Immobilien global im Boom

Wir wissen, dass es einen klaren Zusammenhang zwischen Kreditwachstum und Immobilienpreisen gibt. Das ist klar sichtbar seit Jahrzehnten. Doch aktuell scheinen wir einen wahren Boom zu erleben, getrieben von dem noch billigeren Geld im Zuge der Corona-Krise. Die FINANCIAL TIMES (FT) spricht vom breitesten Boom seit 20 Jahren:

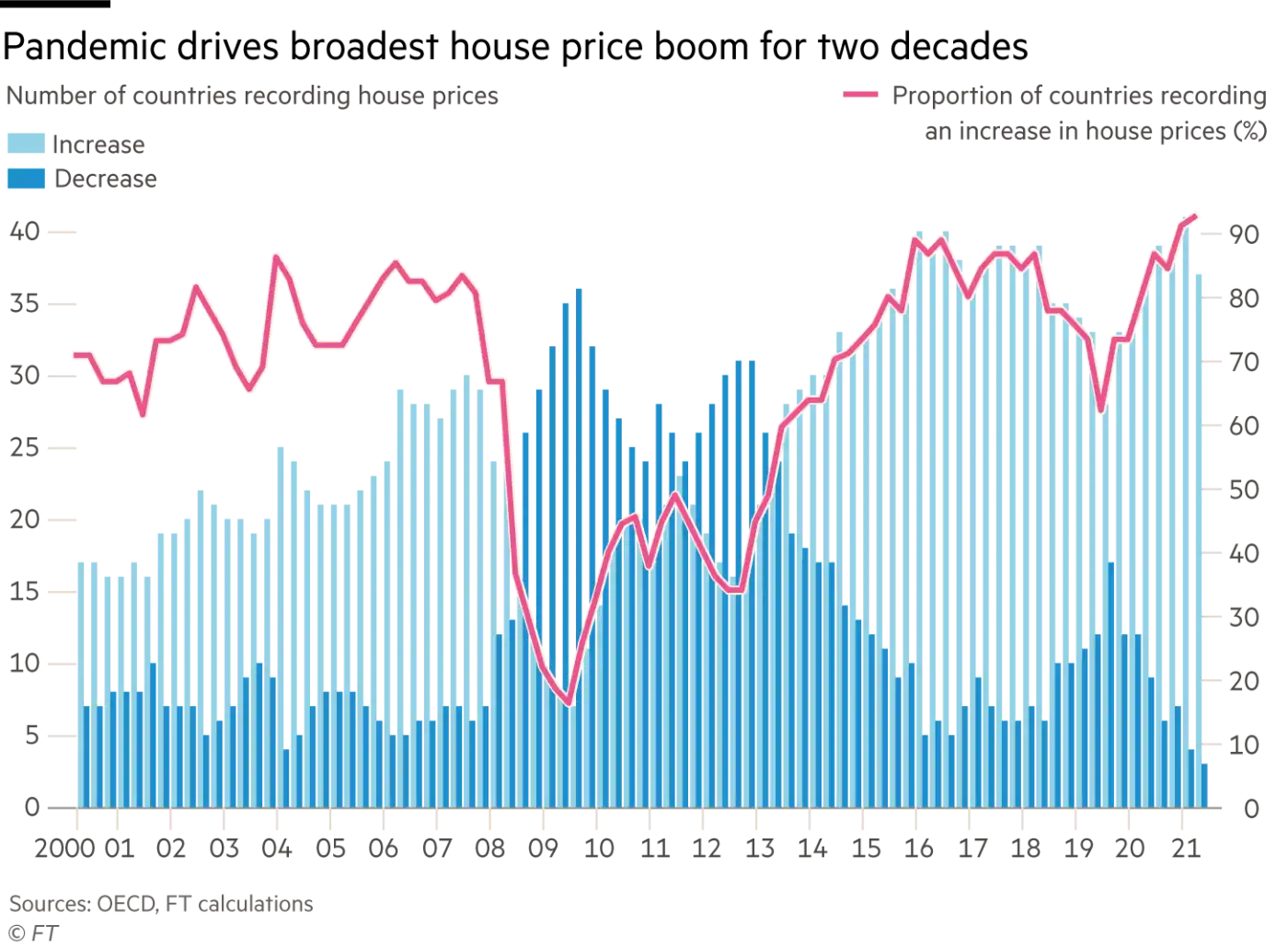

- “Of the 40 countries covered by OECD data, just three experienced real-terms house price falls in the first three months of this year — the smallest proportion since the data series began in 2000, analysis by the Financial Times found. Historically low interest rates, savings accumulated during lockdowns and a desire for more space as people work from home are all fuelling the trend, analysts said.” – bto: was auch klar ist, weil wir weltweit faktisch eine Geldschwemme haben.

