“We’ve hit a cyclical peak”

Meine Haltung zu den FANGs ist bekannt. Ich denke, sie sind das Symbol für die Endphase des Bullenmarktes. Eine Trendwende in diesen Aktien dürfte das Signal für die Trendwende des gesamten Marktes sein.

In die gleiche Richtung gehen die Überlegungen von Dave Rosenberg von Gluskin Sheff, die über John Mauldin/Zero Hedge breiter verfügbar wurden:

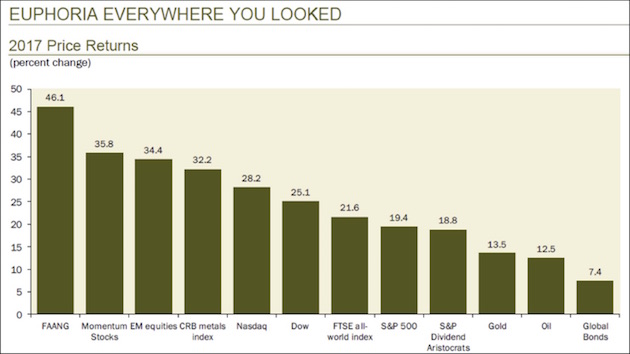

- “The FAANG stocks (…) have ruled the technology sector the last few years and have wielded a heavy influence on the entire stock market. Apple is the world’s most valuable company by market capitalization, with Amazon and Google not far behind. So anyone indexing US large-cap equities – which means almost anyone with investment capital – simply must own them.” – bto: Und wer den Markt übertreffen wollte, musste sogar noch ein Übergewicht an diesen wenigen Aktien haben.

- “Owning the FAANGS was a big help in 2017. (…) Last year pretty much everything went up, but not equally.” – bto: eine wirklich beeindruckende Performance, die als solches nichts darüber aussagt, ob es berechtigt ist oder nicht. Insofern passt der Titel auch nicht. Starke Kursgewinne müssen nicht gleichzusetzen sein mit “Euphorie”.

- “As you can see, the FAANG stocks outperformed other stock benchmarks as well as gold, oil, and bonds. (…) But Dave went on to demonstrate why 2018 or 2019 could be quite different, using four different S&P 500 valuation metrics: Forward Price to Earnings Ratio, Price to Sales Ratio, Price to Book Value Ratio, Enterprise Value to EBITDA Ratio (…) Here’s the result for P/E ratio.” – bto: Das wissen wir schon lange und eine hohe Bewertung als solche ist noch kein Grund für einen Crash. Bekannt.

- “The S&P 500 forward P/E ratio has been below its present level 83% of the time since 1990. Repeating that exercise for the other three metrics and then averaging them, Dave found the index is presently at a 92nd percentile valuation event. (…) In other words, only 8% of the time in the past has the stock market in the United States been as richly priced as it is today. And if you want to come up with reasons why that’s the case, that’s fine. But just understand that we are extremely pricey. We’re more than just a one standard deviation event versus the historical average.” – bto: Und das kann, wie ich bereits mehrfach erläutert habe, nicht mit den tiefen Zinsen erklärt werden!

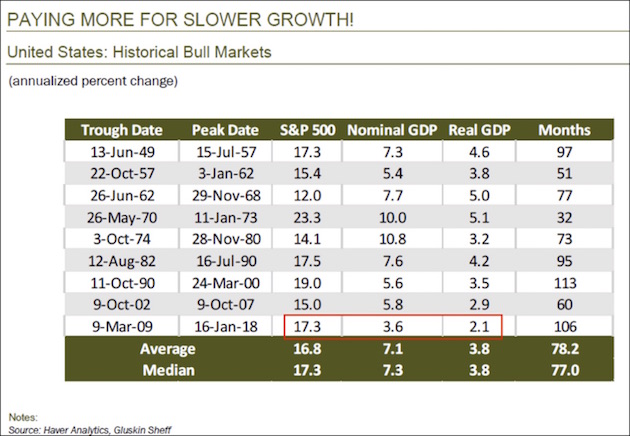

- “Dave then showed this surprising table, comparing historic bull markets with GDP change during the same period.” – bto: Auch das ist natürlich ziemlich bekannt. Schön wäre noch, wenn man den Anstieg der Schulden in die Tabelle aufnehmen würde. Dann würden wir sehen: immer mehr Schulden, immer schönere Börsen, immer weniger Wirkung auf das BIP.

- “(…) how is it that stocks rose the same amount on half as much economic growth? Dave said that if the stock-GDP ratio today had remained what it was back then, the S&P 500 would be around 1,550 today.” – bto: was deutlich weniger ist!

