Der Zusammenbruch der SVB einfach erklärt

Es wurde und wird viel geschrieben über den Zusammenbruch der SVB. Die BlackSummit Financial Group hat es in einer Mail gut zusammengefasst:

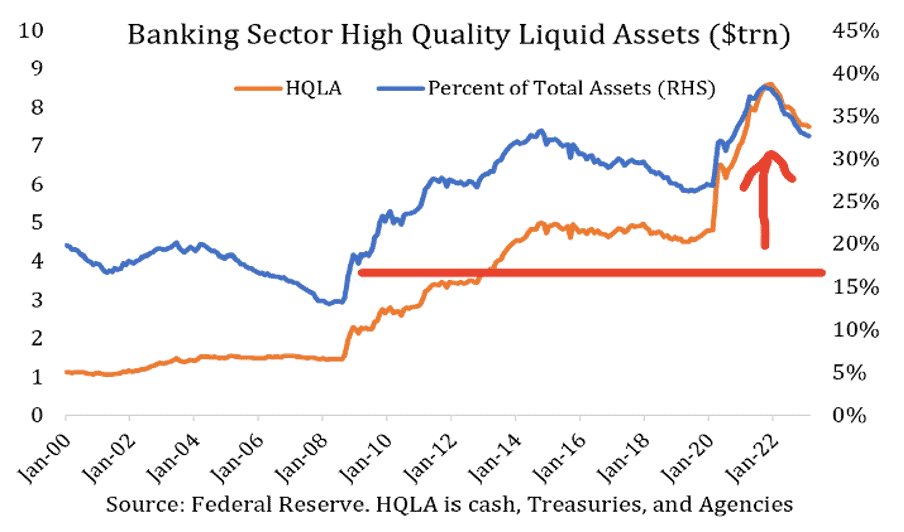

- The Quality of the Assets Was Not the Issue

- „This wasn’t a story of questionable loans or securities that didn’t hold their weight. The bank parked the majority (over 95% per its Balance Sheet as of Dec 31, 2022) of its deposits into US Treasuries and Agency bonds that are backed by the federal government. While every investment has some form of risk, credit risk wasn’t the concern here. The banking sector in large isn’t anywhere close to the kind of position it was in 15 years ago. High-quality assets, namely Treasuries and government-backed agency securities are a much greater mix of balance sheets now compared to then.“ – bto: Es ist eben ein anderes Risiko und zwar jenes, dass die Marktwerte der Assets angesichts steigender Zinsen nicht stimmen.

Asset Quality Is Much Better Than Pre-GFC, Source: Joseph Wang

Quelle: BlackSummit

2. So What Was the Issue?

- „Silicon Valley has positioned itself as the preeminent financial institution serving venture capitalists, nascent tech companies, and high-net-worth individuals. It developed a specialty around an industry that 40 years ago when SIVB was founded, was not something a lot of bankers wanted to touch because of unfamiliarity, unique attributes, newness, and other traits. But the competency and relationships SIVB built served them well. The stock compounded over 18%, in line with the Nasdaq, from the Financial Crisis to two Fridays ago, which includes the stock getting cut in half before the events of last week.“ – bto: Das ist natürlich eine beeindruckende Performance. Das Team war also nicht so schlecht, mit Ausnahme eines erheblichen Managementfehlers, der sich als tödlich erwies.

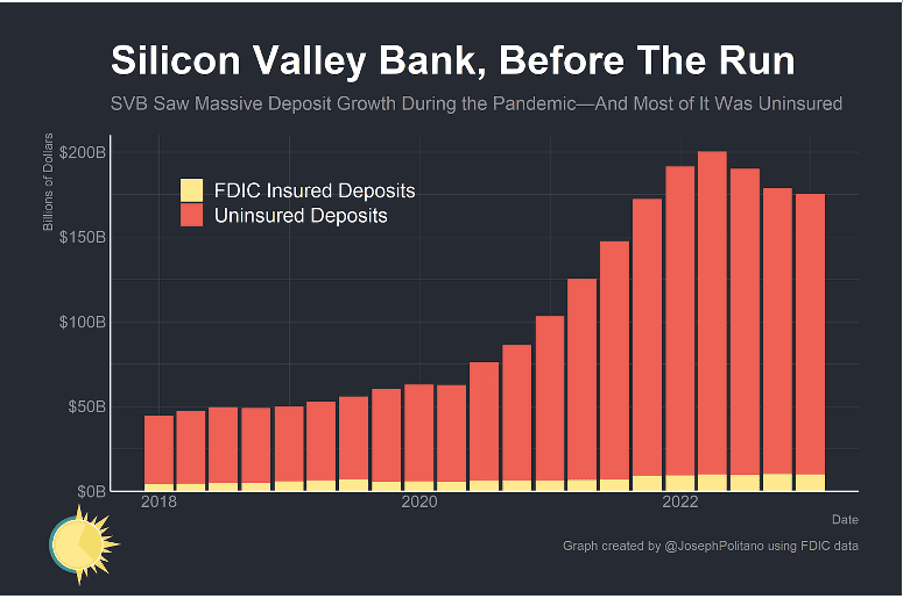

- „That is even more so the case in the boom sparked by the Covid recovery. Everything tech-oriented and tech-adjacent saw booming valuations, easy funding rounds, and business plans approved regardless of how cash burning or flimsy the economic case was. (…) The cash poured into venture and tech companies who deposited it at SIVB; since 2019 deposits at the bank tripled while across the industry they only rose 37% during the same period.“ – bto: Die Bank war also der Parkplatz für die eingesammelten Milliarden. Sie vergaß aber, dass die Milliarden auch wieder abfließen, weil ihre Kunden – die Start-ups – das Geld zur Finanzierung ihres Aufbaus verbrauchten.

Deposits Have Tripled at SIVB Since 2019, Source: Joseph Politano

Quelle: BlackSummit

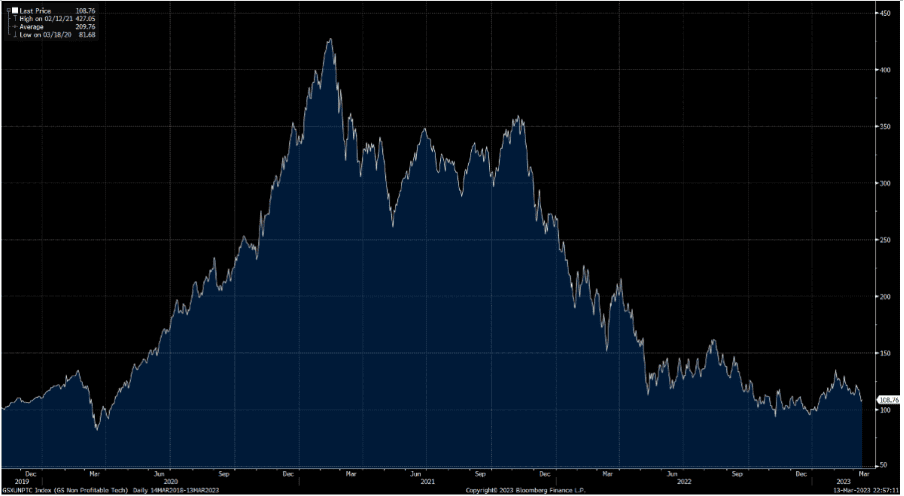

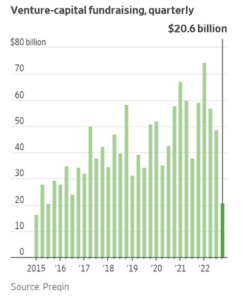

- „But after the Covid boom came the Covid bust where the biggest losers have unquestionably been the most speculative and economically dubious companies. Goldman’s Unprofitable Tech Index tells the story well (Figure 3). It’s no surprise then that VC fundraising across the market fell off a cliff (Figure 4).“ – bto: Das heißt: Es kam kein frisches Geld hinzu, während das vorhandene Geld abgerufen wurde.