Quelle: FT

Quelle: FT

- “Annual house price growth across the OECD group of rich nations hit 9.4 per cent — its fastest pace for 30 years — in the first quarter of 2021, as economies rebounded from last year’s severe coronavirus-triggered recessions.” – bto: Dies ist problematisch (Ungleichheit) und ein Indikator für breitere Inflation.

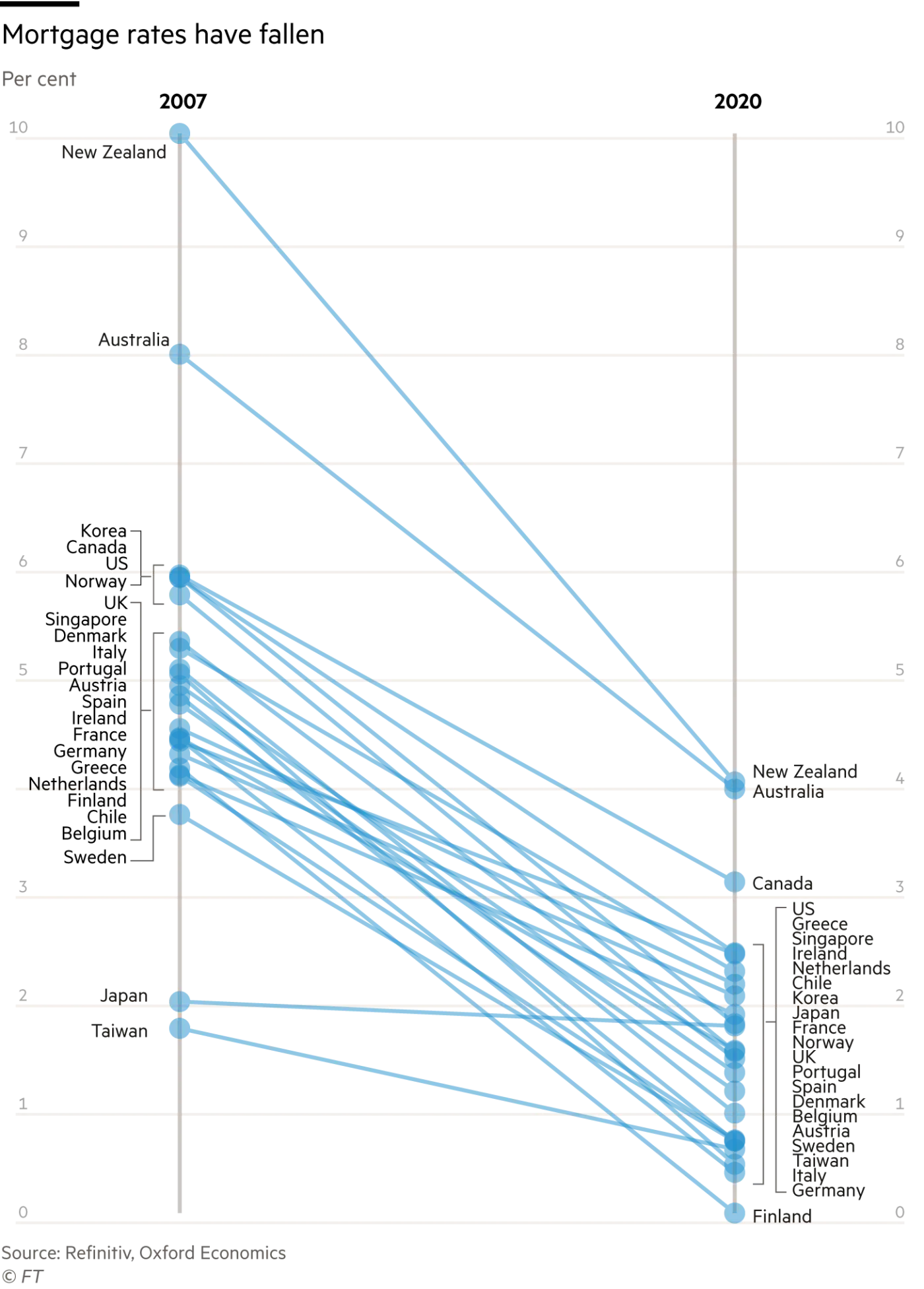

- “‘Extremely accommodating financial conditions’ with record-low interest rates had helped boost house prices at an unusually fast pace during a period of weak economic activity, Borio said. Low borrowing costs make house purchases more affordable relative to rent and to other investments. In addition, many households, particularly those that were already better off, have accumulated large savings since the start of the pandemic as lockdowns limited spending while some jobs were protected. ‘A lot of this additional income has been allocated to the housing market,’ said Martínez-García.” – bto: Es ist sehr simpel. Aber es ist eben eine seit Jahren laufende Entwicklung. Und das ist die Abbildung, die ich für so relevant halte, dass ich den Artikel hier bespreche.

Quelle: FT

- “Average house prices across the OECD are growing faster than incomes, making housing less affordable. They are also rising faster than rents. Adam Slater, lead economist at Oxford Economics, said properties in advanced economies were about 10 per cent overvalued compared with long-term trends. That makes this boom one of the biggest since 1900, he calculated — although nowhere near as big as the run-up to the financial crisis.” – bto: Das mit den Trends ist so eine Sache, wenn der Trend eine konstante Höherbewertung relativ zum BIP/Einkommen bedeutet. Denn so ein Trend kann per Definition nicht ewig anhalten und ist im konkreten Fall dem zunehmenden Leverage der letzten 40 Jahre geschuldet.

