Die Blase ist erst am Anfang – meint Dylan Grice

Vor einigen Tagen hatte ich an dieser Stelle ein Interview mit Dylan Grice bei the market besprochen. Wenig später erschien ein Gastbeitrag von ihm ebenfalls dort. Da ich ihn interessant fand, hier meine Highlights daraus:

- “Stimulus today is excessive and credit conditions loose in part because central banks are relaxed towards the risk of CPI inflation. On this they might be right. But they are similarly relaxed over obvious signs of overheating in financial markets, and on this we are sure they are wrong.” – bto: Natürlich treiben die Notenbanken seit Jahren die Assetpreis-Inflation!

- “The historical precedents we explore below do not bode well. We think it likely that we’re in the foothills of a policy mistake of epic proportion which will have potentially devastating consequences.” – bto: Ich glaube nicht, dass es ein “Fehler” ist, sondern ein Vorsatz.

- “Jerome Powell was recently asked by Harvard’s Greg Mankiw on CNBC’s Squawk Box about how the Fed were thinking about the risks of inflation. The answer was comprehensive and is worth reproducing almost verbatim: ‘The big picture is still that we’ve seen (…) three decades, a quarter of a century, of lower and more stable inflation and we’ve seen really the last decade be characterized by global disinflationary forces and large advanced economy nations struggling to reach their 2% inflation goal from below. So that, I think, is the broader setting. In addition, the pandemic itself has produced lower inflation readings (…) as we look forward we’ll probably see an increase in readings but that’s really not going to mean very much, it won’t be very large or persistent in all likelihood, it’s just a function of those readings falling out (…) if the economy reopens, there’s quite a lot of savings on peoples’ balance sheets, there’s monetary policy, there’s fiscal policy, you could see strong spending growth and there could be some upward pressure on prices. Again, though, my expectation would be that that would be neither large nor sustained (…) We have had inflation dynamics in our economy for three decades which consists of a very flat Phillips curve, meaning a weak relationship between high resource utilization, low unemployment and inflation, but also low persistence of inflation, critically (…) of course those dynamics will evolve, but it’s hard to make the case why they will evolve very suddenly, in this current situation. I described our new framework and our guidance, in major part we are looking at actual inflation, we want to see actual inflation, and part of the reason for that is that all during the long expansion, many of us – and that includes me – were writing down a return to 2% inflation, and maybe a mild overshoot, year after year after year. And year after year inflation fell short of that. So we have tied ourselves to realizing actual inflation for example, that’s the way our rate guidance works is, you’d have to see inflation reach 2% – not in a forecast, but actually. So we are looking at actual inflation.’” – bto: Die Fed schaut also nicht auf künftige Inflationsraten, sondern nur auf die heutige. Damit kann sie natürlich deutlich überschießen, weil es eben eine Weile dauert, Inflation wieder unter Kontrolle zu bekommen.

- “He seems determined that there will be no such error on his watch. (…) We predict a different error, that of focussing so exclusively on the CPI that harder to interpret indicators of building financial risk are ignored. We believe history is on our side given it is an error economists have made repeatedly.” – bto: Natürlich genügt es nicht, auf die Konsuminflation zu blicken, wenn man die Stabilität des gesamten Finanzsystems im Blick haben sollte!

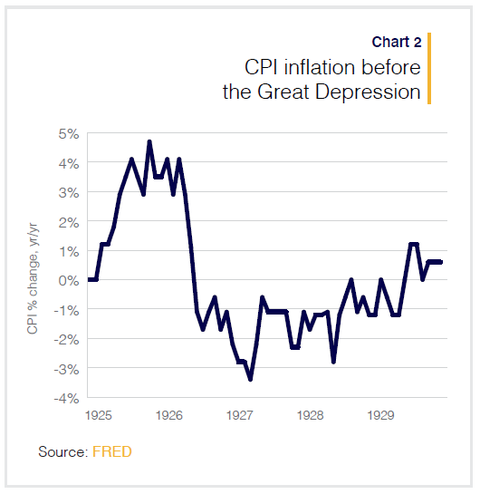

- “Indeed, one of the original architects of the idea that the stability in the CPI was a necessary and sufficient condition for stability in the economy was the economist Irving Fisher, who first articulated his plan for stabilizing the price level in 1913, the year of the Fed’s creation. Not coincidentally, that was the very same Irving Fisher who would later predict that stock prices had «reached what looks like a permanently high plateau» just nine days before the Great Crash of 1929. And in this context one can clearly understand the man’s optimism. After all, in preceding years, CPI inflation had exhibited precisely the kind of calm, reassuring steadiness which Fisher’s theories predicted would guarantee economic, and even social stability (Chart 2).” – bto: Das ist schon beeindruckend. Es gab auch damals keine Inflation und das bei einer boomenden Wirtschaft. Das massive Kreditwachstum wurde als unproblematisch angesehen, wie wir wissen zu Unrecht. Zu Fishers Ehrenrettung muss man allerdings noch anmerken, dass er durchaus brillant war. Ich denke an die Debt-Deflation-Theory of Great Depressions. Auch der Chicago-Plan ist interessant.

Quelle: the market

- “A little-known backdrop to the 1920’s ‘Go-Go’ years is that the Federal Reserve was then embarking upon a policy experiment. The growing consensus amongst economists, both in the United States and abroad, largely influenced by Irving Fisher’s ideas, was that central banks should focus entirely on delivering CPI stability.” – bto: Und heute wird das als Zwei-Prozent-Ziel verkauft.

- “John Maynard Keynes himself was convinced of the wisdom of the new philosophy, hailing ‘the successful management of the dollar by the Federal Reserve Board from 1923 to 1928’ as a ‘triumph’ for currency management. Unsurprisingly, perhaps, Keynes failed to see the crash coming with any more clarity than Fisher had.” – bto: Man hat eben nicht auf die Assetpreisinflation geblickt.

