Vorbereitung auf die Krise beginnt

Zeit, sich auf den nächsten Abschwung einzustellen –, denkt zumindest die OECD und recht hat die Organisation. Denn nicht nur bto-Leser wissen, dass der nächste Abschwung nur eine Frage der Zeit ist und unweigerlich deutlich machen wird, dass der Aufschwung eine Illusion war, eine teuer erkaufte mit immer mehr billigem Geld und neuen Schulden.

Doch was wäre zu tun? Martin Sandbu von der FT fasst die Aussagen der Institutionen zusammen:

- “The OECD’s Economic Outlook (…) generally say similar things (…) simply reflects professional economists’ mainstream analysis of the same data. But that makes it all the more valuable when original interpretations and policy conclusions appear — as they do in the latest OECD report (…).” – bto: Natürlich gibt es gute Berichte, gerade von der BIZ, die allerdings nicht richtig interpretiert und genutzt werden. Ich denke beispielsweise an die IWF-Studie, die zeigt, dass eine Transferunion in Europa nicht funktionieren kann.

- “The OECD is not alone, of course, in noticing a global economic slowdown. The organisation spots a number of warning signs that the global upswing that started in early 2016 stalled around the turn of 2018: global export orders, industrial production, retail sales volumes and container port traffic all exhibit the same pattern, markedly decelerating for the past three or four quarters after accelerating strongly during the two previous years.” – bto: So ist es, die Börsen spiegeln diesen Rückgang nur wider.

Quelle: FT

Quelle: FT- “And the smart money is on the deceleration continuing. The OECD identifies several main risks. One is the intensifying trade warbetween the US and China. (…) financial instability in emerging markets, a China slowdown (for reasons other than trade) and higher oil prices.” – bto: Zumindest Öl sendet ein Zeichen der Entspannung (oder selbst eines der Rezession?).