The Unprofitable Tech Burst, Source: Goldman Sachs

Quelle: BlackSummit

VC Funding Last Q Was Lowest in Almost a Decade, Source: WSJ

Quelle: BlackSummit

- „A slowdown in VC fundraising meant fresh deposits weren’t coming in to replenish SIVB. And cash burn remained extremely elevated. Per an investor presentation from management last week cash burn from SIVB’s clients was still twice as high as pre-2021 levels and VC funding was due to fall an additional 15-20% from last quarter (i.e. from already depressed levels).“

Companies Continued to Burn Cash While New Funds Weren’t Coming in Fast Enough, Source: SIVB

Quelle: BlackSummit

- „SIVB management determined the imbalance between inflows and outflows of funds required some sort of action. The bank announced that it would sell $21B of securities off its books (marked as Available for Sale (AFS) on its Balance Sheet) but would do so at a loss of $1.8B. All of the bonds it had purchased with the surge of deposits had fallen in market value due to rising rates all across the bond market; a sale of common and preferred shares would occur as well in order to shore up its capital position following the loss.“ – bto: Im Prinzip ist das wie ein Margin Call. Man muss Assets verkaufen, um die Auszahlung zu leisten. Kann man die nur mit Verlust verkaufen, wird es ein Problem.

- „(…) emotions took over, with VCs recommending their companies to withdraw cash because ‚there was no downside to removing their money from the bank.‘ The next day $42B was taken out of SIVB as fear spread from one firm and one VC to the next, without ever giving a second thought to the self-fulfilling stampede they were causing. Hysteria took over. Everyone went for the door at the same time and by mid-day Friday, the FDIC had closed the bank and put it in receivership.“ – bto: Und die so smarten Investoren in Start-ups sowie die Gründer waren zunächst so dumm, hohe Beträge an die Bank zu geben und dann einen Bank-Run auszulösen, das muss man auch dazu sagen. Darunter – so die Gerüchte – so illustre und bekannte Namen wie Peter Thiel.

- What Could Have Been Done?

- „First, and perhaps most importantly, there’s been a surprising and disappointing amount of discourse stating that where SIVB erred was in borrowing short and lending long. This, we would point out, is the very definition of a bank; it is the nature of the business model. To point to this as an issue is to point a finger at all banks. Further, not a single bank is set up or could be set up to survive a full-fledged spontaneous bank run. Human emotion and psychology cannot be hedged away.“ – bto: Dennoch haben Banken extra Risikomanagement-Tools, um genau das zu verhindern.

- „(…) the further anyone digs into SIVB over the last couple of years, the more apparent that the distinguishing characteristics of the bank were ones of mismanagement, particularly with regard to risk. Banking 101 is about matching up assets and liabilities so that your duration exposure on either side of the balance sheet is not imbalanced from the other. But with VC funding being the dominant vertical served, SIVB had to know the deposits sitting in its accounts weren’t destined to be long-term liabilities. Yet most of its assets were put in longer-duration Treasuries and MBS. While these instruments bore little credit risk as discussed above, they did possess substantial duration risk if rates rose. Some duration is ok, but too much could be a death sentence with a deposit base that is expected to be withdrawn so that venture companies can cover things like payroll and operating expenses. Further, virtually none of the portfolio was hedged from interest rate risk…” – bto: Eine große Zinswette, die schiefgegangen ist.

- „A counterpoint to the hedging argument is that by entering into an IR swap, SIVB would essentially be foregoing any return. To that I would say if the goal is to make money on the direction of bond prices they should be a hedge fund; some level of hedging to line up with the deposit base would be prudent.“ – bto: Natürlich!

- „Further, inflation has been the biggest macroeconomic story of the past year or so and anyone with a Bloomberg terminal could have told you the direction monetary policy was headed with the way inflation data was coming in. And yet, the bank continued to increase its duration quarter after quarter.“ – bto: Sie haben also gegen die Fed gewettet…

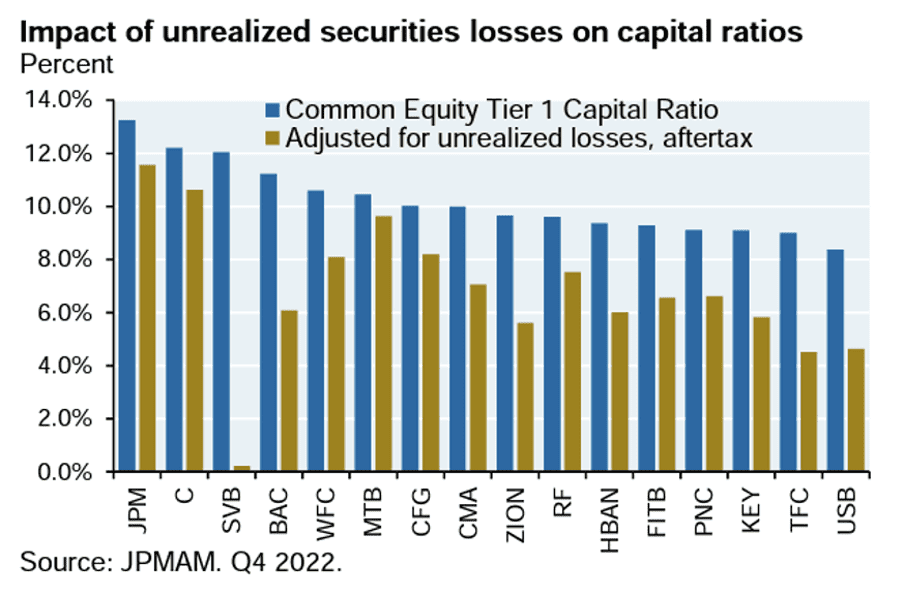

- „Other banks saw this risk and made cautious and calculated decisions to watch their duration exposure. Instead of reaching for yield by moving further out in time or buying riskier debt, M&T Bank made the astute observation that if they were wrong, an equity raise would squash any extra yield picked up. Instead of reaching for yield, they parked more funds at the Fed. M&T’s wisdom is clearly evident in Figure 7 and in stark contrast to SIVB. While Figure 7 clearly shows there would be a notable impact on the capital position of the banking sector if unrealized losses were considered, SIVB clearly stands out unique in the management of its portfolio.“ – bto: … wobei man von Management wohl nicht sprechen kann…

One of These Is Not Like the Other, Source: JP Morgan

Quelle: BlackSummit

4. Did it Need a Bailout?

- „(…) depositors have been made whole at SIVB (as well as at Signature Bank of NY which went into receivership on Sunday) while equity and debt holders have been wiped out. A new credit facility by the Fed was created, and backstopped by the Treasury, to extend credit to regional banks against collateral at full par value. The actions constitute a bailout but not exactly in the same terms as what we saw in 2008. There is no federal ownership of a bank. There is no TARP. Taxpayer funds aren’t being used to support stocks. But it still represents public authorities influencing events to prevent the full pain induced by the private sector. It’s clear based on press reports that the FDIC, Fed, and Treasury all preferred a buyer to step up and purchase the bank while guaranteeing all deposits, but that option didn’t materialize in time.“ – bto: Einfach deshalb, weil die Risiken zu groß sind bezüglich der Zinswette.

- „Did it have to happen this way? (…) there was zero chance all uninsured deposits would have been lost. In fact, there are plenty of credible and plausible scenarios by which 80% more of uninsured deposits would have fully paid out. Maybe not all at once, but enough capital would have been available Monday morning so that business could resume for all stakeholders.“ – bto: … weil die Qualität der Assets stimmte.

- „Presumably, this was done to prevent a wave of bank runs from ensuing first thing Monday morning across the country. How likely that threat was can’t be known but the hysterics by many over the weekend certainly weren’t helping to calm the situation down. For whatever it’s worth, several major regional bank CEOs said they were not seeing unusual withdrawal activity on Monday. Whether that would have happened without these actions is a counterfactual no one can prove.“ – bto: Es wäre nicht begründet gewesen. Aber vielleicht wäre es begründet, die Start-ups und ihre Kapitalgeber neu zu beleuchten und zu bewerten?

