Dämmerung (“Twilight”) für den Euro?

Das hatten wir auch schon länger nicht mehr. Einen Bloomberg-Artikel, der von “Twilight of the Euro” spricht. “Twilight” kann man übersetzen als “Dämmerung”, aber auch als “Lebensabend”.

Nun gut, Leser von bto wissen, dass der Euro Länder zusammenpackt, die weniger gemein haben als eine fiktive Währungsunion aller Staaten der Welt mit dem Anfangsbuchstaben “M”. Dennoch ist es ungewöhnlich, nach der erfolgreichen “Eurorettung” wieder solche Schlagzeilen zu lesen. Hat John Authers von Bloomberg nicht die letzten Verlautbarungen aus der EU gehört? Wir retten das Weltklima und der Euro ist gerettet?

Na gut, was meint er denn?

- “(…) the euro is at its weakest in four months, close to setting a 30-month low, and once more below its level on the day of the U.S. election in November 2016. One again the euro is falling down.” – bto: und dazu noch das passende Bild:

Jetzt kann man natürlich sagen, dass er seit einigen Jahren seitwärts tendiert. Erholt hat er sich jedoch nicht, wie Einige – auch ich – erwartet hätten.

- “First of all, of course, there is politics. Across Europe, the center cannot hold. (…) German politics is thereby thrown into chaos. In Ireland, the emergence of the radical and left-wing Sinn Fein in the country’s general election as the largest party in its lower house has similarly left the established parties of center-left and center-right in a state of confusion.” – bto: Wir haben es halt mit einem strukturellen Umbruch zu tun, ausgelöst durch wirtschaftliche Enttäuschung und Versagen der Politik in wichtigen Feldern. Ray Dalio hat es nicht zu Unrecht mit den 1930er-Jahren verglichen.

- “Then there is the manufacturing sector. On Monday, Italy followed Germany and France in reporting dreadful industrial production figures for the end of last year. The coronavirus had had no effect at this point; manufacturing was supposedly picking up again and awaiting a boost from renewed Chinese post-trade war demand. We now see that all of the eurozone’s biggest three economies ended the year slowing sharply.” – bto: was nicht wundert: Demografie, Fokus auf Umverteilung, Euro, falsche Prioritäten.

