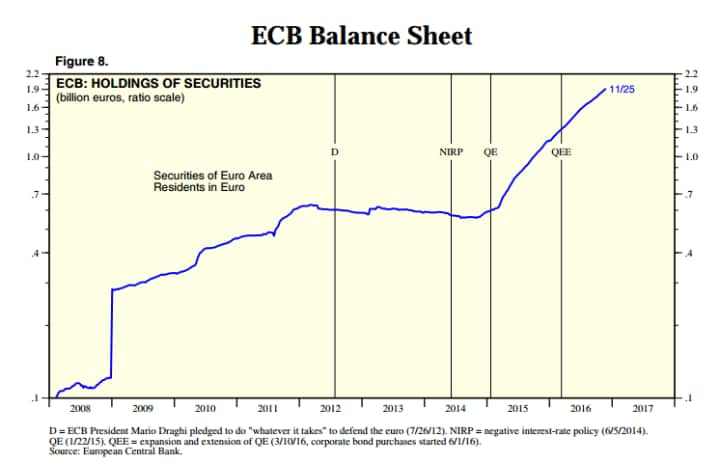

- “The ECB has so far bought €1.4 trillion of bonds. Its balance sheet will reach 35pc of eurozone GDP by the end of the year at the current torrid pace, much higher than it ever reached in the US.” – bto: ohne Wirkung auf die Realwirtschaft übrigens.

Quelle: YARDENI, The Telegraph

- “It invites the perennial question whether Italy, Portugal, and perhaps others, can fund themselves at all in the capital markets, given that the eurozone has done almost nothing since the debt crisis of 2011-2012 to put monetary union on workable foundations.” – bto: Tja, solange die Märkte denken, irgendwer haut sie raus, wenn es hart auf hart kommt, ja.

- “There is still no fiscal union, no shared debt issuance, no banking union worth the name, and no expansionary New Deal to lift the economy off the reefs once and for all. All it has done is to tighten surveillance, hoping somehow that it can muddle through by riding on world demand.” – bto: eine Politik, an der die Gläubiger einen erheblichen Anteil haben.

- “The ECB’s Mario Draghi knows the dangers but he is caught in a Kulturkampf with the dominant power of Europe. Germans regard the experiment of QE and negative rates as a violation of the ‘Ordoliberal’ orthodoxies that anchor the nation’s post-War political and economic thinking.” – bto: Ich sehe die Risiken aus Deutschland nicht so. Im Wahljahr macht die Regierung alles, um die Illusion der Eurorettung aufrecht zu erhalten.

- “If Mario Draghi keeps pushing for more QE in this context, it will become almost impossible to silence criticism that his real objective is to hold down Italian yields and stave off the insolvency of his own country. Perhaps it is already impossible.” – bto: Auf jeden Fall liefert er populistischen Strömungen gute Argumente.

@ M. Stöcker

>Damit die Investition erfolgreich war, müssen über den Verkauf der Produkte/Dienstleistungen diese Ausgaben wieder eingespielt werden.>

Das bestreite ich nicht.

Was ich bestreite:

Dass ALLEIN hinreichende Nachfrage – EGAL, wie sie erreicht wird, sei es durch Helikoptergeld oder weitere Verschuldung – die Investitionen erfolgreich macht.

Mit diesem Ansatz läuft man früher oder später an die Wand, d. h. irgendwann wird die Nachfrage – das, was sich bedarfsbezogen durch sich frei entscheidenden Menschen an den Märkten als erwerben wollend manifestiert – NICHT mehr die Investitionen erfolgreich machen.

Dem entkommt man auch nicht durch eine Staatsnachfrage, die für den privaten Sektor als Nachfrager einspringt.

Man entkommt diesem Problem nur, wenn sich das Angebot ändernd ANPASST (selbstverständlich bei Aufrechterhaltung von Nachfrage) – oder durch eine „Nachfragediktatur“, die auf einem ganz anderen Wirtschaftssystem basiert.

Ich verstehe ja das Problem:

Anpassung des Angebots ist sehr viel schwieriger und mit härteren, destabilisierenden Konsequenzen verbunden als eine monetär induzierte Ausweitung der Nachfrage.

Daher verstehe ich auch nur zu gut, warum jetzt alle auf Fiskalpolitik setzen (unabhängig davon, dass natürlich bezüglich Infrastruktur etc. ein tatsächlicher Bedarf besteht).

Was ich kritisiere, ist das DAMIT verbundene Denken, nämlich:

Wir haben eine Lösung, z. B. Helikoptergeld. DAHER muss das Problem auch dort zu finden sein, wo Helikoptergeld etwas bewirken kann – bei der Nachfrage.