Das meinte ein anderer Kommentator im englischen Telegraph:

- „Yet the debacle has also shone a particularly harsh light on the arrogance and hubris of a technology sector where valuations have been pushed to ridiculous levels by cheap and seemingly limitless money. That era should have come to an abrupt end the moment the Federal Reserve started raising interest rates. Like the cartoon character Wile E. Coyote, it nevertheless kept on motoring, seemingly oblivious to the fact that tighter money would knock a giant hole in valuations.” – bto: Das ist ein zweifellos richtiger Punkt.

- “If interest rates go up, asset values by definition go down to reflect the higher yield environment. A day of reckoning awaits for many of the candyfloss companies, and their venture capital backers, that rode the cheap money wave. They are about to get their comeuppance.“ – bto: Und das hat natürlich breitere Auswirkungen.

- “But what SVB has done is demonstrate just how vulnerable a world awash with debt is to any tightening in interest rates. It seems as if central banks have got themselves into a position where they cannot properly address inflationary pressures without destabilising the entire system. It’s always the same old story. When the tide goes out, you get to see who’s been swimming naked, and it’s rarely a pretty sight.” – bto: Deshalb werden die Notenbanken nicht hart genug gegen Inflation vorgehen.

Diese verlorene Welt auf der Erde erhält ein den erlösenden Gnadenakt, um ohne die Fähigkeiten zur Selbstreinigung zu verwesen.

https://youtu.be/HIttdb9uaYU

ab Minute sechs –

Bazon Brook warnt vor dem Kulturalismus in der Kunst und Wissenschaft.

Ein knapp zweistündiger Vortrag ohne Hilfmittel – Medien – Ablenkungen von der schieren Wirkungskraft des Seins im Hier und Jetzt (Del Amitri “Mother Nature’s Writing” im vielleicht wunderschönsten Roxy Club-youtu.be/sdxGQ0xfeog)

Ein weiterer toller Artikel von Mark Dittli (The Market) mit treffender Überschrift:

Credit Suisse hat Zeit erhalten – mehr nicht

https://themarket.ch/meinung/credit-suisse-hat-zeit-erhalten-mehr-nicht-ld.8618

Nebenbei:

In Zukunft werden wohl noch sehr viele solche Überschriften zu lesen sein…einfach mit anderen Firmennamen … :-) :-)

..vielleicht steht bald die Deutsche Bank in der Überschrift..??

https://cdn.prod.www.manager-magazin.de/images/0aab37dc-0001-0004-0000-000001307455_w616_r1.37987012987013_fpx65.89_fpy54.88.jpg

Der Chart ist aus einem Artikel von 2018 ….aber spielt ja keine Rolle, den der Kurs ist seit 2018 ja praktisch “eingefroren” und unverändert…. und Gestern bei 9.48… :-)

@ weico

Die Deutsche Bank wird ja vorbildlich saniert und entsprechend umgebaut. Sie erwirtschaftet Gewinn. Bei einer jetzigen Dividendenrendite von ca. 2,11 % und einer Dividende von zuletzt 0,20 Cent je Aktie ist dies ein klares Langzeitinvestment.

Bei 1 EUR Dividende je Aktie hätte man 10 % Dividendenrendite, bei 2 EUR je Aktie 20% Dividendenrendite.

Nur die Zukunft zählt. Diese könnte gut werden.

@Gnomae

“Die Deutsche Bank wird ja vorbildlich saniert und entsprechend umgebaut. Sie erwirtschaftet Gewinn. Bei einer jetzigen Dividendenrendite von ca. 2,11 % und einer Dividende von zuletzt 0,20 Cent je Aktie ist dies ein klares Langzeitinvestment.”

Ob CS oder Deutsche Bank…die werden schon seit Jahren “umgebaut” und “erfolgreich” saniert.

Aus den vergangenen Dividendenzahlungen etwas für die Langzeit herauszulesen, halte ich als …gelinde gesagt…nicht sehr klug.

“Diese könnte gut werden”

Klar…wie bei Allem und…mit Betonung auf KÖNNTE..! :-)

Nebenbei:

Die Dividendenrendite war ja bisher auch bei der CS nicht so schlecht…auf dem Weg nach UNTEN.

Die Deutsche Bank hatte da z.B. mehr “Aussetzer” mit den Dividendenzahlungen…auf dem Weg nach UNTEN.

https://www.finanzen.ch/dividende/credit_suisse

Eine schöne Seite um Aktien zu Vergleichen ist …deraktionaer:

Mal 2 grosse Bank-Werte aus Europa mit 2 aus USA :

https://www.deraktionaer.de/aktien/peergroup/creditsuisse-ch0012138530.html?peergroup=DE0005140008&peergroup=US0605051046&peergroup=US46625H1005

@Gnomae

“Die Deutsche Bank wird ja vorbildlich saniert und entsprechend umgebaut. Sie erwirtschaftet Gewinn. Bei einer jetzigen Dividendenrendite von ca. 2,11 % und einer Dividende von zuletzt 0,20 Cent je Aktie ist dies ein klares Langzeitinvestment.”

Nein. Solange ich nicht nachvollziehen kann, wie viele Anlagen mit Wertverust immer noch zu völlig überhöhten Buchwerten in den Büchern der Deutschen Bank stehen, ist die Aktie gar kein Investment.

Oder soll ich etwa auf die Ehrlichkeit ausgerechnet von Bankmanagern vertrauen?

Was hier wieder alles diskutiert wird – bis hin zur Schuldfrage.

Wo ist das Problem?

Es gibt KEINES außer einer vorübergehenden Nervosität.

LIQUIDITÄT ist jedenfalls HINREICHEND da.

FRC betreffend, die nach der SVB dran ist, hier:

https://finance.yahoo.com/news/biggest-banks-to-infuse-first-republic-with-30-billion-to-stabilize-troubled-lender-192748893.html

Daraus:

>The biggest U.S. banks are banding together to rescue beleaguered San Francisco lender First Republic (FRC) with $30 billion of uninsured deposits, an unusual joint effort to stabilize a rival and restore calm following a volatile week.

The actions of America’s largest banks reflect their confidence in the country’s banking system,” the banks said in a joint release. “Together, we are deploying our financial strength and liquidity into the larger system, where it is needed the most.”

Federal Reserve Chair Jerome Powell, Treasury Secretary Janet Yellen and two other regulators said in a joint statement that “this show of support by a group of large banks is most welcome, and demonstrates the resilience of the banking system.”>

Credit Suisse betreffend:

Die SNB hat mal eben über Nacht 50 Milliarden Franken rausgereicht und schon ist wieder Ruhe im Karton.

Die Aktienmärkte quittieren das mit Kursaufschlägen.

Bis zum nächsten Mal …

Mag ja alles richtig sein. Der Moral Hazard bleibt trotzdem. Vor allem, wenn es dabei bleibt, dass die ungesicherten Einlagen von Milliardären/Millionären ihnen erstattet werden. Und das hat nichts mit Neid zu tun.

@Beobachter

Der deutsche Rentner legt sich wieder schlafen – mal sehen, wann er das nächste Mal geweckt wird. ;)

Kennen Sie eigentlich schon Yves Smith von Nakedcapitalism? Eine Leseempfehlung, besonders, wenn Ihnen die Wortmeldungen hier tendentiell zu regierungs- und bänkerfreundlich sind:

https://www.nakedcapitalism.com/2023/03/svb-and-the-only-choice-we-have.html

Märkte funktionieren immer,

egal wie schwer und lange die Manipulation der Geldschöpfer andauert.

Mit der Zeit gewinnt das Pack mehr Fallhöhe und verliert Sanierungsdemographie,

weil die Transferverpflichtungen wachsen.

Wetten, dass dem Geldsystem vor Ende der großen Transformation die Luft ausgeht,

egal wieviel Liquidität man zwangsrekrutiert.

Ökonomie ist eben nicht bullshit Artisten in tech Klitschen zu pampern,

bis die Lebenshaltung unerschwinglich ist, meanwhile in California https://youtu.be/RaBtmA3rp3Y

@foxxly

Sobald die Allgemeinheit haftet, für den Blödsinn Weniger ist´s Sozialismus,

besonders wenn Gewinne privatisiert wurden.