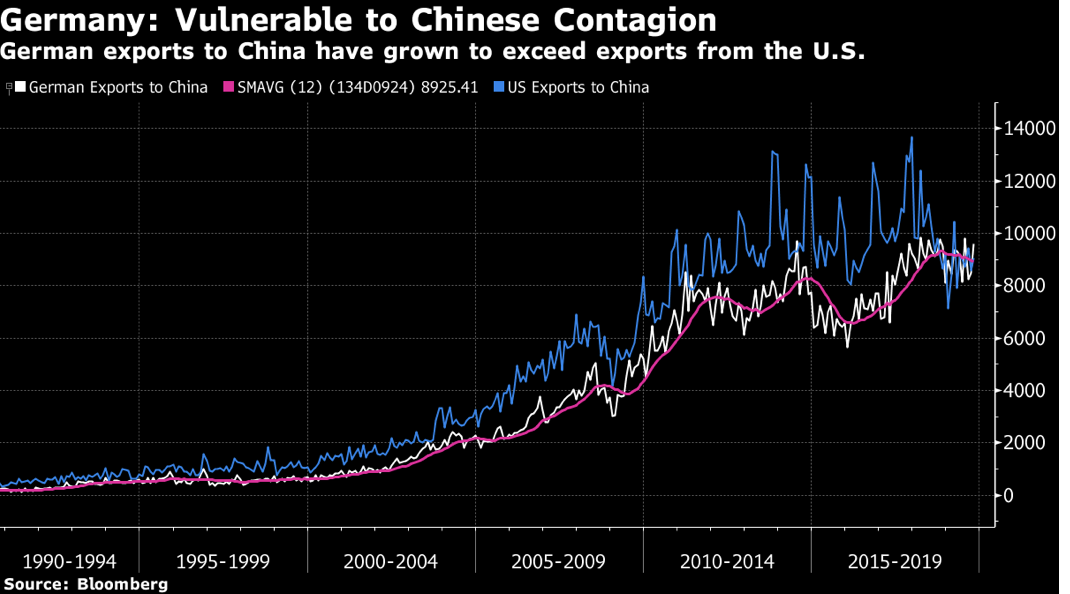

- “This is bad because, thirdly, the eurozone is these days no place to take shelter from trouble in the Chinese economy. A slowdown of some dimension for China can now be taken as a given, just as a result of the belated measures to contain the epidemic. Sadly for Europe, this will come as Germany had put itself at China’s economic mercy. Data from the International Monetary Fund show that exports from Germany to China now slightly exceed those from the U.S., a much larger economy.” – bto: Jetzt habe ich im Märchen vom reichen Land keinen Virus als Auslöser gesehen, aber auf die enorme Abhängigkeit von China hingewiesen.

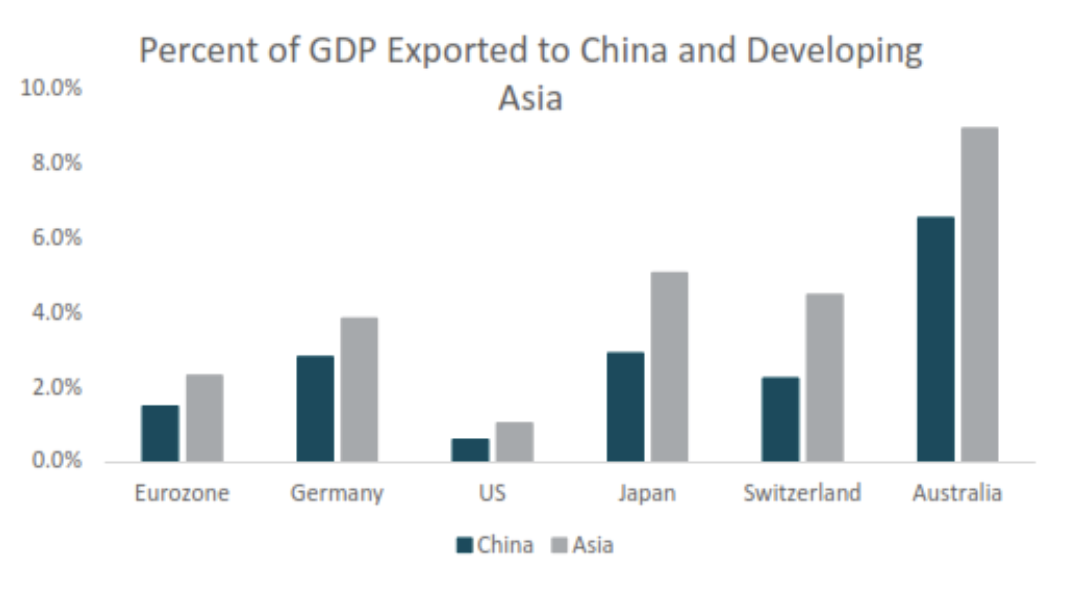

- “If you want a haven from China, then, it is certainly not the euro. And it is probably the dollar. This chart from John Velis of Bank of New York Mellon Corp. shows that even though the U.S. has been the international aggressor in taking on China’s trade power, it stands to lose the least from that economy’s current difficulties. It is the obvious haven:” – bto: Ich muss gestehen, dass ich es zwar geahnt habe, aber nicht in diesem Umfang. Die Schweiz ist übrigens auch interessant in diesem Zusammenhang. Dürften nicht nur Uhrenexporte sein.

- “Beyond these fundamental reasons, there is also the technical issue that the euro has become a highly attractive currency for funding carry trades — the practice of borrowing in a currency with low interest rates, parking in one with higher rates and pocketing the difference, or ‘carry.’ (…) Over the last five year it has been a far more profitable funding currency for those wanting to park in Mexican pesos, for example, than the yen” – bto: Hallo EZB, hallo Verteidiger der EZB-Geldpolitik: Was hier passiert, ist gefährlich für die Stabilität des Welt-Finanzsystems, betrieben durch die EZB!

