Update zu Gold

Immer wieder habe ich mich (strategisch) positiv zu Gold geäußert. So hier:

→ Warum Gold ins Portfolio gehört

Nun kann man mir vorhalten, dass gerade in diesem Jahr die Entwicklung des Goldpreises gegen das Metall spricht. Haben wir nicht Krisen überall und das Gold sollte steigen? Doch es fällt? Und zwar wie!

Das hat interessanterweise besonders viel mit der Krise in den Schwellenländern zu tun bzw. hat eine gemeinsame Ursache. Der steigende US-Dollar führt zu Stress in den Schwellenländern und die steigenden US-Zinsen schlagen sich entsprechend negativ nieder, eben auch im Kurs von Gold. Es kann auch gut sein, dass die Schwellenländer Gold verkaufen – so habe ich das Gerücht aus der Türkei gehört –, um sich Liquidität zu beschaffen. Die FT dazu in zwei Kommentaren:

- “(…) we should be focusing on the strength of the dollar, rather than on events in Turkey, comes from gold. Demand for gold may ultimately lie in the eye of the perceiver, but the gold price is a great gauge of perceptions of risk, and of fears that paper currencies may suffer debasement. It remains an important link in the financial system.” – bto: weshalb es eigentlich komisch ist, dass er fällt.

- “And somehow the gold price has tumbled 12 per cent, when measured in dollars, since its recent peak 12 months ago, following a trajectory that looks remarkably like that of an emerging market currency in that time. It has given up all its gains since the election of Donald Trump in November 2016. As we are in a ‚risk-off‘ environment, when investors try to limit their risks, gold might normally be expected to be exactly the kind of place where they would seek shelter.” – bto: Das würde ich auch sagen, wir tun es nur scheinbar nicht!

- “(…) demand for gold tends to come from emerging markets, whether from individuals for jewellery or from central banks for their reserves, and so this is a sign that investors in emerging markets now feel it necessary to buy dollars rather than gold. And in part, gold tends to function as an indicator of alarm about the Federal Reserve. If investors think that the central bank will be too easy and allow inflation to take off they will buy gold. At present, the perceived risk is that the Fed will be too hawkish (and thus strengthen the dollar).” – bto: also Liquiditätsengpässe in den Schwellenländern und keine Inflationsängste?

- Derweil nimmt die Spekulation gegen Gold zu: “Traders have increased their bets against gold, with speculative positions in futures on the precious metal the most bearish in 17 years, according to government data released on Friday.” – bto: Es wird so stark wie schon lange nicht gegen Gold spekuliert, nachdem: “The price of a troy ounce of gold has fallen another 3.3 per cent this month to a one-and-a-half year low of $1,182.90, extending this year’s tumble to more than 9 per cent.” Also geht es weiter runter? Denke ich nicht.

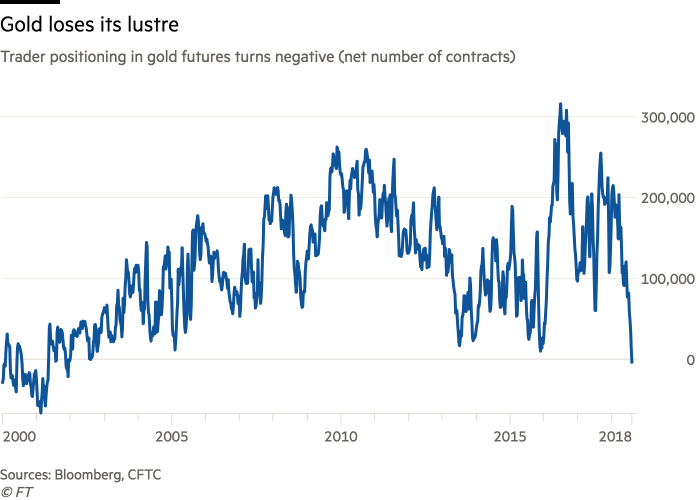

- “The net positioning of ‚non-commercial‘ players in the gold futures market — a CFTC classification that includes hedge funds, asset managers and trading groups — has fallen into negative territory for the first time since the end of 2001.” – bto: 2001 begann der Anstieg von Gold vom Tiefpunkt der Entwicklung seit den 1980er-Jahren bei 271 US-Dollar/Unze. Stehen wir also erneut vor einer derartigen Entwicklung?