Ich sehe schon: Die nächste Flüchtlingswelle kommt aus? … aus California dreaming.

Wir haben noch Platz. Das Boot ist noch lange nicht voll. Wir retten jetzt auch California dreaming …

Man glaubt es kaum, was man in diesem Video sieht. Armut und Erbärmlichkeit.

USA – Kalifornien. Ein reiches, zumindest wohlhabendes Land. Oft besungen.

Die Mamas und Papas haben diesem Land eine Hymne gewidmet, es beseligt besungen; bereits 1966.

Ein unsterblicher Hit; eine Hommage, eine Huldigung an dieses sonnenverwöhnte Land.

https://www.youtube.com/watch?v=N-aK6JnyFmk (über 314 Mio. mal aufgerufen!)

Es hat sich für ewig in mein musikalisches Gedächtnis eingeprägt.

Was für ein häßlicher, kaum verstehbarer Kontrast ist dieses kurze Video zu den Verheißungen, Versprechungen dieses Liedes?

Live aus Buxtetown am Esteriver – 16.3. 2023 – 18:50 Uhr Ortszeit

Felix Haller – nicht erst seit 2013 alternativ

@Bagwahn

Keine ” primitive ” Gesellschaft / Ethie hat historisch je so depriviert, verwahrlost, verarmt , mit Drogen vollgepumpt und verelendet im Dreck leben müssen wie das Lumpenproletariat – heute in LA, morgen in deutschen shitholes. Medikamenten-Drogen-Flohmärkte sind in D. vorgeschlagen und werden der Renner. ( Opium war noch sauber gegen den synthetischen Crack-Dreck aus versifften Laboren) . Mit dem Vertrauen in Geldwert versinken auch menschliche Beziehungen in Hoffnungslosigkeit, Gender-Wahn , Pubertäts-Blocker und Kinder, die Messer-morden.

Künstlerinnen geben Vor-Einblicke in Hoffnungslosigkeit:

https://www.youtube.com/watch?v=Dll6VJ2C7wo

Wenn man das extrapoliert, wie will Amerika den Stellvertreterkrieg in der Ukraine gewinnen, oder erst recht gegen China?

(Trotz Elon Musks’s Space X, die innovativste Firma der Welt)

@Wer war schuld?

Risikoabteilung der Silicon Valley Bank und die Aufsicht bei der Federal Deposit Insurance Corporation (FDIC) & Federal Reserve Bank of San Francisco

– nicht die Zinserhoehungen der FED

– nicht die scheuen Kunden, die mal eben 42 Mrd$ abgezogen haben (Geld ist ein scheues Reh)

– nicht die VCs

– nicht die poehsen Spekulanten

Die SVB war schon im Herbst 2022 (tiefer) unter Wasser und alle hatten beschaemt weggeguckt oder hats der Filz unterm Deckel gehalten?!

Das ist natuerlich nicht von mir, sondern nachgeplappert von Karsten Jeske auf

https://earlyretirementnow.com/2023/03/16/march-2023-market-musings

und der hat Ahnung!

LG Joerg

@Joerg

“Wer war schuld?”

Nicht vergessen: Vor der großen Finanzkrise 2008/09 gab es im Bankwesen noch einen Buchhaltungsstandard namens “mark to market acounting”, dem zufolge sämtliche Positionen immer zum aktuellen Marktwert bewertet werden mussten.

Nach der Finanzkrise wurde dieses Prinzip im Frühjahr 2009 aufgeweicht – was übrigens verblüffenderweise ziemlich genau mit dem Tiefpunkt an den Börsen zusammenfiel: https://www.fasb.org/page/getarticle?uid=fasb_NEWSRELEASE04_09_09Body_0228221200

“Dank” dieser Regeländerung können wir überhaupt erst ein Problem mit Banken haben, die auf einem riesigen Berg von unrealisierten Verlusten in ihrem Anleihen-Portfolio sitzen ohne schon vor dem Verkauf der Anleihen neues Eigenkapital auftreiben zu müssen, wenn sie der Zwangsliquidierung entgehen wollen.

Vorläufiges Fazit:

Die Probleme sind wie immer spezieller und grundsätzlicher Art.

Spezielles Problem:

Moral Hasard im Bankensystem lebt weiter. Es hat sich nur von den systemrelevanten zu den mittleren Bilanzgrößen verlagert, wo weiter unbehelligt von regulatorischen Vorschriften das Risikomanagement vernachlässigt werden kann.

Grundsätzliches Problem:

Der Liquiditätsentzug mit dem das globale Finanzsystem unter Stress gesetzt wird, und die unausweichlichen Folgen, auf die u.a. Jeff Snider seit Monaten gebetsmühlenartig verweist: “The lessons of Bear Stearns are playing out right before our eyes”:

https://youtu.be/flW_GnODQ9M

“Das Team war also nicht so schlecht”

Zum Jahresende 2022 hatte die SVB Assets in Hoehe von rund $211Mrd. auf eine Eigenkapitaldecke von rund $16Mrd. gepackt; also ein Kartenhaus – wie die meisten anderen Banken auch. Wenn da was schiefgeht, bricht das Ganze sofort zusammen. Prof. Sinn hat Recht mit seiner Forderung nach wesentlich hoeheren EK-Anforderungen fuer die Banken.

Das Weisse Haus erhaelt zahlreiche Anrufe aus dem “Valley” mit der Forderung, auch die Einlagen ueber $250k zu schuetzen. Ich dachte immer, die sind dort alle so libertaer und lehnen Staatseingriffe ab.

@Rolf Peter:

“Das Weisse Haus erhaelt zahlreiche Anrufe aus dem “Valley” mit der Forderung, auch die Einlagen ueber $250k zu schuetzen. Ich dachte immer, die sind dort alle so libertaer und lehnen Staatseingriffe ab.”

Dazu N.N.Taleb auf Twitter am 11. 3. , 11h06

“They are all libertarians until they are hit by higher interest rates”.

Am besten gefällt mir immer noch Talebs statement gegenüber seinen ( vielen ) Feinden:

” Wenn meine Kritiker mich genauer kennen würden, würden sie mich noch mehr hassen”. ( Handbuch für den Umgang mit Unwissen, S. 112)

@Rolf Peter

“Ich dachte immer, die sind dort alle so libertaer und lehnen Staatseingriffe ab.”

Ach, nein, wie kommen Sie denn auf die Idee?

Wenn die Unternehmer und Investoren im Silicon Valley wirklich libertär wären, dann würden sie den amerikanischen Geheimdiensten nicht Zugang auf die Nutzerdaten ihrer Ausspäh-Opfer, pardon, ihrer Kunden gewähren, oder? Diese Illusion ist spätestens seit Edward Snowden in Rauch aufgegangen.

Die deutsche Aussenministerin könnte ihr überragendes internationales Standing in die Waagschale werfen und die SNB auffordern, die Credit Suisse vollständig zu übernehmen.

Das würde den Aktienkurs pushen, die Altaktionäre trösten und der Schweizer Exportwirtschaft helfen.

Durch die nachhaltig erhöhte Franken-Geldmenge würde die Schweizer Währung weniger Neid auf sich ziehen.

“Die Credit Suisse wäre nicht pleite, sie wäre nur in solideren Händen”, hören wir einen deutschen Wirtschaftsexperten rufen.

“Und sie könnte sich nun, befreit von den Marktkräften, endlich hundertprozentig auf die Klimaziele fokussieren.

Und als Nebeneffekt einen Teil der durch den notwendigen Deindustrialisierungsprozess freiwerdenden deutschen Arbeitnehmer übernehmen …”

>bto: die Bank war also de Parkplatz für die eingesammelten Milliarden. Sie vergaß aber, dass die Milliarden auch wieder abfließen, weil ihre Kunden, die Start-ups das Geld zur Finanzierung ihres Aufbaus verbrauchten.>

Genau das ist der Punkt:

Es waren EINGESAMMELTE, nicht VERDIENTE Milliarden.