- “Of all the retrospectives on the 1930s Great Depression, most have focused on the aftermath of the crash, and in particular the tightness of monetary policy which likely exacerbated it, but few seem to have given much thought to the policies which preceded the crash, or the extent to which those policies where responsible for its subsequent savagery. This is probably why the mistake was repeated.” – bto: und zwar mehrfach und immer größer. Das muss man erst mal hinbekommen!

- “In June 1999, as the Nasdaq bull-run was turning into a euphoric parabolic, then-Fed Chairman Alan Greenspan soothed growing concerns thus: ‘It is (…) up to us at the Federal Reserve to secure the favourable inflation developments of recent years and remain alert to the emergence of forces that could dissipate them. (…) There was no bubble according to Greenspan, only prosperity. Replicating the thought process of Fisher seventy years earlier, the possibility that the Fed were stimulating a mania wasn’t even entertained. How could monetary policy be too loose when inflation was so low?’”– bto: Genau diese Argumentation bekommen wir auch heute zu hören. Zugleich haben wir die Klagen über die “Ungleichheit”, die immer mehr zunimmt.

- “Only a few years later, in 2006, as a grotesquely inflated U.S. housing market was already rolling over, beginning a descent which would lead to a generational global economic collapse, Ben Bernanke was famously oblivious to the risk: ‘The effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system.’ Bernanke had acquired the nickname Helicopter Ben after a speech pointing out – correctly – that in most circumstances, there was no limit to the inflation a central bank could create.” – bto: Das ist zutreffend; zunächst eher bei den Vermögenspreisen, danach auch bei den Konsumentenpreisen.

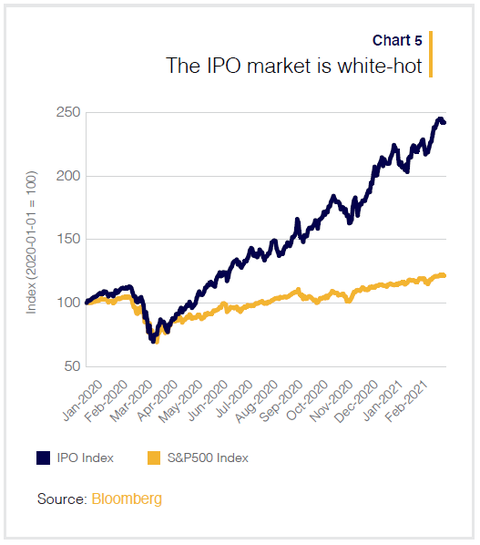

- “As the stock market made new all-time highs, Tesla’s market capitalization in early February surpassed that of the entire S&P 500 energy sector as stock prices hit all-time highs. The SPAC market is hot. The IPO market is hot (chart 5), credit markets are hot (chart 6), commodity markets are hot, the crypto markets are hot. Everything, it seems, is hot.” – bto: Es ist eben eine Assetpreisinflation!

Quelle: the market

→ themarket.ch: „The Bubble is Just Beginning“, 16. März 2021

Sehr gut anschließend an die heutige (bzw. gestrige) Diskussion noch ein interessanter Blickwinkel: relative Höhe der Zinszahlungen (gross interest expense/GDP-ratio). Aus diesem Blickwinkel könnte man die Dose noch eine Weile die Straße entlang treten…

https://klementoninvesting.substack.com/p/we-dont-need-inflation

Mit Blick auf Systemstabilität scheint mir “Zinszahlung / BSP” die deutlich geeignetere Kennzahl als “Schulden / BSP”.

Vielen Dank fuer den Link, interessante Webseite von JoachimK!

@ Thomas M.

Dank auch von mir.

Hochinteressant, was über die chinesischen Kredite geschrieben wird.

Leider ist in der Grafik Deutschland nicht einzeln aufgeführt.

Ich hatte mal eine Statistik gesehen, dass die Zinsausgaben vor 20-25 Jahren noch 20% des Bundeshaushalts ausgemacht haben.

Heute läge der Anteil bei rund 2%. Das ist schon brutal.

Beim IW habe ich eine Studie aus 2017 entdeckt, nach der die Zinsausgaben im Verhältnis zu den Steuereinnahmen etwa 6% ausmachen (2000 noch rund 14%). Auch diese Quote sollte heute deutlich niedriger liegen.

Die Stromgrößen avancieren zum alleinigen Gamechanger, weil das Rechnungslegungsregime für Bilanzkennzahlen duch Pippilangstrumpflkökonomie das Motto erfindet:

“Wir schaffen uns die Welt, wie sie uns gefällt!”

Bis der Strom versiegt, weil dieser ein konkretes Leistungsanreizsystem hinterlegt haben muss, um nicht an Beliebigkeit und Sinnlosigkeit zu vergehen.

>We think it likely that we’re in the foothills of a policy mistake of epic proportion which will have potentially devastating consequences.” – bto: Ich glaube nicht, dass es ein “Fehler” ist, sondern ein Vorsatz.>

Ich bin anderer Meinung:

Es ist weder ein Fehler, noch ist es Vorsatz, vielmehr ist es NOTWEHR.

Es ist natürlich richtig, auf die Assetpreise zu schauen und in der Entwicklung, die sie genommen haben, ein großes Problem zu sehen.

Es ist aber m. A. n. FALSCH zu glauben, dass J. Powell und andere bei der Fed sowie anderen Notenbanken sich dieses Problems NICHT bewusst sind.

Die sind nicht dümmer als der Autor und haben auch aus der Vergangenheit GELERNT.

Wenn der FOKUS in der öffentlichen Diskussion immer wieder NUR auf den CPI gelegt wird, dann ist das die RECHTFERTIGUNG für NOTWEHR.

Denn würden die Notenbanken nicht so sehr mit LIQUIDITÄT akkommodieren, gäbe es nicht nur einen Crash an den Assetmärkten, sondern auch REALWIRTSCHAFTLICH Verwerfungen in einem Ausmaß, das sich niemand so richtig vorstellen kann.

NUR Liquidität hält das System noch über Wasser.