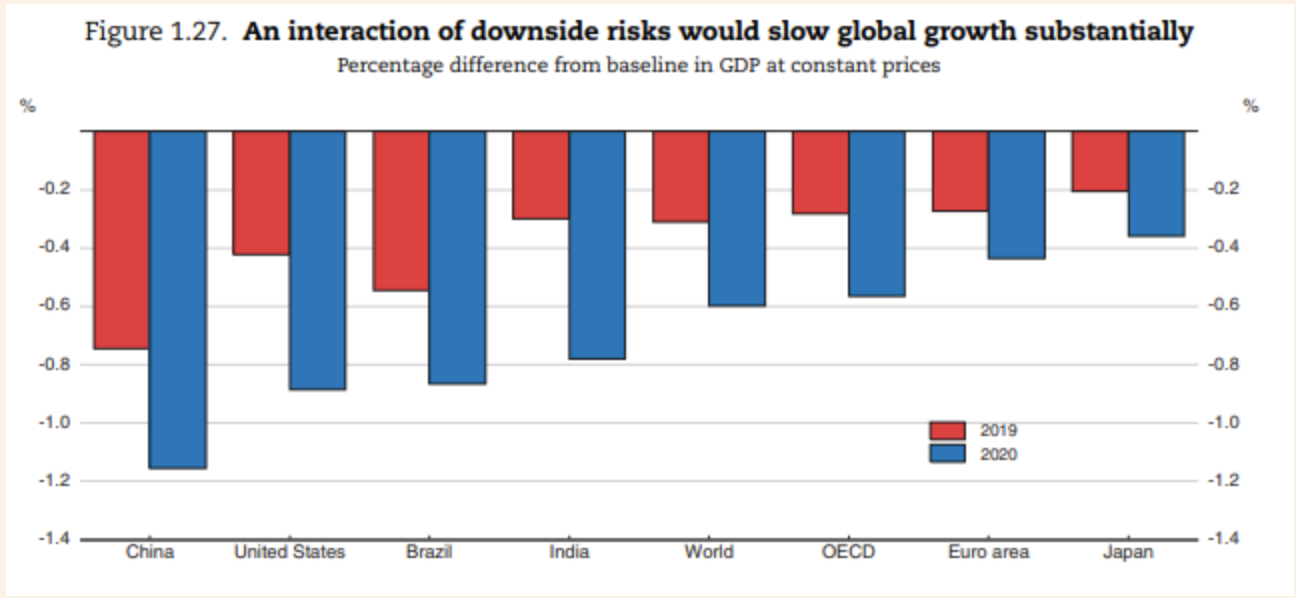

- “Suppose all these risks materialised? The OECD’s modelling suggests a sizeable hit to economies around the world, as set out in the chart below.” – bto: unwahrscheinlich? Vielleicht, aber der Effekt wäre so erheblich, dass man sich ernsthaft mit dem Szenario auseinandersetzen sollte.

Quelle: FT

Quelle: FTInteressanterweise wird die Eurozone hier als relativ robust angesehen. Ich denke, es ist ein Modellierungsfehler. Käme es wirklich zu einem Abschwung auf weltweiter Ebene, würde es die Eurokrise wieder entflammen und entsprechend wirken.

- “Where the OECD stands out is in its willingness to coax policymakers into much bolder actionthan most multilateral institutions have been willing to broach. As in 2009, the world should be prepared to come together for a joint fiscal stimulus, says Laurence Boone, OECD chief economist. She writes that ‘in the event of a downturn, governments should leverage low interest rates to coordinate a fiscal stimulus . . . a coordinated fiscal stimulus at the global level would be an effective means of quickly responding to a sharper-than-expected global slowdown’.” – bto: selbstverständlich! Es wäre der Auftakt zu einem globalen Margin Call mit massiv deflationären Konsequenzen. Dem muss man sich mit aller Macht entgegenstemmen, will heißen, noch mehr Schulden und noch billigeres Geld. Eine Runde könnte noch gehen. Eine.