Das ist Kurzschlussdenken, genauso wie es ein Kurzschlussdenken ist, die Lösung an der Verteilungsproblematik aufzuhängen. Sie ist ein Problem, aber eines auf der zweiten oder dritten Ebene.

“Was ich bestreite:

Dass ALLEIN hinreichende Nachfrage – EGAL, wie sie erreicht wird, sei es durch Helikoptergeld oder weitere Verschuldung – die Investitionen erfolgreich macht.”

Völlig d’accord. Helikoptergeld ist in der aktuellen Situation eine notwendige, keinesfalls jedoch eine hinreichende Bedingung für erfolgreiche Investitionen und wirtschaftliche Entwicklung.

LG Michael Stöcker

Das italienische Drama in 30 Diagrammen: http://www.querschuesse.de/italien-so-siehts-wirtschaftlich-aktuell-aus/

LG Michael Stöcker

Richtig, DAS ist das italienische Drama.

Und was wird den Leuten erzählt?

Das hier von Meister Fricke für die gebildeten Stände:

http://www.spiegel.de/wirtschaft/service/referendum-in-italien-reformen-und-sparen-helfen-nicht-a-1124007.html

Die Krise bleibt, keine Frage; denn es handelt sich hierbei in aller erster Linie um eine Krise in unseren Köpfen. Die strukturellen Probleme im Süden (so schwerwiegend sie auch in manchen Ländern sind) , überdecken aber die eigentliche tiefer liegende systemische Krise (Das Problem hinter dem Problem). Mariana Mazzucato hat hierzu ein neues Buch herausgegeben: RETHINKING CAPITALISM mit Beiträgen von Stephanie Kelton, Andrew Haldane et. al. Zwei Vorträge von Kelton habe ich hier verlinkt, da sie meine Analysen zur Krise bestätigen. Das Paper zu einem der Vorträge beginnt mit: „What if They’re Both Wrong?“ Wir werden diese Krise nur überwinden, wenn wir die Krise in unserem Denken überwinden: https://zinsfehler.com/2016/12/01/das-kollektive-versagen/

LG Michael Stöcker

>Wir werden diese Krise nur überwinden, wenn wir die Krise in unserem Denken überwinden: https://zinsfehler.com/2016/12/01/das-kollektive-versagen/>

Gut, dann schauen wir uns einmal Ihr Denken an, wie in Ihrem Blog dokumentiert.

Da lese ich u. a.:

>Der Kapitalismus hängt in seiner Funktionalität aber ganz zentral an den Verkäufen. Denn nur Ausgaben erzeugen Einnahmen, die dann wieder Ausgaben erzeugen können. Am Anfang allen ökonomischen Handelns muss von daher immer zuerst die Ausgabe stehen.>

Mein Denken sagt mir:

Der Kapitalismus hängt in seiner Funktionalität ganz zentral an den Angeboten. Denn nur Angebote erzeugen Einnahmen, die wiederum Ausgaben erzeugen können. Am Anfang allen ökonomischen Handelns muss von daher immer zuerst das Angebot stehen.

Bewertung:

Beide Auffassungen sind kreislaufbezogen berechtigt.

Beide sind jedoch nur begrenzt richtig, d. h. jede für sich benennt NICHT HINREICHEND die Bedingungen für die Funktionalität des Kapitalismus, oder eingeschränkter: die für einen Ausgleich von Angebot und Nachfrage.

Denn sowohl von der Nachfrageseite wie von der Angebotsseite her gedacht als der jeweils nicht zu hinterfragenden PRIMÄREN Determinante, die man nur richtig adjustieren müsse, u. a. mit dem „richtigen“ Geldsystem, kann man in schwerwiegende Fehlallokationen laufen, mit der Folge, dass Angebot und Nachfrage nicht aufeinander treffen.

BEIDES muss immer wieder GLEICHBERECHTIGT gedacht werden.

Diese Erkenntnis, allein bei weitem nicht hinreichend die Dinge zum Besseren zu wenden, wäre wenigstens einmal ein Anfang, die „Krise in unserem Denken“ zu überwinden.

„BEIDES muss immer wieder GLEICHBERECHTIGT gedacht werden.“

Schon richtig, Herr Tischer; aber wo bleibt bei Ihrer Analyse das Geld und die Reihenfolge? Es ist der Bankkredit, der im Aggregat überhaupt erst ein solches Angebot ermöglicht; denn über den Bankkredit wird das Angebot vorfinanziert. Über diese Vorfinanzierung wird der Verkauf der Arbeitskraft überhaupt erst möglich. Diese investiven Ausgaben verwandeln sich sodann in die Einnahmen der Arbeitnehmer und in die Gewinne (Hinweis: auch Lagerinvestitionen erhöhen den Gewinn; interessiert aber die Bank nicht, denn die will in Cash bezahlt werden und nicht mit Oliven/Kühlschränken/….). Damit die Investition erfolgreich war, müssen über den Verkauf der Produkte/Dienstleistungen diese Ausgaben wieder eingespielt werden.