Durch Liquidität gerechtfertigt zu akkommodieren, lässt sich nun einmal am GLAUBWÜRDIGSTEN mit BEZUG auf GEMESSENE Sachverhalte, d. h. mit Verweis auf den CPI argumentieren.

WIE gemessen wird, ist natürlich eine ganz andere Frage.

@Herr Tischer

“Denn würden die Notenbanken nicht so sehr mit LIQUIDITÄT akkommodieren, gäbe es nicht nur einen Crash an den Assetmärkten”

Na und?

“…sondern auch REALWIRTSCHAFTLICH Verwerfungen in einem Ausmaß, das sich niemand so richtig vorstellen kann.”

Uhh, niemand kann sich das richtig vorstellen, aber es ist bestimmt total gefährlich und schlimm! Jetzt hab ich aber richtig Angst.

Wenn schon Panikmache, dann bitte handwerklich besser gemacht. Das kann ja niemand ernst nehmen.

@ Richard Ott

Machen Sie sich nicht lächerlich.

SIE haben doch auch immer wieder die ALTERNATIVE im Blickfeld, die das heißt:

MASSENINSOVENZEN mit einem Heer von ARBEITSLOSEN.

Was damit verbunden sein kann, wissen wir aus dem letzten Jahrhundert.

Es ist zumindest eine REALISTISCHE Perspektive.

Von Panikmache kann da keine Rede sein.

Die Notenbanken MUSS man nun wirklich nicht loben.

Aber so zu tun, als würden sie verrückt spielen in einer Welt, in der man sich nichts SCHLIMMES und GEFÄHRLICHES vorstellen kann, ist schlichtweg albern.

@Herr Tischer

“MASSENINSOLVENZEN mit einem Heer von ARBEITSLOSEN. Was damit verbunden sein kann, wissen wir aus dem letzten Jahrhundert.”

Die wird es geben, und dann eine Zeit lang auch ein “Heer von Arbeitslosen”. Ich bin aber anders als die Notenbanken wenigstens so ehrlich, nicht zu suggerieren, dass sich das mit endlosem Gelddrucken abwenden ließe.

In Ostdeutschland lief nach 1990 genau der gleiche Prozess mit Masseninsolvenzen ab, brachte uns allerdings keinen Hitler sondern letztendlich eine Merkel ein, was wieder andere Gründe hatte. Und das Arbeitslosenheer ist gegenüber den 90ern deutlich geschrumpft.

Noch ein Beispiel: In USA gab es kurz nach dem 1. Weltkrieg eine schwere Rezession, als die Kriegswirtschaft wieder auf Normalproduktion umgestellt wurde – woraufhin die Zentralbank exakt gar nichts tat. Und 2 Jahre später war die Arbeitslosigkeit wieder unten:

https://2.bp.blogspot.com/-xN6h_M_yA8E/UvpEaI6redI/AAAAAAAAATE/GAIfiDQiI7Y/s1600/USunemployment19141929.png

“Die Notenbanken MUSS man nun wirklich nicht loben. Aber so zu tun, als würden sie verrückt spielen in einer Welt, in der man sich nichts SCHLIMMES und GEFÄHRLICHES vorstellen kann, ist schlichtweg albern.”

Oh, ich kann mir viel “Schlimmes” und “Gefährliches” vorstellen.

Nicht wettbewerbsfähige Unternehmen und überschuldete Staaten pleite gehen zu lassen, gehört aber in keine der beiden Kategorien, das ist allerhöchstens “unangenehm”, aber manchmal eben nötig.

@ Richard Ott

Zu Ihrem letzten Kommentar fällt mir nichts mehr ein.

>In Ostdeutschland lief nach 1990 genau der gleiche Prozess mit Masseninsolvenzen ab […]

Dieser Vergleich hinkt, weil das kollabierende Ostdeutschland vom intakten Westdeutschland aufgefangen wurde. Wenn die ganze EU abstürzt, wer fängt diese dann auf?

Im Prinzip wird die US-Situation in Teilen gerade simuliert. Viele Arbeitnehmer haben Lockdown-bedingt den Job verloren oder sind in Kurzarbeit. Mal gucken, ob es danach einen Boom gibt… bin skeptisch, aber immer offen für neue Fakten.

@Thomas M.

“Dieser Vergleich hinkt, weil das kollabierende Ostdeutschland vom intakten Westdeutschland aufgefangen wurde. Wenn die ganze EU abstürzt, wer fängt diese dann auf?”

Welche fremde Macht hat denn nach 1990 die zerbrechende Sowjetunion aufgefangen? Ich sage es Ihnen: Keine.

Das Leben dort war eine Zeit lang sehr unangenehm, von mir aus auch “schlimm”, aber es ging trotzdem weiter.

“Im Prinzip wird die US-Situation in Teilen gerade simuliert. Viele Arbeitnehmer haben Lockdown-bedingt den Job verloren oder sind in Kurzarbeit. Mal gucken, ob es danach einen Boom gibt… ”

Die bekommen aber üppige Finanzhilfen, manche haben mit der “Pandemic Unemployment Assistance” sogar mehr Einkommen als vorher. Und die meisten ihrer Jobs sind zeitweilig verschwunden, weil die Regierung ihnen die Berufsausübung wegen Infektionsschutz verboten hat, nicht weil das Geschäft an sich unter Normalbedingungen nicht funktionieren würde. Ein wirklich aufschlussreicher Vergleich ist das nicht.

@Herr Tischer

Fällt Ihnen zu der “Post-World-War-I-Recession” in den USA, die ohne Zentralbankintervention vorbei ging, auch nichts ein?

Dieser Disput zwischen Ihnen beiden ist mindestens eine Wiederholung.

Und wieder weise ich daraufhin, dass der “Nowehr-Weg” niemals zu einem guten ende führen kann und auch nie konnte. Durch diese Politik und Geldpolitik wird das Ende jeden Tag schlimmer.

Allerdings hat sich die Sachlage seit der “Uraufführung” doch ein wenig verändert: es gibt kein Zurück mehr. Und unter dieser Prämisse kann auch nicht mehr seriös abgeschätzt werden, ob es nun wirklich immer schlimmer oder nur anders schlimmer wird.