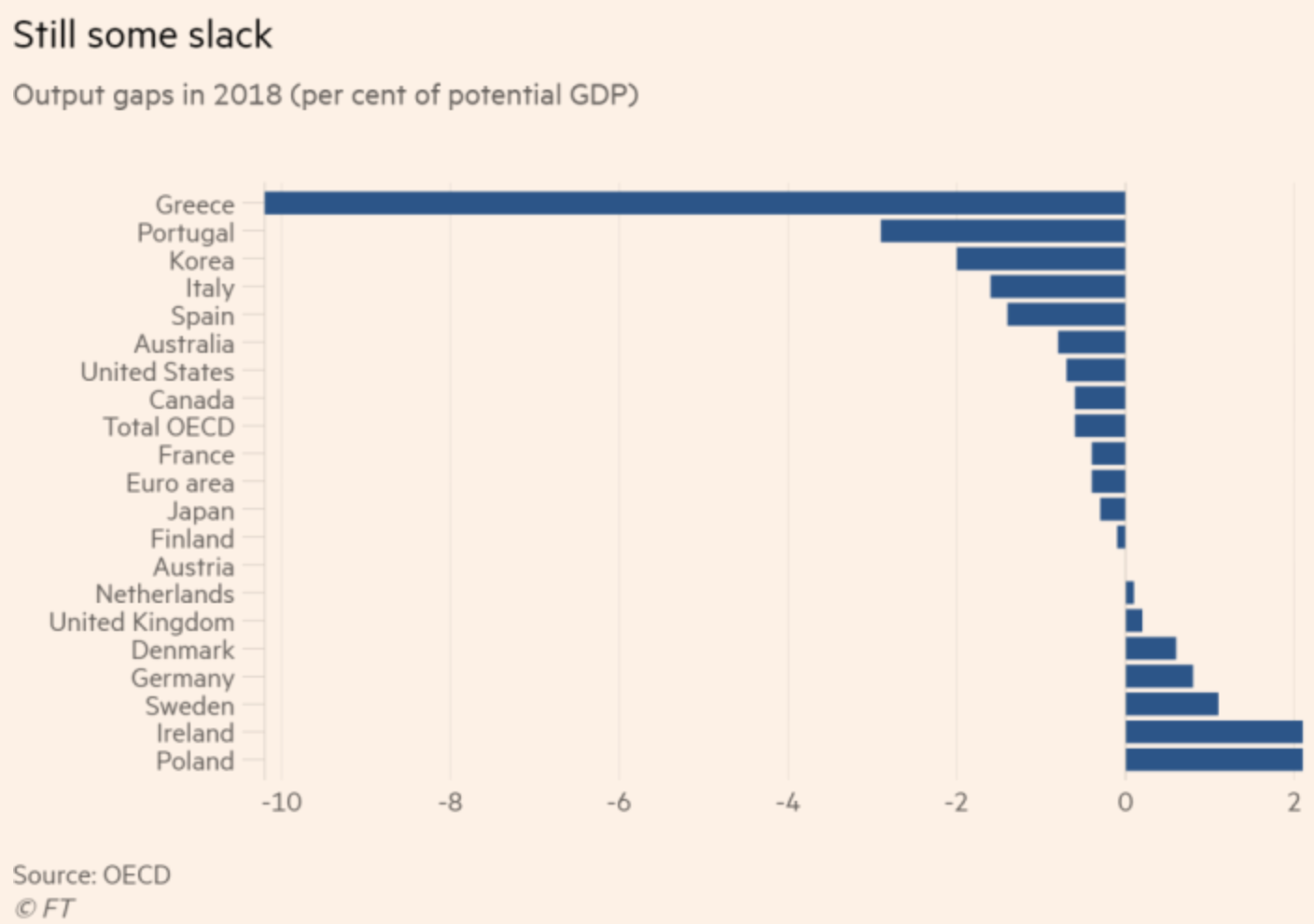

- “Boone and her team back it up with analysis showing that a fiscal stimulus would have a strong effect on growth(a ‘multiplier’ of about 1) and would be less risky for high-debt governments when done by everyone together. It helps that the OECD has more realistic estimates than most of how far countries are from full employment (their output gaps, in the jargon). These capture the weakness of the recovery from the global financial crisis and buttress the conclusion that a stimulus could be less risky than the alternative.” – bto: Man beachte, dass Italien nach dieser Analyse auf jeden Fall einen hohen Fiscal Multiplier haben sollte. Also hätte die italienische Regierung recht, wenn sie mit mehr Schulden die Wirtschaft stimulieren möchte.

Quelle: FT

- “The mood for international co-operation has soured badly in the past two years. But the global economy’s two chief antagonists may not be the hardest to persuade. The US last year showed it could happily engage in huge stimulus even when the economy is doing quite nicely. And China has just launched fiscal and monetary stimulus to combat its homegrown slowdown.” – bto: Das glaube ich auch. Es ist ein klares Zeichen dafür, wie kaputt das System ist, dass alle in einem beschleunigten „Weiter-So“ die Lösung sehen.

- “It is the Europeans who will be hard to convince. As Brad Setser has highlighted, the European Commission’s puzzling judgment is that all eurozone countries except Greece are above potential, and so the already tiny fiscal deficit (0.6 per cent of gross domestic product in aggregate) needs to be squeezed further.” – bto: nicht zuletzt getrieben von der deutschen Regierung. Aber die Staatsschulden sind schon jetzt nicht kontrollierbar, besser ein ordentlicher Schnitt, statt diese Agonie.

- “Therefore expect little enthusiasm from Europe for a co-ordinated fiscal stimulus, not even a conditional commitment to one in the case of a downturn.” – bto: Ich denke, dass der natürlich kommen wird, finanziert über die EZB (wenn auch versteckt). Höchstens eine gewisse Zeitverzögerung wäre einzupreisen.

→ ft.com (Anmeldung erforderlich): “Make policy like it’s 2009 again”, 23. November 2018