Der Unterschied nicht nur Banken betreffend, sondern generell:

Eingesammeltes Geld kommt von (Zukunfts)-GLÄUBIGEN, verdientes von REALISTEN, die für ERFAHRBAREN Nutzen bezahlt haben.

Was wiederum heißt:

KREDITE erhalten in aller Regel nur solche Unternehmen, die hinreichende Erlöse für erfahrbaren Nutzen erzielen, d. h. mit GEWINNEN Eigenkapital aufgebaut haben und DAHER über eine BONITÄT verfügen.

Hans-Werner Sinn in einem Interview mit welt.de

https://www.welt.de/wirtschaft/plus244308505/Hans-Werner-Sinn-zur-SVB-Blasen-wurden-aufgebaut-Nun-haben-wir-den-Schlamassel.html

Daraus:

„Die zur Inflationsbekämpfung nötigen Zinserhöhungen haben die eigentlich soliden, aber niedrig verzinslichen Staatsanleihen der Silicon Valley Bank entwertet und Eigenkapital vernichtet.

Die Eigenkapitalanforderungen an die Banken sind viel zu gering, zumal das Eigenkapital großenteils selbst nur rechnerisch durch die Zinssenkungen der Vergangenheit entstanden ist, die zu einer künstlichen Aufblähung der Werte der Anlagen führten. Mit höheren Eigenkapitalpuffern oder dem Verbot, Dividenden qua Verschuldung aus bloßen Wertzuwächsen zu bezahlen, hätte die Pleite vermieden werden können.

Ich habe jahrelang davor gewarnt, dass die Notenbanken mit ihrer ultralockeren Geldpolitik Blasen aufbauen und den Rückwärtsgang blockieren. Jetzt haben wir den Schlamassel. Es lief alles vorhersehbar ab. Die Zinssenkungen hatten die Kapitalmärkte wegen der dadurch entstehenden Wertzuwächse glücklich gemacht. Die Rückkehr der Zinsen auf ein der Inflation angemessenes Niveau, die jetzt versucht wird, ruft weltweit im Bankensystem Probleme hervor und wird deswegen nicht stattfinden.“

Frage an H.-W. Sinn:

Was wären die KONSEQUENZEN einer NICHT so ultralockeren Geldpolitik der Notenbanken gewesen?

Wäre es weniger Kreditgewährung der Banken bzw. Kreditgewährung zu deutlich höheren Zinsen gewesen und hätte dies daher – Zinsen sind Kosten für Unternehmen – zu mehr UNTERNEHMENSPLEITEN (Zombies!) und ARBEITSLOSIGKEIT geführt?

Wenn so, wie hätten die westlichen Gesellschaften dies verkraftet?

Fazit:

>It seems as if central banks have got themselves into a position where they cannot properly address inflationary pressures without destabilising the entire system.>

Das sehe ich auch so – „properly“ ist hier der Schlüsselbergriff.

Deshalb werden sie auch bei einer anhaltenden Normalisierung der Energiepreise und des Abbaus der Lieferkettenprobleme das Inflationsziel von 2% NICHT erreichen.

Aber sie werden 2 bis 3% erreichen können, wenn es gut läuft und 3 bis 4% erreichen müssen, wenn es nicht so gut läuft, was ich angesichts des Demografieproblems und des sich dadurch weiter aufbauenden Potenzials für Lohnsteigerungen für wahrscheinlicher halte.

Gibt es auf dem Weg bis zu einer wie auch immer verstandenen Zielerreichung Probleme im Finanzsektor, werden die Notenbanken den Privatbanken „Kredite“ gewähren und/oder der Staat wird sie rekapitalisieren.

Die Notenbanken brauchen dafür keine Bonität und die Privatbanken auch nicht, denn zumindest die bedeutenderen müssen gerettet werden, um den Systemkollaps zu verhindern.

Immer daran denken:

Angesichts der Labilität der Verhältnisse sind wir FORWÄHREND im Modus den VERHINDERNS des Schlimmsten – eben des Systemkollapses.

Ich weiß nicht was Herr Sinn mit höheren Eigenkapitalanforderungen genau meint. M.E. dürften auch Staatsanleihen nur mit ihrem Kurswert und nicht mit dem Nominalwert als Eigenkapital anerkannt werden. Das werden die Staaten aber nicht beschließen, weil sonst niemand ihre Schrottanleihen kaufen würde.

@ Lothar

Sie wissen anscheinend nicht, was Schrott ist.

Die Anleihen der wichtigsten Staaten, d. h. derer mit hoher Wertschöpfung und nicht zu hoher Verschuldung zum BIP sind in aller Regel die SICHERSTEN Anleihen.

Das Problem:

Sie ändern ihren Zeitwert, wenn sich die Zinsen ändern.

@ Lothar

Wenn eine Bank risikogewichtete Aktiva besitzt, deren Anrechnung 0 % auf die Risikoposition beträgt, sagt dies nichts über das Zinsänderungsrisiko aus.

Wenn eine Anleihe mit 120 % in den Büchern steht, durch Zinssteigerung aber der Kurs auf 100%, verlangt die mark to market Bewertung einen Ansatz von 100%. Ergo ergibt sich auf die Position ein Kursverlust von 20% x Bestand der Anleihe, welcher gegen das haftende EK läuft und er senkt entsprechend die Solvabilitätskoeffizienten ab (weil die Eigenmittel ja um den Verlust verkürzt werden). Gemäß obiger Grafik waren die Eigenmittel der SVB ja fast bei 0 %.

Die Eigenkapitalanforderungen kann man natürlich durch die Risikogewichtung von Staatsanleihen steuern. Das ist aber nicht gewünscht, weil wir dann wahrscheinlich einen Großteil unserer europäischen Banken neu kapitalisieren müssten.

@Gnomae

“Das ist aber nicht gewünscht, weil wir dann wahrscheinlich einen Großteil unserer europäischen Banken neu kapitalisieren müssten.”

So ist es, der Kaiser ist nackt.

Es ist wieder soweit !

Der Frühling naht, und damit die Gewitter-Saison im Zeichen des Klimawandels.

Der Bundeslandwirtschaftsminister gibt deshalb,

in Abstimmung mit dem engeren Führungskreis von FFF,

proaktiv die nachhaltigen Gewitter-Regeln für die kommende Saison bekannt:

1. Eichen sollst Du weichen

2. Buchen sollst Du verfluchen

3. Tannen sollst Du verbannen

4. Eiben sollst Du vertreiben

5. Fichten sollst Du vernichten

“Noch immer sterben in Deutschlands Wäldern jedes Jahr Bürger*innen durch Missachtung dieser Leitplanken”, so der Gesundheitsminister in seinem aktuellen Podcast.

Die Bundes-Innenministerin weist darauf hin, dass mit der öffentlichen Delegitimierung dieser Richtlinien

durch rechtslastige Kreise zu rechnen ist und ermahnt alle aufrechten Demokrat*innen zu erhöhter Wachsamkeit.

@Väterchen Thiel

Wenn ( endlich) der Euro crasht gibt´s bestimmt EZB-vorgedruckte grüne Blüten:

” money for nothing & your chicks for free “( Dire straits )

Hauptsache: GRÜN!.

https://www.youtube.com/watch?v=b6LfIzX-zp0

@ Dr. Lucie Fischer

Hauptsache: GRÜN!

“And it’s gone” (Southpark)” [insb.0:26]

https://www.youtube.com/watch?v=-DT7bX-B1Mg

aaand it’s gone

@Gnomae

In der gleichen Southpark-Folge wird auch gezeigt, wie genau die “Rettungsstrategien” bei Finanzkrisen ausgewählt werden:

https://www.youtube.com/watch?v=wz-PtEJEaqY

Wär ja schön, wenn es tatsächlich so liefe, ohne dass korrupte Venture-Capital-Fatzken aus Kalifornien bei der Regierung anrufen und das bestellen, was ihnen persönlich finanziell am meisten nützt.

Auch auf die Gefahr hin, gleich wieder Haue zu bekommen: mal die letzten Folgen J. Snider hören. Der stellt u.a. die Frage, WARUM die Startups aktuelle MEHR Cash brauchen als lt. Erfahrungshorizont der SVB zu erwarten war. Letztlich war es diese (untererwartete) Cash-Nachfrage, die zum Kollaps führte.