@ Felix

Ist ja richtig, was Sie sagen.

Was ich versuche, KLAR zu machen:

Die Notenbanken haben einen HINREICHENDEN Grund, die Geldpolitik zu betreiben, die sie betreiben.

Angesichts der Mittel, die Sie haben, KÖNNEN sie NICHT sagen:

Es geht eh alles die Bach runter, je eher, desto besser.

Sie MÜSSEN versuchen, die Lage so stabil zu halten, wie sie es vermögen.

Heißt:

Es wird als IHRE Aufgabe von Ihnen selbst und denen, die sie als Institution geschaffen haben, angesehen, dass sie die ERKENNTLICH schlechtere Situation, d. h. den unmittelbaren Kollaps des Systems VERHINDERN, auch wenn das System immer UNSTABILER werden sollte – möglicherweise gerade auch DURCH Ihre Maßnahmen, hier die Geldpolitik.

Beispiel für diese Commonsense-Logik:

Ein Boot ist leck und läuft voll Wasser.

VERNÜNFTIGE Menschen schöpfen Wasser aus dem Boot so lange wie sie es können.

UNVERNÜNFTIGE lehnen sich zurück und sagen sich:

Na ja, da saufen wir halt ab.

Ich habe keine Lust, mich dauernd zu wiederholen.

Aber offensichtlich BEGREIFEN manche nicht die SITUATION und daher auch nicht, WARUM so gehandelt wird, wie gehandelt wird.

@Herr Tischer

Da bringen Sie wieder die unzutreffende Analogie vom sinkenden Boot an.

Ich antworte mit der Analogie vom Alkoholsüchtigen, dem es dreckig geht, weil er nichts mehr zu saufen hat, dem Sie aber eine Flasche Schnaps geben um “seine Lage stabil zu halten”. Da geht es ihm gleich viel besser! Sie haben damit seinen “unmittelbaren Kollaps” verhindert, ganz, ganz toll.

Aber Felix hat recht, das hatten wir alles schon mal, und da sind wir von einem Konsens weiter entfernt als je zuvor.

@ Richard Ott

>unzutreffende Analogie vom sinkenden Boot>

Sie haben das Problem NICHT verstanden.

IHRE Analogie zeigt dies.

Es geht nicht um Alkoholsüchtige einerseits und die normalen Übrigen andererseits.

Es geht um ALLE im System.

Wenn die Notenbanken die Liquiditätsversorgung einstellen, dann platzen nicht nur die Assetblasen und den reichen „Süchtigen“ geht es dreckig.

Sondern es entsteht ein Heer von Arbeitslosen, weil Firmen ohne Zahl aufgeben MÜSSEN.

Wann kapieren Sie es endlich:

Die Notenbanken STABILISIEREN das SYSTEM und nicht nur ein paar Süchtige, die nichts mehr zu saufen haben.

@R. Ott

Falls es hilft, in Ihrem Bild: Stellen Sie sich eine Welt vor, in der ALLE alkoholkrank sind und niemand weiß, wie man eine Kette verkraftbarer Teilentzüge herstellen kann, sondern die Kur der kalte Entzug aller gleichzeitig ist.

Was tun? (und jetzt mit einer Dosis Realität: Diese „Alkoholsucht“ ist das beste System mit dem höchsten Massenwohlstand, das es je gab. Wer startet den Entzug und warum? Wer wird ihn verhindern wollen?)

@Herr Tischer

“Sondern es entsteht ein Heer von Arbeitslosen, weil Firmen ohne Zahl aufgeben MÜSSEN. Wann kapieren Sie es endlich: Die Notenbanken STABILISIEREN das SYSTEM und nicht nur ein paar Süchtige, die nichts mehr zu saufen haben.”

Sie lügen sich in die eigene Tasche.

Irgendwann entsteht das Heer von Arbeitslosen sowieso, und es wird umso größer, je länger Sie die “Systemstabilisierung” fortsetzen. Sie erkennen ja selbst an, dass die angebliche Stabilisierungspolitik nicht unbegrenzt lange fortgeführt werden kann.

Und das Heer der Arbeitslosen wird neue Arbeit finden, selbst nach einem totalen Zusammenbruch wie in der Sowjetunion war das so.

Möchten Sie einfach nur, dass die unangenehmen Konsequenzen nicht mehr zu Ihren Lebzeiten auftreten und sich irgendwann jemand anderes mit dem Problem befassen muss?

@Christian Anders

“Stellen Sie sich eine Welt vor, in der ALLE alkoholkrank sind und niemand weiß, wie man eine Kette verkraftbarer Teilentzüge herstellen kann, sondern die Kur der kalte Entzug aller gleichzeitig ist. Was tun?”

*ALLE*? Sehr unrealistisch. Selbst zu den Hochzeiten des Opiumkonsums in China waren nur schätzungsweise 10% der Bevölkerung opiumsüchtig.

Aber wenn es so wäre, dann wäre die Konsequenz auch nicht schwer vorherzusehen:

Je länger Sie die Säufer mit Schnaps versorgen “um sie zu stabilisieren”, desto mehr von ihnen werden letztendlich sterben – nur nicht sofort, was Ihr “Erfolg” mit Ihren “Staibilisierungsmaßnahmen” ist.

Je schneller Sie den kalten Entzug beginnen, desto mehr werden überleben.

“Diese ‘Alkoholsucht’ ist das beste System mit dem höchsten Massenwohlstand, das es je gab.”

Unser System schafft den hohen Lebensstandard *trotz* der Liquiditätsversorgung für Insolvente durch die Zentralbank, nicht *wegen* ihr.

Oder glauben Sie ernsthaft, wir sind so “reich”, weil wir so viel Geld drucken?

” Wer startet den Entzug und warum? Wer wird ihn verhindern wollen?”

Die mächtigsten Interessengruppen, die den Entzug verhindern wollen, sind natürlich die Süchtigen und die Händler und Hersteller des Suchtmittels.