- “Credit growth is lower than before the global financial crisis, suggesting ‘a lower risk of a bust compared to, say, 2006-2007’, he said. Mortgage growth was driven largely by people with strong financial positions, and across most advanced countries households were less indebted than before the financial crisis, suggesting a lower risk that the situation would follow the same path with a wave of defaults and fire sales.” – bto: Das mag schon sein, dennoch ist der Leverage im System weiter gestiegen und damit die Anfälligkeit.

Immos sind heute die wichtigste Alternative für frühere Bond-Investoren, solange es um langfristige Anlage geht und nicht auf die Liquidität ankommt. Das zieht sich durch von Privatanlegern bis zu Versicherungen. Da werden immer noch laufend Milliardenbeträge umgeschichtet. Dividend Stocks sind für die Risikopräferenz klassischer Bond-Investoren keine Alternative.

Private Käufer mit der Zielsetzung Eigennutzung denken sich: Wenn nicht jetzt, wann dann?

@Schwarzenberg

“Immos sind heute die wichtigste Alternative für frühere Bond-Investoren, solange es um langfristige Anlage geht und nicht auf die Liquidität ankommt.”

Das geht auch als vergleichsweise liquide Anlageform, wenn man das Immobilienportfolio als an der Börse gelistete Aktiengesellschaft oder als REIT strukturiert.

Mittlerweile frage ich mich, wieso überhaupt noch irgendjemand in geschlossene Immobilienfonds investiert.

>“Average house prices across the OECD are growing faster than incomes, making housing less affordable. They are also rising faster than rents.>

Wenn die Häuser immer schwieriger zu finanzieren sind mit Blick auf die Einkommensentwicklung und die Mieten nicht in dem Maß wie die Hauspreise steigen, muss man annehmen, dass die Hauspreise STEIGEN, weil

a) mit WEITER fallenden Zinsen gerechnet wird, daher günstiger (Zinsbelastung) bzw. teurer (Hauspreis) gekauft werden kann und folglich auch bei HÖHEREN Hauspreisen eine auskömmliche Rendite zu erzielen ist

ODER

b) – mal als These in den Ring geworfen – Hauskäufer an eine INFLATIONÄRE Entwicklung glauben, was die Leute auch dann in Sachwerte treibt, wenn die Zinsen NICHT weiter fallen und kaum noch eine auskömmliche Rendite zu erwirtschaften ist, um ihr Vermögen vor Geldwertverlust zu SICHERN.