Hypothese: die Wirtschaft läuft schlechter als mit den ganzen Zinserhöhungselegien der ZBs suggeriert wird, es kommt weniger Cash aus dem Wirtschaftskreislauf bei Startups/Investoren an usw. Fazit: Rezession ist schon da bzw. kommt bald.

Zudem fragt er, warum aktuell (global) eine massiv gestiegene Nachfrage nach Staatsanleihen zu beobachten ist, OBWOHL in den nächsten Tagen Zinserhöhungen der EZB/FED erwartet werden…

Es droht Ungemach.

Momentummäßig stottern die Aktienmärkte seit ein paar Monaten -> Flight to Safety?

Das Gute: Mit den aktuellen Zinsen für kurzlaufende US-Staatsanleihen kann man sich schon heute ein Super-Sparbuch basteln. Wenn die Zinsen steigen, wird’s zukünftig noch besser. Fühlt sich fast wie gute alte Knax-Zeit an – man muss nur Währungsschwankungen ausblenden ;)

@Thomas M.

Bei J Snider geht es eigentlich überhaupt nicht mehr um die Aktienmärkte. Die hält er für vollkommen degeneriert und mehr oder weniger blind auf die Aktionen der ZBs schauend (Zinsen hoch – schlecht, Zinsen runter – gut).

Aus seiner Sicht hat wieder alles mit nem globalen Liquiditätsengapss im letzten Herbst angefangen, der zur Verringerung des globalen Handels geführt hat und jetzt kumuliert in den nationalen Volkswirtschaften ankommt.

Und die Banken haben aufgrund des Aufschreckens durch die SVB plötzlich alle Panik und kaufen “Sicherheit” was das Zeug hält. Deleveraging aller Positionen soweit es geht. (Er zieht Parallelen zu Bear Stearns.)

Mal schauen. Muss irgendwie die Balance zwischen Deleveraging und Zugreifen bei den sich bietenden Chancen hinbekommen…

@Stoertebekker

“Muss irgendwie die Balance zwischen Deleveraging und Zugreifen bei den sich bietenden Chancen hinbekommen…”

Wieso “Deleveraging”? Arbeiten Sie etwa beim Spekulieren mit Fremdkapital?

@Stoertebekker:

Mit Rezession hat das nichts zu tun. Es ist das Ende der Ära des billigen Geldes. Es gibt keine fast zinslosen Kredite mehr und die Opportunitätskosten der Investoren sind massiv gestiegen. Letzten Herbst gab es bereits fast 5% auf 2Y-Treasuries.

Auf der Suche nach Rendite waren Investoren gezwungen in risky assets zu investieren und die VCs konnten sich vor Zuflüssen kaum retten. Das ist einfach vorbei. Es gibt viel weniger neues Finanzierungskapital als vorher.

@Jacques

Wenn man in die echte Wirtschaft schaut, gab‘s sowieso keine fast zinslosen Kredite. Die Banken haben schön nach Bonität der Kreditnehmer unterschieden und LIBOR + x verlangt. Was im Finanzbereich läuft, ist ne andere Kanne Bier.

Hier geht‘s aber um Realwirtschaft. Hab selbst einen syndizierten Kredit gesehen, der im Frühjahr 22 das x bei 2,0 hatte (Beginn der Verhandlungen) und im Herbst um 0,5 höher ausgegeben wurde. Nicht, weil der Schuldner plötzlich irgendwie schlechter aufgestellt war, sondern weil die Aussicht fürs Geschäft eingetrübt waren.

Wir reden hier viel zu häufig über die Finanzwelt und übertragen unreflektiert auf die Realwelt. Die Rezession (wieder Realwirtschaft) kommt bzw. ist schon da.

“eine große Zinswette die schiefgegangen ist.”

Bei SVB war wohl die Qualität der Assets nicht das Problem. Also dürfte per Saldo doch entweder das Geschäftsmodell ab Mitte 2020 zu hinterfragen sein oder es liegt ein Versagen der Aktiv-Passiv-Steuerung vor, also ein Managementfehler.

Der EZB muss man zu Gute halten, dass bereits Mario Draghi vor diesem Szenario der möglichen schnellen Änderung der Zinsstrukturkurven gewarnt hat.

Auch bei der CS ist ersichtlich, dass es Managementfehler waren, die zum Fiasko führen, wobei natürlich zu beachten ist, dass die CS ein großer Konkurrent der US-Investmentbanken ist und daher das Handeln der SEC wahrscheinlich auch unter diesem Aspekt zu betrachten ist.

Die Frage, wie die Einlagen zu betrachten sind, ergibt sich im Nachhinein. Da die VC-Community unter sich extrem vernetzt ist, sehr zentriert in Californien sitzt und einen großen Einfluss auf die Unternehmen ausübt, in die sie investiert, ist das Klumpenrisiko auf die Einlagen viel größer als angenommen. Zusätzlich kommt hinzu, das elektronisches Banking in Sekundenschnelle erlaubt, Einlagen zu bewegen. Ein Tweet an x-Benutzer ist schnell abgesetzt und handeln dann x-Benutzer, so werden Einlagen von x- Bankkunden auf einmal / tagesgleich bewegt. Es handelt sich also um einen elektronischen Bankrun. Diesen kann eine Bank in einer solchen Konstellation nicht erfüllen, also muss zwingend die Schließung erfolgen.

Die Übernahme durch die FDIC ist folgerichtig, da doch sehr viele Tec-Start-Up-Firmen von den Krediten abhängig sind und auch in Zukunft abhängig sein werden. Ferner ist das Risiko aufgrund der Aktiva auf die Zinsänderung bzw. den Zinsverlust begrenzt, also überschaubar.

Richtig ist auch, dass das Bankmanagement strafrechtlich zur Verantwortung gezogen wird. Gleiches hätte auch in der Subprime-Krise für alle Beteiligten gelten müssen, auch in Deutschland.

“Die Übernahme durch die FDIC ist folgerichtig …”

Auch für die Deposits > 250.000 $, die angeblich voll entschädigt werden? Obwohl die Absicherung eben genau da aufhört. Hier werden, wenn es so kommt, Milliardäre und ihre Investitionen gerettet.

Glauben Sie, in Europa würde bei > 100.000 € das auch geschehen?

@ Beobachter

UK hat das Problem geschickt durch die Übernahme des dortigen SVB-Teils durch die HSBC geregelt.

VC-Investoren sind nicht alle Milliardäre. Diese sammeln das Geld wiederum ein.

Wichtig erscheint mir der Gedanke: Wenn das Geschäft der Finanzierung nicht mehr angeboten wird, stirbt das Start-up in Cal. aus / wird reduziert, es droht ein industrieller Totalausfall.

Bei einer Vollpleite wäre wohl das Vertrauen in die mittleren Banken zerstört worden. Dass hätte einen vermehrten Kollaps von kleinen und mittleren Banken ausgelöst.

Sicherlich kann hinterher immer die bessere Lösung gefunden werden. Aber in der Sekunde der Entscheidung halte ich das Vorgehen der US-Behörden für gut. Aufgrund der guten Assets war das Ausfallrisiko absehbar.

@Beobachter

“Hier werden, wenn es so kommt, Milliardäre und ihre Investitionen gerettet.

Glauben Sie, in Europa würde bei > 100.000 € das auch geschehen?”

Das hängt natürlich ganz davon ab ob die superwoke “Berliner Hipster Bank” aus Kreuzberg in Schwierigkeiten ist oder bloß irgndeine doofe holländische Bauernbank…

@Gnomae

“VC-Investoren sind nicht alle Milliardäre. Diese sammeln das Geld wiederum ein.

Millionäre sind aber schon viele unter ihnen, oder?

“Wichtig erscheint mir der Gedanke: Wenn das Geschäft der Finanzierung nicht mehr angeboten wird, stirbt das Start-up in Cal. aus / wird reduziert, es droht ein industrieller Totalausfall. ”

Oh nein! Kalifornien ist doch der einzige Ort in den USA, wo Startups entstehen können! Wer soll denn sonst das nächste Social Platform für vegane Kochvideos entwickeln und vermarkten?