Bei Ihrer Version der Analogie, wo ausnahmslos alle, also auch die Hersteller und die Händler drogensüchtig sind (für Drogendealer ein echter Anfängerfehler, tss…), ergibt das nicht mehr viel Sinn, aber beim historischen Szenario “Opiumsucht in China” war offensichtlich, wer profitierte:

Die Briten als Hersteller und Händler des Opiums, und dazu noch eine bestimmte Fraktion innerhalb der chinesischen Elite, die auch im Opium-Business war.

Den kalten Entzug durchgezogen hat übrigens Mao, und zwar mit äußerst rabiaten Methoden. Wenn er es nicht getan hätte, wäre China heute wahrscheinlich immer noch ein Vasallenstaat der Briten, oder vielleicht mittlerweile der Amerikaner. (Das möchte ich gerne erwähnen, weil mir hier so oft vorgeworfen wird, ich sei ein ganz böser Kommunistenfresser…)

@ ch anders 04:21 >>Wer startet den Entzug und warum? Wer wird ihn verhindern wollen?)<<

…….. wer sollte den entzug verhindern wollen, wenn keiner ihn will??

nun, andererseits ist corona vielleicht eine gewisse analogie im entzug?

-das angebot und der verbrauch wird/wurden runter gefahren.

-die verschuldung wurde massiv erhöht und die finanz-assets steigen

-neben der laufenden assets-inflation, ist auch die inflation in der realwirtschaft angekommen.

die reduktion auf der einen seite, erhöht den kaufkraftverlust auf der anderen seite.

soll sowas eine heilung bringen? niemals!

die inflation wird die kaufkraft abwürgen bis die wirtschaft kollabiert.

(auch die historie hat es mehrfach schon gezeigt)

es ist schon erstaunlich, wie ignorant man den relativ einfachen zusammenhängen, gegenüber steht.

aber das ist ja der garant, dass die geschichte (mit moderneren mitteln) sich wiederholt!

@R. Ott

„ *ALLE*? Sehr unrealistisch. Selbst zu den Hochzeiten des Opiumkonsums in China waren nur schätzungsweise 10% der Bevölkerung opiumsüchtig.“

Toll. Ich baue eine Analogie auf Grundschulniveau und Sie verstehen es immer noch nicht. Herrn Tischers Resignation ist mehr als nachvollziehbar.

Warum ALLE? Weil JEDER vom Umsatz abhängt, der bereits dann für ALLE jede Schmerzgrenze knackt, wenn „nur“ 10% ausfallen. Eine Analogie aus der Physik wäre „Kettenreaktion“…

„Bei Ihrer Version der Analogie, wo ausnahmslos alle, also auch die Hersteller und die Händler drogensüchtig sind (für Drogendealer ein echter Anfängerfehler, tss…), ergibt das nicht mehr viel Sinn,“

Huch! Ich ziehe zurück: Sie haben es ja doch verstanden. Ja. Genau so ist es. ALLE. Sogar die Dealer und Hersteller. Verknüpft über den o. g. Mechanismus.

@Christian Anders

” Ich baue eine Analogie auf Grundschulniveau und Sie verstehen es immer noch nicht.”

Das Problem scheint mir eher zu sein, dass Sie wirtschaftliche Szenarien grundsätzlich nicht begreifen können und da nichtmal Analogien auf Kindergarten-Kaufmannsladen-Niveau beim Erklären helfen.

“Warum ALLE? Weil JEDER vom Umsatz abhängt, der bereits dann für ALLE jede Schmerzgrenze knackt, wenn „nur“ 10% ausfallen.”

Was wollen Sie mir mit dem Satz sagen?

Etwa: “JEDER geht pleite, wenn er 10% weniger Umsatz macht?”

Das ist ja völliger Unsinn, wie sind Sie denn auf diese Idee gekommen?

@ Richard Ott

>Irgendwann entsteht das Heer von Arbeitslosen sowieso, und es wird umso größer, je länger Sie die “Systemstabilisierung” fortsetzen.>

Was irgendwann entsteht, ist offen.

Aber selbst wenn ABSOLUT sicher wäre, dass IRGENDWANN ein Heer von Arbeitslosen entsteht, ist das KEIN Grund für die Notenbanken es HEUTE entstehen zu lassen.

Sie WOLLEN es NICHT kapieren:

NIEMAND, der bei Verstand ist, führt HEUTE etwas herbei, das von den Betroffenen als sehr nachteilig angesehen wird, weil es IRGENDWANN doch stattfindet.

JEDER Vernünftige sucht das HEUTE-NACHTEILIGE zu VERHINDERN.

Erst DANN, wenn es NICHT mehr zu verhindern ist, findet es statt – WEIL es eben nicht mehr zu verhindern war.

Das ist die ÜBERLEBENSLOGIK oder der gesunde Menschenverstand vom Kindergarten bis zu den Zentralbanken.

This is probably why the mistake was repeated.” – bto: und zwar mehrfach und immer größer. Das muss man erst mal hinbekommen!

Wer sagt denn, dass das unerwünscht war/ist? Vielleicht sind die Krisen ja gewollt?

Vielleicht ist es ein bisschen wie in einer tragischen Familie: Die einen Kinder bekommen alles, werden gehaetschelt und gepflegt, gefuettert und gepampert [Asset-Owners], andere dagegen werden vernachlaessigt, uebersehen, versteckt [Sparbuch-Sparer, Mieter, Kollateral-Ausbader]. Irgendwann bricht sich die Tragik Bahn und es kommt zum Brudermord … oder Great Reset?

Nur, ein Platzen der Blasen hilft keinem, (fast)alle werden verlieren?

Wir braeuchten ein geordnetes, geplantes, reguliertes Luftablassen? Ein langsames Pfffffffftt.

Warum nicht die (kurzfristigen) Zinsen auf Staatstitel in der EU von der EZB geordnet ueber 5 Jahre auf 1% schleussen? Die 10jaehrigen mittels Zinsstrukturkurven-Kontrolle im gleichen Zeitraum auf 2,5% bringen und dort fixieren?