Ich weiß nicht, ob a) oder b) das Kaufmotiv ist.

b) ist jedenfalls nicht auszuschließen, weil Inflation (der Verbraucherpreise) nicht nur gefühlt, sondern auch amtlich festgestellt und damit – zumindest als bestehender Sachverhalt, wenn auch nicht notwendigerweise als fortwährender – NICHT mehr zu bestreiten ist.

Da fangen Leute schon mal an, zu ÜBERLEGEN was ist, wenn …

Institutionelle Investoren haben noch einen Grund

c) wenn man den ganzen Markt für Wohnimmobilien in einem Stadtteil oder in einem bestimmten Marktsegment (z.B. Studentenwohnungen) unter seine Kontrolle bringt, dann kann man monopolistische Slumlord-Renditen erzielen und muss sich nicht mit normalen Marktrenditen zufrieden geben. Was soll der Pöbel machen, irgendwo muss er ja wohnen?

https://www.zerohedge.com/markets/after-cornering-rentals-blackstone-now-going-after-student-dorms

Das ganze lohnt sich natürlich umso mehr, je niedriger die Realzinsen sind, bei ungefähr *minus* 4% p.a. in den USA für eine 10-jährige Finanzierung kann man auch ein Aufgeld beim Kauf verschmerzen, um sich mit ihm die gewünschte Position als Slumlord in attrativen Märkten zu erkaufen.

@Tischer:

a) Macht keinen Sinn, denn unabhängig von den Zinsen müssen sich die Hauspreise langfristig am verfügbaren Einkommen orientieren.

b) Private Hauskäufer haben wenig Ahnung von Inflation. Immobilien sind aber KEIN Inflationshedge, besonders nicht wenn die Bewertung bereits sehr hoch ist (ähnlich Aktien). Die Kosten einer Immobilie inflationieren nämlich auch und ob die Mieter ihr Einkommen real steigern können ist fraglich. Wer wirklich Schutz vor Inflation will, der kauft entsprechende Rohstoffe oder Unternehmen mit Preissetzungsmacht (bspw. Louis Vuitton). Die Instis kaufen aktuell einfach den Markt leer weil der risikolose Zins so niedrig ist (in D nominal unter 0). Das Tapering der FED wird deshalb interessant zu beobachten. Steigen nämlich die Renditen auf Staatsanleihen, steigen auch die Bauzinsen. Auch eine höhere Inflation wird die Bauzinsen treiben. Welche Bank vergibt denn 1% Immokredit bei 4% Inflation?

Am Immomarkt herrscht auch viel Kaufpanik und FOMO. Das geben ehrliche Makler schon zu. Da werden Bruchbuden zu Preisen verkauft, das erinnert an die Ostimmobilien nach der Wende. Solange die Marktteilnehmer an steigende Preise glauben, kann sich sowas leicht selbst verstärken. Der Umschwung wird nur noch heftiger. Andreas Beck prognostiziert ja eine Wende am Immomarkt aufgrund der Demografie, völlig unabghängig von Zinsen.

@ Jaques

Zu a):

Es ist zwar richtig, dass die Hauspreise sich – LANGFRISTIG – am langfristig verfügbaren Einkommen orientieren MÜSSEN, WENN man die Zinsentwicklung als unbeachtlich, d. h. neutral annimmt.

Wenn man aber FALLENDE Zinsen unterstellt und die Einkommensentwicklung als neutral ansieht, können die Hauspreise rational begründbar weiter steigen.

Kurzum:

Es kommt auf die ANNAMEN man, an denen man sein Handeln orientiert.

Da es dabei um auf die Zukunft bezogene Annahmen geht, ist man relativ frei bei seinen Annahmen.

b) >Private Hauskäufer haben wenig Ahnung von Inflation.>

Mag so sein oder auch nicht.

Sie müssen nicht viel Ahnung haben, sondern die Inflation nur FÜRCHTEN.

Wer Bargeld hortet oder es sein Geldvermögen auf Konten belässt, der WEISS, was Inflation für diese „Anlagenklassen“ bedeutet.

>Immobilien sind aber KEIN Inflationshedge,..>

Stimmt, wenn die Inflationsentwicklung maßvoll ist.

Wenn sie nicht maßvoll ist, sieht das anders aus.

Auch hier wieder:

Es kommt auf die Annahmen an.

Die können natürlich UNREALISTISCH sein.