@Carsten Pabst

Je mehr Experten Beruhigunsfloskeln absondern & ” ruhige Hände” an-mahnen, desto kritischer die Lage.

Mein Lieblingsautor N.N. Taleb hält sich zurück, am besten sind seine Kommentare zu bitcoin .

Er hasst ungebildete Anleger, ich bewundere immer seine erlesene Höflichkeit:

Nassim Nicholas Taleb

@nntaleb

Most of us who went into finance in the 80s knew in great detail what happened in the 60s, 40s, 20s & even the 19th century. Some of us studied EVERY recorded past crisis.

We are seeing VCs & hotshots like my two recent preys who don’t even know what really happened in 2007.

11:38 nachm. · 14. März 2023

·

Und hier auch nochmal eine gute Aufarbeitung der Probleme rund um die SVB:

https://www.youtube.com/watch?v=ASoOnVhtKjU

Naja, so gut finde ich das Video nicht. Es blendet die systematischen Risiken im Bankensektor aus. Alle auf DCF Basis bewerteten Assets sind im Wert gesunken. Haben Banken diese als Sicherheit akzeptiert, haben sie das gleiche Problem. Zu nennen sind hier insbesondere Gewerbe Immobilien. 100% Finanzierungen sind hier keine Seltenheit. Hinzu kommen Probleme bei der Vermietung, energetischer Sanierungsstau und kurzlaufende Finanzierung aufgrund des Geschäftsmodells, diese Immobilien schnell weiterzuverkaufen.

Aber mit steigenden Zinsen konnte ja wirklich niemand rechnen. Dass jetzt ausgerechnet die SNB die CS mit 54 Mrd. CHF retten muss, ist schon interessant, hatte diese doch selbst 2022 einen Verlust in Höhe von CHF 132 Mrd. gemacht. In der Welt der Zimbabwean School of Economics alles kein Problem. Mal schauen was die EZB heute macht.

Wer sich den max. Chart von der Bank ansieht, kann den sehr langsamen Anstieg über viele Jahre …dann die relativ kurze schnelle “Übertreibung” nach Oben …und die nachfolgende relativ kurze schnelle “Übertreibung” nach Untern….mit dem Finalen sehr schnellen heftigen Absturz anschauen.

Absolut alles im normalen Bereich eines” Aktienlebens” und des simplen Aktienmarktes !

Flassbeck stellt die richtige Überlegung und Fragen und verfällt nicht der üblichen Medienpanik:

https://www.relevante-oekonomik.com/2023/03/15/bankrun-in-kalifornien-wegen-zu-vieler-staatskredite/

Nebenbei bevor die CS-Medienpanik zum Forenthema wird :

Man vergleiche mal die Bank-Aktienkurven von Anfangs 90er Jahren von CS und Deutscher Bank (frappant ähnlich)… ! :-)

@weico

“Flassbeck stellt die richtige Überlegung und Fragen”

Nein. Ein ganz schwacher Artikel von Flassbeck.

“Die kurzfristigen Verluste treten ja nur auf, wenn die Einleger verrückt spielen und die Anleihen schnell verkauft werden müssen. Das erklärt aber nicht, warum die Einleger plötzlich in Panik geraten. Die FT weist zu Recht darauf hin, dass die aktuelle geringe Bewertung der Staatsanleihen lange vor dem Run bekannt war. Ich jedenfalls würde nicht nervös werden, wenn ich mein Geld bei einer Bank hielte, die vorwiegend Kredite an den Staat gegeben hat, von der aber sonst nichts Nachteiliges bekannt ist.”

Er kapiert nicht, dass eine Bank zwangsweise geschlossen wird, wenn ihr Eigenkapital unter die festgelegten Eigenkapitalgrenzen fällt und sie kein frisches Eigenkapital auftreiben kann – und dass eine Bank Eigenkapital schmälernde Verluste realisieren muss, wenn sie Staatsanleihen mit Kursverlust verkaufen muss um sich Liquidität zu beschaffen. Und wenn das Eigenkapital sogar negativ wird, dann sind die normalen Forderungen (also auch die Kontoguthaben der Kunden) nicht mehr komplett erfüllbar und dann droht der gefürchtete “Bail-in” für die Bankkunden, quasi das Zypern-Szenario, wenn Sie sich noch daran erinnern.

@Hr. Ott:

>Ich jedenfalls würde nicht nervös werden, wenn ich mein Geld bei einer Bank hielte, die vorwiegend Kredite an den Staat gegeben hat, von der aber sonst nichts Nachteiliges bekannt ist.

Ohne Ahnung lebt’s sich halt entspannter ;)

Mir gefällt Alden’s Charakterisierung in ihrem aktuellen Newsletter: “From a depositor perspective, banks are basically highly-leveraged bond funds with payment services attached, and we treat it as normal to keep our savings in them. To help normalize that and make it seem less weird, the FDIC provides insurance against deposit losses up to $250,000 which mitigates some of the risk.”

Es bestätigt sich wieder einmal: Don’t panic. But if you panic, panic first.

@Richard Ott

“Er kapiert nicht, dass eine Bank zwangsweise geschlossen wird, wenn ihr Eigenkapital unter die festgelegten Eigenkapitalgrenzen fällt und sie kein frisches Eigenkapital auftreiben kann – und dass eine Bank Eigenkapital schmälernde Verluste realisieren muss, wenn sie Staatsanleihen mit Kursverlust verkaufen muss um sich Liquidität zu beschaffen.”

Ich denke Flassbeck kennt die Eigenkapitalrege sicherlich gut:

“Die neuen Basel-III-Regeln sehen vor, dass Banken über Eigenkapital in Höhe von mindestens 8% ihrer risikogewichteten Aktiva verfügen müssen. Ab dem 1. Januar 2019 müssen die größten „systemrelevanten“ Banken eine Quote von 11,5 bis zu 13,0% und die meisten anderen Banken eine Quote von 10,5% erfüllen.”

Der verlinke Video von Carsten Pabst erklärt den medialen Herdentrieb wirklich toll:

https://think-beyondtheobvious.com/stelters-lektuere/der-zusammenbruch-der-svb-einfach-erklaert/#comment-300477

@weico

“Ich denke Flassbeck kennt die Eigenkapitalrege sicherlich gut:”

Wenn er das weiß und auch versteht, wieso schreibt er dann in seinem Text, dass er sich keinen sachlichen Grund für das plötzliche Abziehen der Einlagen vorstellen kann?

Flassbeck hat das Problem noch gar nicht kapiert.

@Thomas M.

“Mir gefällt Alden’s Charakterisierung in ihrem aktuellen Newsletter: “From a depositor perspective, banks are basically highly-leveraged bond funds with payment services attached, and we treat it as normal to keep our savings in them. To help normalize that and make it seem less weird, the FDIC provides insurance against deposit losses up to $250,000 which mitigates some of the risk.””

Das Schlimme daran ist ja: Wenn man einer solchen dubios agierenden Organisation namens “Bank” Geld gibt, bekommt man viel weniger Rendite als wenn man der Investor in einen Hedge Fonds mit der gleichen Strategie ist…

Erinnert mich iwie an:

” “How did you go bankrupt?” Two ways. Gradually, then suddenly.”

― Ernest Hemingway, The Sun Also Rises”

Naja, bestimmt nur Koinzidenz … 🤷♂️

LG Joerg

Das Team war auch nicht so schlecht, mit Ausnahme eines erheblichen Managementfehlers, der sich als tödlich erwiesen hat.

Diesen tödlichen Fehler wird man evtl. dann bei den heimischen Sparkassen ab ca. 2024 erleben. Ich kenne genug in meinem persönlichen Umfeld,

die in den Jahren ab 2014 gebaut haben, Zinsen 10 Jahre fest bei einem Prozent Tilgung.

https://www.baufinanzierung-xpert.de/aktuelle-bauzinsen-zinsentwicklung/

Kaum Eigenleistung, Häuser in kürzester Zeit bauen lassen, Bäder gleichen Wellnessoasen,

Außenanlage fix und fertig durch den Galabauer und anschließend ab in den Urlaub. Bauen schlaucht ja ungemein! Let build- Life- Balance…

Das Schlachtfest wird nicht mehr lange auf sich warten lassen.