Dann wuerden die Assetmaerkte abdiskontieren (hoffentlich nicht mit einem Knall?), und die “Kinder” waeren wieder naeher beieinander?

Jetzt ihr: “das ist Bloedsinn, weil …”?

LG Joerg

@Joerg

“Jetzt ihr: ‘das ist Bloedsinn, weil …’?”

Na die üblichen Verdächtigen werden gleich kommen und Ihnen das Märchen erzählen, dass die Notenbanken die Zinsen doch überhaupt nicht beeinflussen können. :D :D :D

“Warum nicht die (kurzfristigen) Zinsen auf Staatstitel in der EU von der EZB geordnet ueber 5 Jahre auf 1% schleussen? Die 10jaehrigen mittels Zinsstrukturkurven-Kontrolle im gleichen Zeitraum auf 2,5% bringen und dort fixieren?”

Ich fände es schon extrem interessant, zu sehen, was passiert, wenn die Notenbaken ihre riesigen Staatsanleihen-Ankaufsprogramme einstellen. (Beispiel aus der EZB-Buchstabensuppe: 1850 Milliarden Euro durch das “Pandemic Emergency Purchase Programme (PEPP)”)

@Hr Ott

“was passiert, wenn die Notenbaken ihre riesigen Staatsanleihen-Ankaufsprogramme einstellen. (Beispiel aus der EZB-Buchstabensuppe: 1850 Milliarden Euro durch das “Pandemic Emergency Purchase Programme (PEPP)”)”

Naja, diese Ankauf-Feuerkraft wird auch noetig sein, um kurzfristige 1% und 10jaehrige 2,5% herzustellen und zu halten. Vielleicht auch mehr. Nur gaebe es weniger Streit unter den “Kindern”?

“Freier Markt” waere trotztdem nicht – der kaeme, wenn ueberhaupt, erst NACH einem Reset? (den keiner will – Schmerzvermeidung!)

@Joerg

“Naja, diese Ankauf-Feuerkraft wird auch noetig sein, um kurzfristige 1% und 10jaehrige 2,5% herzustellen und zu halten”

Wieso “Ankauf-Feuerkraft”?

Wenn Sie wollen, dass die Zinsen von Staatsanleihen steigen (das bedeutet, dass ihre

Kurse sinken), dann muss die Zentralbank aus ihrem riesigen Portfolio welche *VERKAUFEN*.

“Wenn Sie WOLLEN, dass die Zinsen von Staatsanleihen steigen (das bedeutet, dass ihre Kurse sinken), dann muss die Zentralbank aus ihrem riesigen Portfolio welche *VERKAUFEN*.”

[also ICH WILL es nicht, aber es war die Frage im DS-Leitartikel, wie man die Spreizung zwischen Asset-Blase? einerseits und “wohlstands-abgehaengten” Buergern? andererseits schliessen koennte]

OK, ein paar Staatsanleihenverkaeufe vielleicht als Priming/PoC? Vermutlich reicht aber das blosse Ankuendigen von flexiblem “Nicht-Mehrkaufen” ueber kurz oder lang aus?

Vermutlich klappt es bei den zukuenftigen Euro-Bonds auch besser … sonst hat man wieder diese laestige Spreizung: Italienische 10j schiessen auf 3% und deutsche duempeln dann trotzdem bei 0,1% herum?

@Joerg

Oh, ich dachte, Sie hätten sich den Vorschlag zueigen gemacht. Aber geschenkt, die Arugmentation funktioniert auch, wenn Sie die Sätze entpersonalisieren.

“OK, ein paar Staatsanleihenverkaeufe vielleicht als Priming/PoC? Vermutlich reicht aber das blosse Ankuendigen von flexiblem “Nicht-Mehrkaufen” ueber kurz oder lang aus?”

Das ist genau die Frage, die ich mir stelle. Ich würde vermuten, dass der Einfluss auf die Stimmung und die Psychologie des Marktes enorm groß wäre.

Die Notenbanken werden ihre Ankaufprogramme von Staatsanleihen noch lange nicht einstellen, höchstens etwas verlangsamen. Sie haben nämlich aus den Fehlern der 1930-Jahre gelernt, nehme ich an.

Grüße Erich Pitak, Autor von “DAX 19.000”.

@Joerg

Die Asset-Owners werden ja nicht *direkt* gehätschelt; die steigenden Kurse und teilweise irrwitzigen Bewertungen sind die Konsequenz von größeren Entwicklungen wie langfristig fallenden Zinsen oder m.E. auch, dass mehr Leute global zu Wohlstand kommen und Geld in relativ wenige Einzeltitel stecken. (Letzteres ist meine private Hypothese als *ein* Faktor.)

Dass alle Bewertungen “weiß-glühend” sind, halte ich für übertrieben. Wenn man abseits von IPOs, SPACs und Modetiteln guckt, ist jede Menge in Relation zum niedrigen Zinsniveau “ordentlich” bewertet.

Das langsame Luftablassen wäre die Inflation; so sie denn kommt und sich kontrollieren lässt.

>Warum nicht die (kurzfristigen) Zinsen auf Staatstitel in der EU von der EZB geordnet ueber 5 Jahre auf 1% schleussen? Die 10jaehrigen mittels Zinsstrukturkurven-Kontrolle im gleichen Zeitraum auf 2,5% bringen und dort fixieren?

Dann wuerden die Assetmaerkte abdiskontieren (hoffentlich nicht mit einem Knall?), und die “Kinder” waeren wieder naeher beieinander?

Dann müssten den Kindern aber die Steuern erhöht oder die Goodies reduziert werden. Irgendwer muss ja diese höheren Zinsen zahlen. Und evtl. klappt manch ein Unternehmen zusammen, was seine Kredite tilgt durch Neu-Kreditaufnahme.