„Beide sind jedoch nur begrenzt richtig, d. h. jede für sich benennt NICHT HINREICHEND die Bedingungen für die Funktionalität des Kapitalismus, oder eingeschränkter: die für einen Ausgleich von Angebot und Nachfrage.“

Alle wichtigen aktuellen Indikatoren sprechen für ein globales Nachfrageproblem, das seine wesentliche Ursache in den nationalen und internationalen Disparitäten hat (Matthäus-Effekt): https://www.youtube.com/watch?v=sirXAfpIrao&t=2053s.

LG Michael Stöcker

Hier ist der Matthäus-Effekt mal grafisch aufbereitet: http://blog.tagesanzeiger.ch/nevermindthemarkets/index.php/40903/ungleiches-europa/. Insbesondere der Norden Italiens sticht hier besonders ins Auge und zählt somit neben GB und GR zu den größten Verlierern.

LG Michael Stöcker

Soweit, so schlecht und schlimm.

AEP:

>„The greatest danger for Itay is the looming loss of the ECB shield”>

Das ist richtig – auf der monetären Ebene.

Wenn die Zinsen, induziert von den Entwicklungen in USA, weiter anziehen – und zumindest im Augenblick spricht einiges dafür –, dann wird auch die EZB ihre Zinspolitik ändern müssen. Es käme dann unweigerlich zu Schocks auf den Euro-Kapitalmärkten. Für Italien wären die Folgen verheerend.

Die andere größte Gefahr für Italien kommt vom Verlust der politischen Stabilität.

Renzi, jung und dynamisch an der Macht gekommen, wollte Verschrotter des Systems sein. Jetzt ist er politisch krachend gescheitert selbst „Schrott“. Über kurz oder lang gibt es Neuwahlen. Es ist abzusehen, dass dies noch mehr Instabilität verheißt. Auch das kann Schocks auf den Finanzmärkten auslösen.

Unter allem lodert die Glut der nicht gelösten, nicht befriedend zu lösenden Bankenkrise des Landes.

Verallgemeinernd:

Die etablierten politischen Kräfte versuchen in den krisengeprägten Ländern mit „Hau ruck-Programmatik“ erforderliche Reformen durchzusetzen. In Italien ist das einmal mehr gescheitert. Wie es u. a. in Frankreich gelingen kann mit dem radikalen Thatcher-Liberalismus von Fillon („neues Betriebssystem für Frankreich“), ist mir absolut schleierhaft. Wertkonservative Kaschierung wird es nicht richten. Und halbherzig betriebene soziale Appeasement-Politik auch nicht. Sie wäre bei den fundamentalen Problemen kontraproduktiv.

Fazit:

Man hätte den Bevölkerungen viel früher viel mehr abverlangen müssen als geschehen ist, um das Unzufriedenheitspotenzial nicht so anschwellen zu lassen. Weil es in erster Linie um Systemstabilität der Eurozone ging (und nach Lage der Dinge auch gehen musste, um Extrem-Schocks zu vermeiden), kam es – quasi notwendigerweise – nicht zu den erforderlichen Bereinigungsprozessen, die auch innenpolitisch kaum durchzusetzen gewesen wären. Jetzt ist das Unzufriedenheitspotenzial offensichtlich nicht mehr einzufangen. Die Unsicherheit wächst, nichts ist mehr berechenbar.

Da ist es schon fast gespenstisch, wie das Ergebnis der österreichischen Präsidentenwahl gefeiert wird.

„Da ist es schon fast gespenstisch, wie das Ergebnis der österreichischen Präsidentenwahl gefeiert wird.“

Genau so habe ich das heute früh auch empfunden.

LG Michael Stöcker

Ja. “Gespenstisch” ist der richtige Ausdruck. Ich glaube darin sind sich die Leser hier alle einig.

“bto: Ich sehe die Risiken aus Deutschland nicht so.Im Wahljahr macht die Regierung alles, um die Illusion der Eurorettung aufrecht zu erhalten.”

So wird es sein und das Handeln der Bundesregierung wird von “tiefster Überzeugung” in die Richtigkeit ihres Handelns geprägt sein. Aber vielleicht wirft die Bundesregierung mal einen Blick hierhin:

“Der Euro liegt nicht in der DNA des Kontinents, sagt der Wirtschaftshistoriker Abelshauser. Flexible Wechselkurse und sanfte deutsche Geldvormacht sind aus seiner Sicht der bessere Weg für Europa. ”

https://www.welt.de/wirtschaft/article159951580/Wir-brauchen-den-Euro-nicht.html