“China’s economy will get worse before it gets better”

Heute Morgen hatte ich den langfristigen Ausblick für China, nun der kurzfristige. Sieht ganz danach aus, dass China als Wachstumslokomotive der Welt vorerst ausfällt:

- “China’s economy is probably growing more slowly than the government’s target rate in the final weeks of 2018, with recent efforts to support growth having failed. Conditions may get worse before they get better; a cooling housing market is only beginning to take its toll while investment growth is also set to slow again. Pressure to do more to boost the economy will increase, testing the leadership’s very public commitment to reining in credit excesses and delivering more equitable growth.” – bto: Die chinesische Schuldenwirtschaft stößt an ihre Grenzen. Deshalb wird es schwer, einfach so umzubauen, vor allem, wenn die strukturelle Wachstumsrate auch wegen der Demografie unter Druck gerät.

- Das liegt auch an den Bemühungen der Regierung, das Kreditwachstum unter Kontrolle zu bringen: “The flow of credit through shadow finance channels shrank again in November, resulting in the growth of system-wide finance falling to a new low. Bank loan growth has been largely stable over the past two years, though this means that traditional lenders have failed to compensate for the forced retreat of trust companies and other providers of off-balance-sheet loans.” – bto: vermutlich aus gutem Grund, weil die Kredite eben zu gefährlich sind!

- “The temptation to relax constraints on risky lending practices appears to be increasing as the government tries to boost infrastructure investment activity — which is mostly financed by this kind of lending — and as the housing market finally turns. The headline index of our November real estate survey fell to its lowest level in almost two years as developers reported that prices dropped across all cities surveyed.” – bto: Es geht nur noch mit riskanten Krediten. Den Exzessen im Westen nicht unähnlich.

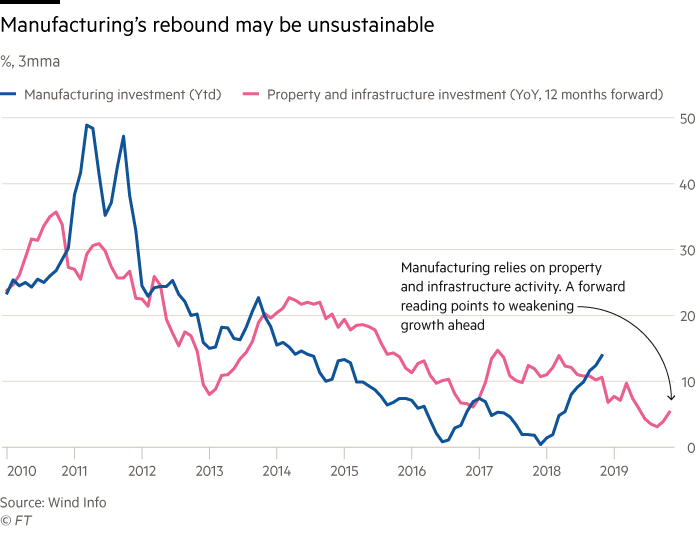

- “This does not bode well for overall investment, which is still a key driver of Chinese growth. Better manufacturing investment growth helped push up overall investment growth, but manufacturing is reliant on the housing market and infrastructure, as well as exports, and the outlook for all three is uncertain at best. Unless the domestic finance and global trade pictures improve, a forward reading of property and infrastructure investment suggests manufacturing growth is set to weaken again.” – bto: und damit auch die Weltwirtschaft!

Quelle: FT

Quelle: FT

- “Alarmed at the fallout from the 2015 stock market collapse, the government encouraged households to borrow to buy apartments and egged on banks to lend to them. The result is record high levels of household debt, while consumer expectations for further house price gains are cooling sharply. (…) slowing retail sales growth shows the susceptibility of consumer spending to falling asset prices and negative economic news.” – bto: Auch hier ist natürlich die Frage nötig, wohin die Immobilienpreise steigen sollen angesichts einer demnächst schrumpfenden Bevölkerung?

- “The government accepts that the years of heady growth are over and is trying to manage the economy’s slowdown while keeping domestic conditions — the labour market in particular — under control. This prescribes a continuation of targeted, gradual policy easing rather than big-bang stimulus such as was seen during the global financial crisis.

- “The problem is they may not be enough to counter the impact of a slowing housing market and still-tight credit conditions. This means Beijing will begin the new year with the challenge of keeping the economic engine on the track.” – bto: Schaffen sie es nicht, haben wir eine Rezession in der Welt, die wir bekanntlich wegen des enorm gestiegenen Leverages gar nicht gebrauchen können!