Die ZB können allerdings auch nicht die Zinsen direkt beeinflussen. Ich schätze, während ich hier tippe, antwortet Herr Stöcker auch schon ;)

@ThomasM Danke,

Asset-Bewertung angemessen relativ zu Zinsniveau = OK

Andere pers. Meinung:

“langsame Luftablassen wäre die Inflation”

Im Sinne von den Unterschied zwischen Asset-Ownern und und Wohlstands-(bald)Abgehaengten (Sparbuch/privLV/privRV/bAV/Riester/Ruerup) vermindern, waere eine hoehere Inflation eben genau die falsche Loesung (unruhestiftend/risikoreicher)? Deshalb die These von hoeher gesetzten Zinsen (statt -0,5% eben >0% fuer Sichteinlagen und 1-2% fuer 10j).

Im Prinzip waere es vernuenftig und wir werden hoffentlich in der EU auch noch dahin kommen.

Wenn die Amerikaner und Japaner keine Deppen sind, machen die es ja schon besser als wir (also nicht/kaum negativ, kurzfrist zwischen -0,1 und 0,25% sowie 10j zwischen 0,0 und 2%), das wird sich bei uns auch noch durchsetzen … vielleicht sind jedoch EUR-Bonds dazu eine Voraussetzung?

“Dann müssten den Kindern aber die Steuern erhöht oder die Goodies reduziert werden.”

Da will ich gerne dazulernen, wieso ist das zwangslaeufig der Fall? Der Staat kann doch erstmal auch bei niedrigen, positiven Zinsen so weitermachen wie bisher (Transfers aus Steuern, Investieren, Zinsen begleichen)? Also, das Land erneuern, die Wohlstands-Abgehaengten pampern, im groben das Prinzip “wir schuetten alle Probleme erstmal mit Geld zu und kicken die Dose die Strasse hinunter” beibehalten?

“Die ZB können allerdings auch nicht die Zinsen direkt beeinflussen”.

Wir brauchen hier nicht schwarz/weiss zu diskutieren (Hr Stoecker ist noch im Meeting? ;-)), aber wenn die EZB auf Einlagen etwas Zins gibt, und gleichzeitig die Zinsstrukturkurve mit Anleihe-Transaktionen (Kaeufe/Verkaeufe) in gewuenschten Korridoren haelt, ist eine Zins-Beeinflussung schon etwas moeglich, oder? (“Believe me, it will be enough”)

@Joerg:

Inflation scheint mir der Weg mit dem geringsten Widerstand für die Entschuldung zu sein. Daher dürfte es darauf hinaus laufen. Ist zumindest meine “Wette” losgelöst davon, ob es fair wäre oder nicht (siehe hierzu auch noch weiter unten…)

>>“Dann müssten den Kindern aber die Steuern erhöht oder die Goodies reduziert werden.”

>Da will ich gerne dazulernen, wieso ist das zwangslaeufig der Fall? Der Staat kann doch erstmal auch bei niedrigen, positiven Zinsen so weitermachen wie bisher (Transfers aus Steuern, Investieren, Zinsen begleichen)?

Bei steigenden Zinsen steigen doch die Zinsausgaben des Staatshaushalts. Diese Mehrausgaben müssen dann entweder über die Wege höherer Steuern, Reduktion der Ausgaben oder (zusätzlicher) Neuverschuldung bedient werden.

Ich gehe übrigens auch davon aus, dass die ZB sehr wohl die Zinsen *in Teilen* beeinflussen können und dies tun. Sie können dafür sorgen, dass die Zinsen nicht über einen bestimmten Wert steigen. Sie können natürlich niemanden direkt zwingen, Anleihen zu kaufen und insofern auch keine Zinssteigerung auf beliebige Werte direkt durchsetzen.

Negativzinsen beim “Endanwender” auf dem Konto halte ich für kontraproduktiv. Meinem bescheidenen auf der Praxis fußenden Modell zufolge ändert sich das Verhalten nicht stetig bei sinkenden Zinsen, sondern grundlegend bei Erreichen von negativen Zinsen. Bei Positivverzinsung schiebe ich Geld *gezielt* dorthin, wo es Zinsen gibt, bei Negativverzinsung schiebe ich es *irgendwo* hin, wo es nicht mehr negativ verzinst ist.

Eine Investition im Unternehmen wird ja nicht attraktiver und fehlende Möglichkeiten zur Investition ergeben sich nicht, wenn das Geld auf einmal vom Konto verschwindet. Vielleicht macht man auch noch ein Konto auf, flüchtet gleich ganz aus der Währung in andere Währungen oder Sachwerte. Mag ja sein, dass das auch den Konsum und Investitionen etwas steigert; aber am Ende des Tages resultieren aus negativen Zinsen beim “Endanwender” (nicht bei den Banken) m.E. in erster Linie nur unkontrollierbare Ausweichbewegungen.

Ich fände von Seiten der Regierung übrigens folgende Sachen gut (Achtung festschnallen, wilder kapital-sozialistischer Mix), um Chancen zu schaffen, mit den ungleichen Startbedingungen und den schwieriger werdenden Vorsorgebedingungen umzugehen.

– Wertpapier-Altersvorsorgesparkonten wie in den USA (IRA); darin kann man Wertpapier steuerfrei verwalten und bezahlt erst Steuern im Alter

– inflationsausgleichende Schatzbriefe für Kleinsparer; können nur von Bürgern bezogen werden, Menge ist limitiert

– Bürgschaft der Komune/des Landes beim Erwerb des eigenen Daches über dem Kopf für Leute ohne Kapital im Rücken; Quasi “Eigentums-Bafög”

Davon wird natürlich nichts kommen, weil es “oben” kein Interesse geben dürfte und zuviele Interessensverbände dagegen arbeiten würden.

Von Substanzbesteuerung halte ich aus Prinzip nichts. Das könnte ich versuchen zu begründen, aber am Ende des Tages liegt das an meiner Präferenz für Eigentumsrechte und der Rolle des Staates.

Danke, @ThomasM

“Bei steigenden Zinsen steigen doch die Zinsausgaben des Staatshaushalts. Diese Mehrausgaben müssen dann entweder über die Wege höherer Steuern, Reduktion der Ausgaben oder (zusätzlicher) Neuverschuldung bedient werden.”