- “When a currency becomes popular for funding carry trades, it naturally comes under downward pressure. That is contributing to the euro’s problems. (…) however, it is clear that the dollar seems mighty attractive to foreign exchange traders at present. (…) The Federal Reserve is now expected to cut target rates at least once this year with a 50-50 chance of a second reduction, according to fed funds futures, while the European Central Bank stands still. And that also makes no difference.” – bto: Klartext: Die Märkte trauen dem Euro nicht.

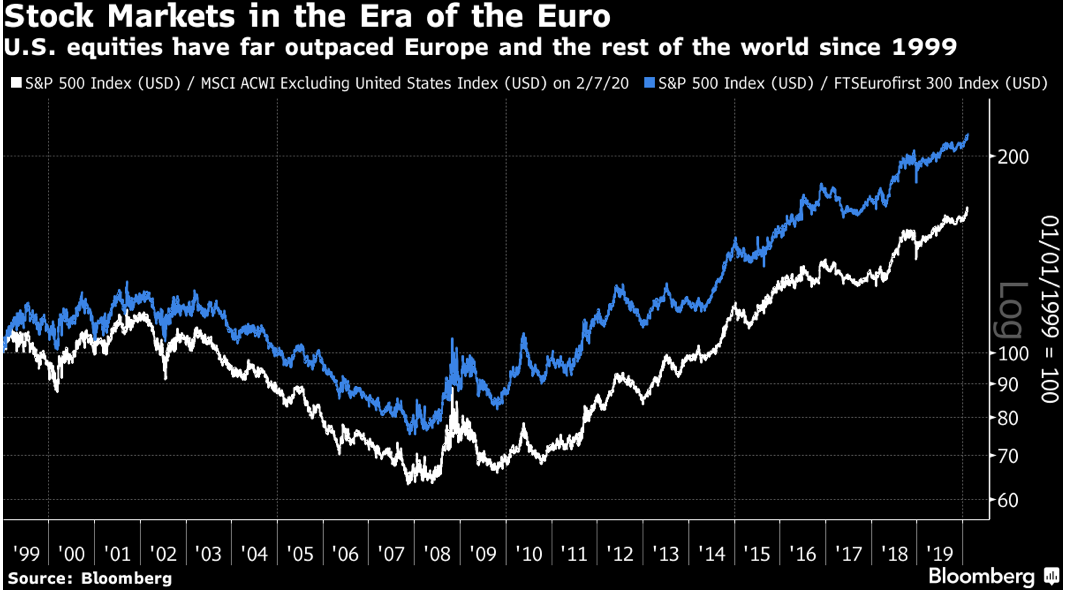

- “So why is money running toward the U.S., despite everything? Without wishing to pile on to any political triumphalism, the markets are obviously partial to the current situation, where Senator Bernie Sanders is seen as likely to be nominated for president by the Democrats, and also likely to lose to Donald Trump. There is also some triumphalism around U.S. companies. The biggest companies in the world, at present, are all American, and they are busily conquering the rest of the planet. U.S. internet groups’ dominance has helped to ensure that the U.S. stock market continues to outperform the rest of the world, and particularly Europe, to a remarkable extent. The chart shows the relative performance of U.S. stocks since the beginning of 1999, when the euro came into being.” – bto: Platt gesagt, die USA liefern und die EU nicht. Trump steht dafür, dass die USA weiter liefern. Über die EU muss man nichts sagen.

- “(…) the coronavirus is now widely interpreted as the moment that revealed China isn’t, in fact, ready to challenge American economic hegemony, while there is also excitement at the notion that the botched handling of the situation in Wuhan could yet signal major trouble for China’s political model. Couple that with a sense that Europe, whose common currency was intended two decades ago to launch another challenge to American exorbitant privilege, is also now revealing a deeply flawed political model, to go with a structurally challenged economy, and you have what could be a moment of classic market revulsion for Europe, combined with American triumph, and a very strong dollar.” – bto: Und wie schlecht muss man sein, um schlechter als der Dollar zu sein!