Quelle: FT

- “‚When you see this extreme positioning on the short side it leads to a bottom in gold (…) It’s a great sign that a gold bottom is very near‘, said Mr Boockvar, a longstanding bull on gold.” – bto: Das könnte stimmen!

Das sieht auch PIMCO so:

“Gold is a real asset that not only serves as a store of value but also a medium of exchange, and that tends to outperform in risk-off episodes. As such, one would expect gold to outperform during the recent period of rising inflation expectations along with rising recession risk. Yet counterintuitively it has been underperforming relative to its historical average.” – bto: Gold ist also billig!

PIMCO weiter: “We believe this is because in the near term, gold’s properties as a metal and as a currency are causing it to drop amid trade tensions and the stronger U.S. dollar, dominating its properties as a long-term store of value. This leads, in our view, to an opportunity to add a risk-off hedge to portfolios at an attractive valuation.” – bto: eine Sicht, die ich teile.

→ zerohedge.com: “Traders increase bets that gold has further to fall”, 17. August 2018

Wir hatten vor einiger Zeit hier doch auch die short-Positionen von Bridgewater auf europäische Aktien und long-Position auf Gold in der Diskussion. Ist bekannt, wie das ausgegangen ist? Die short-Positionen auf deutsche Aktien wurden wohl schon relativ schnell glatt gestellt.

In einem Interview hat Dalio bekräftigt, an den long-Positionen zu Gold festhalten zu wollen (obwohl es natürlich sein kann, daß er öffentlich so eine Aussage trifft und dann gegenteilig handelt).

Wenn ein großer Teil der short-Positionen auf Gold seit Januar dieses Jahres eingegangen wurde, müßten diese dann nicht bald glatt gestellt werden?

Hier noch ein interessanter Artikel zum Sentiment: https://www.goldseiten.de/artikel/387113–Die-Tuecken-der-Sentimentanalyse-am-Goldmarkt.html

Der dort abgebildete Charts zeigt, dass die Spekulanten am Gold-Futuresmarkt der COMEX zwischen 1996 und 2001 durchgehend short waren. Das ist aktuell (noch) nicht der Fall. Es ist auch nicht gesagt, dass es im aktuellen Zyklus dazu kommen muss. Das heißt aber nicht, dass es nicht dazu kommen könnte.

Ich verstehe die ganze Überraschung bzgl. des Goldpreis-Rückgangs ehrlich gesagt nicht. Gold ist primär einen Versicherung gegen einen fallenden Dollar. Dieser ist aber extrem stark aktuell und wird es vermutlich noch einen ganze Weile bleiben (kriselndes Südeuropa, steigende Zinsen in USA im Gegensatz zu Europa). Wer Gold als Versicherung sieht lebt entspannter, einfach eine fixe Quote ins Depot am besten physisch und bei unterschreiten der Quote nachkaufen ;-)

Edelmetalle sind eine essentielle Lebensversicherung für das Vermögen – vor allem

gegen Krisen und das Notenbankexperiment der EZB. Es ist durch die Natur limitiert, bewährt und schützt vor Inflation.

Gold ist kein Spekulationsobjekt, Gold ist eine Versicherung.

Beispiel: Stellen Sie sich aktuell einen Bewohner der Türkei vor, der zum Jahresanfang seinen Vorrat an türkischen Lira in Gold getauscht hat. Alternativ jemand, der sein Gold in gleicher Menge gemäß dem Wunsch des türkischen Präsidenten zeitgleich in Lira getauscht hat.