Ich erkenne keine Hyperinflation, weiß aber auch nicht, welche Inflationsentwicklung wir in – sagen wir – 10 Jahren haben werden.

>Am Immomarkt herrscht auch viel Kaufpanik … Solange die Marktteilnehmer an steigende Preise glauben, kann sich sowas leicht selbst verstärken.>

Eben.

Was ich versucht habe, war lediglich zu RATIONALISIEREN, d. h. Annahmen zu unterlegen, die Käufe bei steigenden Preisen begründbar erscheinen lassen.

Ich empfehle nicht, Immobilien zu kaufen.

>Andreas Beck prognostiziert ja eine Wende am Immomarkt aufgrund der Demografie, völlig un-abghängig von Zinsen.>

Auch das ist Zukunft mit Annahmen, die z. T. offen sind.

…… die frage ist, wie lange dieser immobillien-boom und die flucht in die sachwerte, noch anhält?

wenn die bereits laufende inflation die kaufkraft weiter senkt?

wenn die coronamaßnahmen und deren auswirkungen (weitere erkrankungen und sterbefälle auch bei den geimpften), die wirtschaft strangulieren?

sowie dies auch durch die maßnahmen zum (angeblichen) klimaschutz die wirtschaft kein ausreichendes wachstum erzielt?

die politik ist nahezu völlig konfus, noch die richtigen entscheidungen zu treffen, da jede handlung graphierende negative konsequenzen nachsich ziehen.

dies ist geschuldet dem zwiespalt des wachstumszwanges beim großkapital und den bürger ruhig zu halten von deren auswirkungen.

ich denke, dass der kipp-punkt mit corona endgültig erreicht ist: die kreditbelastungen, aber auch die umfangreichen maßnahmen (corona, klima etc.) lassen kein notwendiges wachstum der breiten wirtschaft mehr zu.

ein wachstum geschied nur noch für die big-player, indem der klein- und mittelstand langsam krepiert.

@foxxly

Viel zu wenig wird m.E. reflektiert, was Automatisierung / Digitalisierung/ für humans wirklich bedeutet: Menschen ( lebendig ) haben sich überflüssig gemacht, Terminatoren brauchen keine Häuser , sie sind fast unbesiegbar :

https://www.youtube.com/watch?v=y3RIHnK0_NE

@Dr. Lucie Fischer

Anspruch der Propaganda youtu.be/bAdqazixuRY

und Wirklichkeit der Automatisation:

youtu.be/Cpg_3syMT_U

youtu.be/CGKLG4XB_7Y

& Never forget the bio robots, cheap und easy:

https://youtu.be/XzfsfYnuc8c

Angst als Waffe zur Domestikation, die Lämmer für immer schweigen.

@ Dr. Lucie Fischer

Nicht so martialisch und pessimistisch – Menschen machen sich nicht überflüssig.

Eine meiner Erfahrungen:

Fahrkartenautomat auf einem Provinzbahnhof.

Ältere Menschen, die mal eben zu einem Fußballspiel fahren wollten, kamen damit nicht zurecht.

Da hat einer den Fahrkartenautomaten eingetreten und danach ist etwa das Dutzend Menschen in den Zug mit der Parole eingestiegen:

Da bezahlen wir zur Not eben im Zug, wenn überhaupt einer kommt und kassieren will.

Wir können alle bezeugen, dass der Fahrkartenautomat defekt war.

Fazit:

Wenn die Bahn unter derartigen Bedingungen mit Fahrkartenautomaten Geld verdienen will, muss sie diese so gestalten, dass Menschen, die noch nicht digital verwahrlost sind anhand ihres gesunden Menschenverstands damit zurechtkommen.

ODER:

Sie muss die personale Fahrkartenausgabe in den Zug verlegen, was in Stoßzeiten ein ganz paar Leute verlangt.

Wie auch immer, ohne Menschen funktioniert diese Welt nicht.

@Herr Tischer

“Da hat einer den Fahrkartenautomaten eingetreten und danach ist etwa das Dutzend Menschen in den Zug mit der Parole eingestiegen: Da bezahlen wir zur Not eben im Zug, wenn überhaupt einer kommt und kassieren will. Wir können alle bezeugen, dass der Fahrkartenautomat defekt war.”