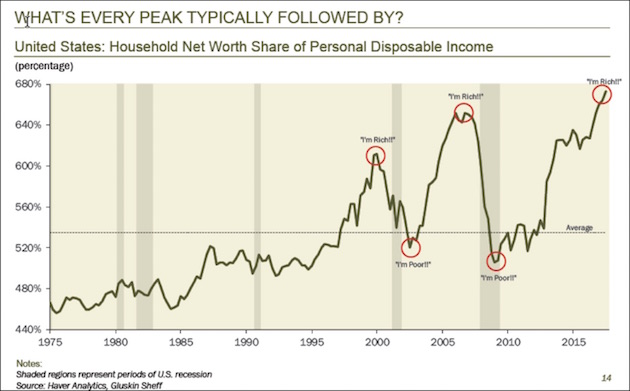

- (…) household net worth as a percentage of disposable income. (…) was in 1999–2000 and again in 2006–2007, (…) near a peak, and people felt good. The good feelings didn’t last. Both times the ratio corrected back below its long-term average.” – bto: weil es jedes Mal zu einer noch größeren Krise kam.

- “Whenever it happens, the next downturn will be something new: the first socially networked recession and bear market. It’s hard to believe now, but Facebook and Twitter were both just infants in 2007. Smartphones were still a high-end luxury item, too. We are now tied together in ways we were not back then. Those connections will make the experience quite different, so it’s worth talking about networks.

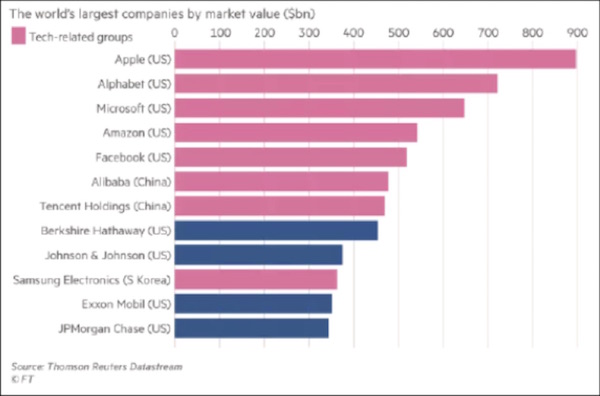

- “As we saw above, the stock market is overvalued by many different measures. (…) What drove valuations higher? Many reasons, but the FAANG companies are primary.” – bto: Sie stehen auch für 27 Prozent vom S&P 500.

- “Tech stocks – including all the FAANG names except Netflix – were 8 of the world’s 12 most valuable companies when FT made this chart last year. If several of these stocks start rolling over, the global bull market will be hard to sustain – and it’s already under assault for entirely different reasons, like rising interest rates, a potential trade war, and the overdue US recession.” – bto: So ist es.

→ zerohedge.com: “These Five Indicators Signal That We’ve Hit A Cyclical Peak”, 31. März 2018

Beim nächsten Crash wird wohl kaum der Euro als Fluchtwährung dienen und wie dann die Schweizer Notenbank sich gegen den Aufwertungsdruck fü den Franken stemmen will möchte ich gerne mal sehen.

Sollten die SNB dann mit gedrucktem Geld Aktien werthaltiger Unternehmen mit hinreichend Cashflow zu Substanzwertpreisen kaufen gibt es Schlimmeres das sie dem Steuerzahlen zumunten könnte. Wie Schlimmeres geht da muß man nur nach Deutschland blicken.

Ich mag mich irren, aber hat die Schweizer Notenbank SNB nicht ganz erheblich in die FANGS “investiert”.

Sie dürfte damit erheblich zu einer Überbewertung beigetragen haben.

Da die SNB das Geld dafür selber druckt, dürften ihr Kursverluste auch eher egal sein, Hauptsache der Schweizer Franken sinkt und die Schweiz kann ihr Exportmodell weiter fortführen.

Erinnert mich an die grosse Depression. Erst Börsencrash, dann Währungskrieg und dann Handelskrieg. Wiederholt sich irgendwie. Im Unterschied zu damals haben die Notenbanken durch QE uns Zeit gekauft. Ich fürchte nur sie haben den Mühlstein der uns am Hals hängt höher geschoben und jetzt fällt er um so tiefer.

Wenn man physisch short geht stehen begrenzten Gewinnen theoretisch unbegrenzte Verluste gegenüber. Das können sich in der Regel nur Hedgefonds oder andere institutionelle Anleger leisten.

Die Mutter aller Shorts ist ja laut einem amerikanischen Hedgefondmanager derzeit Tesla. An Tesla konnte man auch bisher schön sehen das der Markt länger irrational sein kann als man selbst liquide (Keynes).

Alle Shortwetten sind bisher an Tesla abgeprallt und die Jünger (Tesla hat keine Aktionäre die rechnen können) treiben Tesla immer wieder auf neue oder alte Höhen egal wie beschissen die Zahlen sind.

Gerade wieder schön zu beobachten gewesen erst fällt Tesla innerhalb von 2 Tagen um fast 20% dann behauptet Musk alles sei toll und man habe in einer Woche 2020 Model 3 gebaut, rums schon überschreitet Tesla genauso schnell die gerade gerissene 300 Dollar Marke. Da braucht man als Shortseller schon sehr starke Nerven und tiefe Taschen.