Ich denke, das Ergebnis ist klar: Entscheidend ist die Entwicklung des Goldpreises in der eigenen Landeswährung. Und damit kommen wir zu uns. Entscheidend für Einwohner im Euroraum ist der Goldpreis in Euro. Und hier besteht durchaus noch Luft nach oben…

Die türkische Lira nur in US-Dollar zu tauschen und jene in US-Treasuries oder ggf. ETF´s anzulegen wäre die bessere Lösung gewesen, da Gold seit Jahresanfang in US-Dollar ca. 5% verloren hat:

https://www.boerse.de/historische-kurse/Gold-Euro/XC0009655157

>Gold ist kein Spekulationsobjekt, Gold ist eine Versicherung.

Ich sehe das bzgl. physischem Gold und Silber auch so. Eine ältere Bekannte hatte vor ein paar Jahren ein paar Münzen, die noch vom Opa waren, geerbt. Die “Mark des neuen Deutschen Kaiserreichs” waren nicht in seinem Säckle gewesen. Das gibt Perspektive, was es mit Edelmetallen wirklich auf sich hat: Geld / Währungsersatz für den Notfall und generationsübergreifend.

Allerdings wird ja mit dem Papiergold-Preis ganz ordentlich spekuliert. Ist irgendwie schon kurios, dass dieser den Preis bestimmt und nicht das physische Angebot der Minen.

@Thomas M.: in guten Zeiten ist das mit dem Papiergold sicher so. Interessant wird es, wenn die Panik um sich greift und einer der Kontrahenten physische Auslieferung verlangt. Papiergold ist Schönwettergold, solange der Dollar halbwegs wertstabil ist. Wenn er das nicht mehr ist, wird es interessant. Siehe Türkische LIra.

@Hr. Selig: Bei den Papiergold-Zertifikaten ist auch das Kleingedruckte lesenswert: “Redemptions can be suspended if trading on the NYSE or COMEX is suspended or restricted, or one or both exchanges are closed for any reason; or if an emergency dictates that “delivery, disposal, or evaluation of gold is not reasonably practicable.”” Über den letzten Satz kann man sich dann beliebig lange streiten…

Wie Sie schon sagen: Papiergold ist Schönwettergold. Zum Traden gut und bequem, als Versicherung unbrauchbar.

@SB Guter Link… Die Kurse der Goldminen (bzw. GDX-ETF) lagen tatsächlich fast leerbuchmäßig in einem “bearishen” Dreieck inkl. sinkender Umsätze. Goldminen sind halt eine Achterbahn… so schwungvoll wie’s runter geht, geht’s aber auch gerne wieder rauf. Nichts für Leute, die jeden Tag ins Depot gucken…

@ Thomas M.

Goldminen- und Rohstoffaktien sind nur etwas für Leute, die jeden Tag oder zumindest regelmäßig ins Depot gucken, vgl. innerhalb einer längeren Zeitdauer die jeweils kurzen Zeiträume, in der eine Investition durch die 200-Tage-Linie angezeigt war:

https://www.boerse.de/historische-kurse/Barrick-Gold-Aktie/CA0679011084

https://www.boerse.de/historische-kurse/Anglogold-Ashanti-Aktie/US0351282068

https://www.boerse.de/aktien/Freeport-McMoran-Copper-Aktie/US35671D8570

https://www.boerse.de/historische-kurse/Rio-Tinto-plc-Aktie/GB0007188757

https://www.boerse.de/historische-kurse/CVRD-Aktie/BRVALEACNOR0

lehrbuchmäßig meinte ich natürlich :) Das die zwei Wörter so ähnlich geschrieben werden… man fragt sich, woher das kommt.

The net positioning of ‚non-commercial‘ players in the gold futures market — a CFTC classification that includes hedge funds, asset managers and trading groups — has fallen into negative territory for the first time since the end of 2001.“ – bto: 2001 begann der Anstieg von Gold vom Tiefpunkt der Entwicklung seit den 1980er-Jahren bei 271 US-Dollar/Unze. Stehen wir also erneut vor einer derartigen Entwicklung?

Passend zur Beantwortung dieser Frage dieser Artikel: https://www.goldseiten.de/artikel/387082–Die-Goldaktien-brechen-zusammen-Was-nun.html