Und dann können wir schreiben:

Die Kreditvergabe lief eigentlich sehr erfolgreich, mit Ausnahme eines kleinen Problems: Das Tilgen erwies sich doch schwieriger als gedacht😉

Beste Grüße

Carsten Pabst

@Herr Pabst

Das ist dann aber mal wieder eine schöne klassische Immobilienkredit-Bankenkrise.

Aber wo die Gefahr wächst, da wächst das Rettende auch: Die Sparkassen könnten diese schönen Immobilien gleich übernehmen und an ihre Eigentümer, also die Landkreise, weitervermieten. Die suchen doch gerade verzweifelt zusätzlichen Wohnraum für Migranten in unser Sozialsystem. ;)

Hallo Herr Ott,

da ist doch jetzt genug Masse zum Ausbau vorhanden in den Landkreisen:

https://www.spiegel.de/wirtschaft/unternehmen/abschied-vom-mythos-kaufhaus-a-8a6ff9ae-21cb-4c03-adb4-950d9e547139

Alles muß raus, neues muss rein!

@C Pabst

Moin, na mal sehen. Die 2014er und 2015er erwischt es vielleicht.

Aber ich sehe folgendes Szenario: die hohen Preise (Supply chain, Angebot/Nachfrage, Sie wissen schon, keine monetäre Inflation😉🙃) fahren die Wirtschaft langsam runter. Geht zumindest in der Chemie schon massiver los.

Die ZBs führen das auf die Wirkung ihrer Zinserhöhungen zurück (die lt. eigener Aussage eigentlich erst mit 24-36 Monaten Zeitverzug wirken) und verlangsamen den Zinsanstieg bzw. kehren um. Das SVB/CS-Schauspiel verstärkt diese Überlegungen.

Wir kommen zurück zur Situation vor/in der Pandemie – anämische Wirtschaft allerorten. Und China zieht auch nicht an. Konsequenz?

Na klar, Zinsen senken und QE. Und die Häuslebauer können sich in den von Ihnen gebauten Wellness-Oasen und Hightech-Küchen bei Latte irgendwas auf den nächsten Urlaub in …, tja, das ist dann nicht so einfach, freuen. Wette gefällig?

PS Mich amüsiert ja schon ein wenig, dass die aktuelle Bedrohung nicht von den hier rauf und runter diskutierten Zombies und faulen Krediten bei den Banken kommt. Sondern von einer Kombination aus fehlendem qualifizierten Risikomanagement bei SVB, einer Fed, die Rezessionsgefahren mit Zinserhöhungen bekämpft und einem ordinären Bankrun der Großfinanz. 😲

Die gehören alle abgeschafft bzw. zumindestens eingehegt.😉

Hallo stoertebekker,

das Szenario nennt man dann wohl Katastrophenhausse?! Oder was spricht dagegen😉?

Beste Grüße

C.Pabst

@C Pabst

Katastrophenhausse ist schön. Ob’s so kommt 🤷♂️

Aber ich halt mich an J Snider, der hat die Wirtschaftswelt aus meiner Sicht besser verstanden als jeder andere. Und auch aktuell recht behalten hat. Seit Herbst weist er auf drohendes Ungemach hin. (Zudem kann ich seine Podcasts super beim langsamen Werden meines ersten Dachsbarts nebenbei hören.)

Er erwartet weitere Liquiditätsverknappung und eine Rezession ohnehin schon lange. Scheint mir plausibel, die Chemie geht damit ja auch schon in die Öffentlichkeit.

Die Frage ist, was man in seinem eigenen kleinen Turf macht. Alles nicht so einfach. 🙃😲

Wenn Snider recht hat, wird’s in Deutschland aber auch übel. Bin gespannt, was die Schönwetter-Klimarettungs-Heizungsabschaltungs-Dämmungs-Koalition dann anstellt.

@Beobachter

Sie wird eine Kehrtwende wie bei der Kohleverstromung vollziehen. So sicher wie das Amen in der Kirche.

@Stoertebekker

“Sie wird eine Kehrtwende wie bei der Kohleverstromung vollziehen.”

Unterschätzen Sie die motivierende Kraft von Ideologie nicht.

Unsere Regierung importiert auch immer weiter Migranten in unser Sozialsystem, obwohl viele Kommunen nicht einmal mehr Wohnraum für die zu versorgenden Neuankömmlinge finden.

Lieber Herr Pabst,

wenn die Zinsen steigen: Mini-Jobs (bei Partnern gleich zwei) beim Italiener um die Ecke; der sucht wohl händeringend Bedienung. Dann kann man auch die Extra-Zinsen wieder stemmen und dem Restaurant ist auch geholfen. Wenn die Vier-Tage-Woche kommt, ist auch genug Zeit da, das alles ohne Wellness-Einbußen zu leisten. Schlagen Sie das doch schon mal vor ;)

Hallo Thomas M,

vollkommen richtig. Aber ich stelle in letzter Zeit immer mehr fest, wenn ich Personen den Spiegel vor das Gesicht halte, stört das das Befinden derjenigen sehr. Das ist auch für mich ermüdend und außerdem mache ich es dann zu meinem Problem.

Habe ich aber keinerlei Lust mehr zu.

Das Problem mit evtl. höheren Zinsen und deren Tilgung ist das WOLLEN.

Aber die Gesellschaft ist so satt und schreit beim kleinsten Gegenwind nach dem Staat. Es wird versucht jeder Schwierigkeit aus dem Weg zu gehen. Anstrengung, Disziplin und die Überwindung von Schwierigkeiten ist leider sehr vielen in der Gesellschaft fremd geworden. Und die Politiker lassen sich nicht lange bitten und schütten mit dem Füllhorn Steuergelder aus. Habe vor kurzem einem jungen Lehrer mal erzählt, dass wir früher jeden 1. und 3. Samstag Unterricht hatten. Da ist dem sein Kiefer auf dem Asphalt aufgeschlagen.

Aber was soll`s. Halte mich da mittlerweile raus. Ist besser für den Blutdruck.

Man könnte natürlich auch anstatt beim Pizzabäcker um die Ecke woanders Geld verdienen:

Kommt im März die Sommerzeit, bleibt`s länger hell für Schwarzarbeit😉

Aber da sind wir ja wieder beim Anfangsproblem. ARBEITEN, sprich Reduzierung der Zeiteinheiten für die Work- Life- Balance zugunsten der Tilgung.

Wer will das schon?!

Dann jammer ich doch lieber wieder rum, wie schlecht die Welt ist. Der nächste Politiker steht schon an der Ecke und bedient sich diesem Problem🤢

Beste Grüße

Carsten Pabst

Hierbei wird immer wieder vergessen, dass sich die Schulden durch die Inflation entwerten. Der Schuldner gewinnt durch die Inflation. Verlierer sind die Guthabenbesitzer, Rentenbesitzer, Vermieter, Arbeiter, usw.

bto: “Das Team war also nicht so schlecht, mit Ausnahme eines erheblichen Managementfehlers, der sich als tödlich erwies.”

Tja, dann war das Team wohl doch nicht so gut…

“Silicon Valley has positioned itself as the preeminent financial institution serving venture capitalists, nascent tech companies, and high-net-worth individuals.”

Und warum sollen ausgerechnet deren Kontoeinlagen auch über der US-Einlagensicherungsgrenze in Höhe von 250.000 $ vom Staat gerettet werden obwohl sie eigentlich einen netten kleinen Haircut hätten bekommen müssen, weil die SVB ja offensichtlich negatives Eigenkapital hat?

Dummheit muss bestraft werden, besonders die Dummheit von Leuten, die sich eigentlich für Profis halten und selbstverständlich auch entprechend bezahlt werden wollen – sonst sehen wir in Zukunft noch viel mehr davon.