Profi-Tipp: Wenn man den Fahrkartenautomaten nicht umtritt sondern fachgerecht in die Luft sprengt, hat man gleich noch ordentlich Biergeld fürs Stadion. ;)

Im Prinzip illustriert die Anekdote eine alltägliche Anwendung desjenigen Prinzips, das sich schon in der amerikanischen Unabhängigkeitserklärung finden lässt: “Governments are instituted among Men, deriving their just powers from the consent of the governed,—That whenever any Form of Government becomes destructive of these ends, it is the Right of the People to alter or to abolish it”

Wir werden sehen, wie lange das noch hält. Wir hatten auch jahrhundertelang Regierungen, bei denen der Herrscher behauptet hat, von Gott zur Herrschaft legitimiert zu sein, was eine Priesterkaste im Tausch gegen königliche Privilegien gerne bestätigte.

Und es muss ja kein personaler Gott sein, mit “Kampf gegen den Klimawandel” als Naturreligion funktioniert das Gottesgnadentum bestimmt genauso gut.

Dietmar Tischer, 12:28

Lieber, sehr geehrter Herr Tischer,

Ich bin nicht pessimistisch! In meinem Beruf/ geschlossene Stationen/ musste ich allerdings worst-case-Szenarien zu jeder Sekunde / Autopilot/ berücksichtigen- sonst

( gibt es zur Genüge ) degeneriert man als Psychiater zum Psychopharmaka-Dealer und schadet mehr als man hilft. ( Iatrogenik, Ivan Illich ) .

Für genau zwei Trieb-Derivate sollte man Experte sein: destruktive und libidinöse Triebe, und deren Mischungen sind so vielfältig wie binäre Zahlenkombinationen. Die menschliche Aggression wird leider nur oberflächlich verstanden, ( es gibt keine Pille gegen Mord oder Suizid !), auch hier lösen sich Rätsel in der Kleinkindforschung.

Und jetzt stelle ich mir Sie als Held in der Bahnhofshalle vor:

EIN Tritt mit dem Tischer-Biker- Boot und der Karten-Apparat bricht zusammen, ich sorge ( Drehbuch! ) für standing ovations der Zuschauer. Applaus, Bravo! Zombietod.

Im Zug wird gefeiert, Sie sind der Held, und ich verteile ( ausnahmsweise Zuckerkram) sweets, etwa so wie in der dämlichen Haribo-Werbung:

https://www.youtube.com/watch?v=6nVaQBhWyFY

Nur in einem Punkt Dissens:

Die Welt existiert ohne uns, s. Alan Weismann ( 2007 ) : Die Welt ohne uns,

( Wenn nur meine Rauchschwalben vor dem Aussterben gerettet würden, ich würde nicht protestieren). Das Dogma ” seid fruchtbar, und mehret euch” gilt nicht mehr.

@ Dr. Lucie Fischer

Wenn Sie das Drehbuch schreiben und auch noch die Regie übernehmen, dann laufe ich bestimmt zu Hochform auf.

Heißt:

Das Spektakel wird sich so schnell rumsprechen, dass die Gewerkschaft der Lockführer sofort den GESAMTEN Zugverkehr in Deutschland einstellt, damit die Rentner-Randale nicht das Land ansteckt ;-)

Zum Dissens:

Sie haben vollkommen Recht.

Ich hätte sagen müssen, dass ohne Menschen UNSERE Welt – Ausschnitt aus der gesamten – nicht funktioniert.

Aus „Sicht“ der Evolution sind wir Menschen nicht einmal ein Betriebsunfall oder Ausrutscher, sondern letztlich nicht mehr als ein Fliegensch***.

>Das Dogma ” seid fruchtbar, und mehret euch” gilt nicht mehr.>

Es hat schon immer auf einer Illusion beruht.

Beispiel Heuschrecken:

Fressen alles leer und legen unzählige Eier ab.

Wenn die Eier schlüpfen, passiert was?

Der Nachwuchs stirbt, weil es nichts zu fressen gibt.

So enden Heuschreckenplagen.

@Herr Tischer

Davos-Klaus und seine Freunde wollen, dass in Zukunft die niederen Stände die Heuschrecken einfach aufessen. Die Propagandakampagne läuft schon:

Watch Brianna Keilar eat dead cicadas on live TV [CNN]

https://youtu.be/kaj6-sAC_6o

Dafür gibts sogar einen “White House Champion of Change”-Award.