Eine weniger gefährliche aber auch sehr unbefriedigende Form ist die Shortwette mit einem Optionsschein, das Problem ist die Laufzeit und das Timing. Habe das gerade bei Tesla versucht und es fast geklappt, ich werds nochmal versuchen aber wie gesagt mit dem Timing ist das so eine Sache das klappt ja meist nicht an der Börse.

Gegen einen Haufen Jünger die Aktien kaufen, egal wie abgrundtief schlecht die Fundamentaldaten sind, kann man kaum angehen.

Es gibt Artikel in der amerikanischen Presse die behaupten Tesla sei ohne weitere Kapitalmaßnahmen inert 3 Monaten pleite. Die Argumente sind zahlreich angefangen vom Junkstatus der Bonds, den dieses und nächstes Jahr fällig werdenden Schulden, den Produktionsproblemen beim Model 3 etc. pp.

Ein wie ich finde sehr apartes Argument hat ein amerikanischer Analyst gebracht, Tesla hat mit den Oberklassemodellen bisher nur Verluste eingefahren trotz satter Margen, und versetzt jetzt Mitarbeiter aus dieser Produktion in den Produktionsbereich für das Model 3 um mehr von einem Auto mit noch schlechteren Margen zu bauen.

Hinzu kommt Tesla war bisher ohne Konkurrenz, dieses Jahr kommen Jaguar und Audi in der Oberklasse mit eigenen E-Modelle raus und nächstes Jahr folgen die anderen großen Hersteller.

Man wird sehen wohin das führt und ob die Jünger auch am Tag der nächsten Quartalszahlen dem 1. Mai noch so stumm vor Glück sind. Bei den Quartalszahlen ist der Gestaltungsspielraum von Musk deutlich geringer.

Übrigens Musk wollte ja ursprünglich einmal 500.000 Autos pro Jahr bauen, selbst wenn er dieses Jahr durch ein Wunder die Zahl von 5000 pro Woche erreicht sind das bei 52 Wochen knapp 250.000 Autos pro Jahr und damit hat er sein ursprüngliches Ziel deutlich verfehlt.

Tesla wird jetzt schon so bewertet als wäre die goldenen Versprechungen längst Fakten.

Für Otto Normalanleger ist ein Teslashort aus den o.g. Gründen eher finanzieller Selbstmord, eine kleine sportliche Wette hingegen mit einer verschmerzbaren Summe, warum nicht.

Von den “FAANG” – Werten haben bis auf Amazon und Netflix alle anderen die 200-Tage-Linie bereits zum Teil deutlich unterschritten:

https://www.boerse.de/aktien/Facebook-Aktie/US30303M1027

https://www.boerse.de/aktien/Amazon-Aktie/US0231351067

https://www.boerse.de/aktien/Apple-Aktie/US0378331005

https://www.boerse.de/aktien/Netflix-Aktie/US64110L1061

https://www.boerse.de/aktien/Alphabet-A-Aktie/US02079K3059

Ebenso das auch zum Tech-Sektor zu rechnende Unternehmen Tesla:

https://www.boerse.de/aktien/Tesla-Motors-Aktie/US88160R1014

Jedoch noch nicht der große Nasdaq 100 – Index:

https://www.boerse.de/indizes/Nasdaq-100/US6311011026

Die 200-Tage-Linien-Strategie ist hier gut erläutert:

http://aktien-mit-strategie.de/200-tage-linien-strategie/

Insofern ist man aktuell bei einem Teil dieser Überflieger-Unternehmen bereits desinvestiert, dem zukünftig wahrscheinlich noch weitere folgen werden.

Die Wirksamkeit dieser Strategie in Form von Verlustvermeidung läßt sich für die Vergangenheit einfach feststellen.

Ferner wird zukünftig irgendwann erneut ein Einstiegssignal erfolgen: demnächst, falls sich die Hausse weiter fortsetzt oder viel später, wenn die aktuelle Entwicklung in eine Baisse mündet.

Ein weiterer Indikator zur Unterstützung der Trendsignale sind Richtung und Steigerungsrate der amerikanischen Wertpapierkredite (Nyse Margin Debt):

https://www.advisorperspectives.com/dshort/updates/2018/04/02/margin-debt-and-the-market

http://www.finra.org/investors/margin-statistics

Regelmäßige, wenigstens monatliche Kontrolle!

Ich bin ja seit längerem geneigt, Short Positionen auf FANG Aktien sowie andere NASDAQ Titel (e.g. Tesla) einzugehen. Allerdings muss man ja mit weiteren Hilfspaketen (QE) seitens der US Regierung rechnen, sobald es ordentlich runtergeht. Und damit sind eventuelle Shorts riskant. Wie sehen Sie das?

Hier das big picture von Martin Wolf: https://m.soundcloud.com/ft-analysis/martin-wolf-the-wests-global-order-unravels

LG Michael Stöcker

„We’ve hit a cyclical peak“

Und das wohl auch bei den Zinsen: https://bankunderground.co.uk/2018/04/04/bitesize-uk-real-interest-rates-over-the-past-three-centuries/

LG Michael Stöcker