Ja, klar; gucken Sie nach JAP, USA, einfach (noch) mehr Neuverschuldung: tut (scheinbar) nicht weh und geht immer weiter (solange in eigener Waehrung erfolgt und in halbwegs gesunder Relation zum inlaendisch gehaltenen Vermoegen bleibt)?

Wenn dann Inflation nur troepfelt (= Konsens?) statt ketchup-blobbt (=Doom&Gloom), geht’s bis zur naechsten Waehrungsreform auch gut ;-)

Sonst alles einverstanden.

Zu “Wertpapier-Altersvorsorgesparkonten” gute Chancen, dass es mal ueber die EU kommt und dem Michel so geholft wird?

Motto: “Was der kl. Michel nicht kann, wird ihm die Uschi schon noch beibringen”

LG Joerg

@Joerg

Gerne und Danke zurück! Das Ketchup-Flaschen-Bild gefällt mir gut: Erst kommt nix, nur ein paar Tropfen. Man klopft kräftigt und dann macht’s auf einmal “blob”…

Wertpapier-Altersvorsorgesparkonten: Wenn Blackrock in Brüssel gut lobbyt? Wer weiß ;)

@ thomas 15:40 >> Inflation scheint mir der Weg mit dem geringsten Widerstand für die Entschuldung zu sein. Daher dürfte es darauf hinaus laufen. <<

……… das denke ich auch!

Aber: es ist egal, wie das ding gedreht wird:

ob inflation, oder schuldenbremsen (auch weniger schuld-papier aufkauf etc. usw.)

beides führt zu einer wachstumsbremse der wirtschaft und des kapitals.

dieses exponentielles system hält eine anhaltende wachstumsbremse nicht aus. es kollabiert dann in wenigen jahren.

die inflations-variante ist die wahrscheinlichste, weil auch in dieser inflationszeit noch unheimlich viel (rest-) vermögen aus der realwirtschaft hin zu dem finanzkapitals-sektor umverteilt wird.

dies ist ja gerade der zweck des herrschaftlichen kreditgeldsystems!

mit jeder anderen "lösung", würde der zweck des geldsystem kontakariert.

schuldenstreckungen etc. sind nur scheinlösungen und psychologisch gut fürs volk.

das volk zahlt alles!!!!, egal welchen weg die macht-eliten gehen werden!

Sehe auch noch superviel Aufwärtspotential bei den Börsen! Venezuela macht vor, welche immer neuen Höchststände man erreichen kann, wenn man einfach nur genug Geld druckt:

http://www.acting-man.com/blog/media/2018/09/5-IBC-Index-Caracas.png

(bitte nicht übersehen: die Skala ist logarithmisch…)

@Herrn Richard Ott:

Ich habe gerade ein Gedankenexperiment gemacht. Setze Annalena Baerbock vor einen solchen logarithmischen Chart und überlege, was passiert, wenn es sich um die Eurozone handelt. Das Ergebnis meines Gedankenexperiments war: es passiert nichts. Die Schmetterlinge müssen genauso gerettet werden wie ohne Geldmengenanstieg und die Kosten für Trampoline steigen langsamer als für Medikamente, weil man den Konsum von Trampolinen schieben kann. Alles ist gut!^^

@Frau Finke-Röpke

Von Baerbock würde ich dann erwarten, dass sie schnell Mindest- und Höchstpreise für den Aktienmarkt und auch sämtliche andere Produkte vorschreibt. In Venezuela bringen sich die Leute ja mittlerweile auch wegen einem geschlachteten Hühnchen um, weil die Lebensmittelpreise so hoch sind – das kann man mit Preiskontrollen ganz offensichtlich effektiv verhindern (und außerdem sollten die Leute sowieso weniger Fleisch essen, schon fürs Kliemer)…

Kanzlerkandidat Scholz würde den Chart aber auch nicht kapieren, der legt sein ganzes Geld ja bekanntlich auf dem Sparbuch an und bekommt später sowieso eine Pension vom Staat.

Seine Neffen sind besonders lustig: https://www.t-online.de/finanzen/news/unternehmen-verbraucher/id_89632332/neffen-von-olaf-scholz-unser-onkel-scheut-den-aktienmarkt-.html

Laschet traue ich auch nicht viel zu, aber immerhin wird er mittlerweile vom Blackrock-Merz beraten, der das Problem zumindest begreifen müsste.

@Herrn Richard Ott:

Wenigstens hat bei den Neffen von Herrn Scholz die Erziehung funktioniert.

Und ja, ich traue Frau Baerbock auch zu, dass sie glaubt, durch staatliche Preisfestlegungen den Mangel beseitigen zu können.

Leider war sie in der Jugend Trampolinspringen. Verstärkte Aktivitäten bei Trödel- oder Flohmärkten hätten wahrscheinlich mehr wirtschaftliches Verständnis vermittelt. Bei Herrn Laschet setze ich weniger auf Herrn Merz als vielmehr auf seinen eher konservativen Berater und Staatskanzleichef Nathaniel Liminski, der ein ganz anderes Kaliber ist, aber halt nicht öffentlichkeitstauglich. Der könnte wirklich ein marktwirtschaftliches Profil entwickeln, muss aber – weil NRW – in der nächsten Regierung im Hintergrund bleiben, selbst wenn die Union Teil der Regierung werden wird.

@ >>Die Blase ist erst am Anfang – meint Dylan Grice <<

was denn sonst!

solange dieses kreditgeldsystem besteht, gibt es keine andere möglichkeit, als aufbau und zerstörung.

die politik hat nur die möglichkeit die systemisch, unvermeidbare blasenbildung, langsamer, oder schnneller mit luft zu füllen, also zeit gewinnen, mehr nicht.

alles andere zu diskutieren und sogar glauben machen wollen, dass es dazu eine lösung dazu gibt, ist verlorene lebenszeit und noch dazu vorsätzlich gefährlich und falsch.