Zu viel Geld jagt knappe Anlagemöglichkeiten

Vorgestern warf ich bereits einen Blick darauf, die Geldpolitik auf die Finanzmärkte wirkt. Kernaussage: Die Liquiditätsflut treibt die Börsen, während immer weniger Geld in der Realwirtschaft landet. Heute greife ich das mit zwei Kommentaren aus der FINANCIAL TIMES (FT) auf.

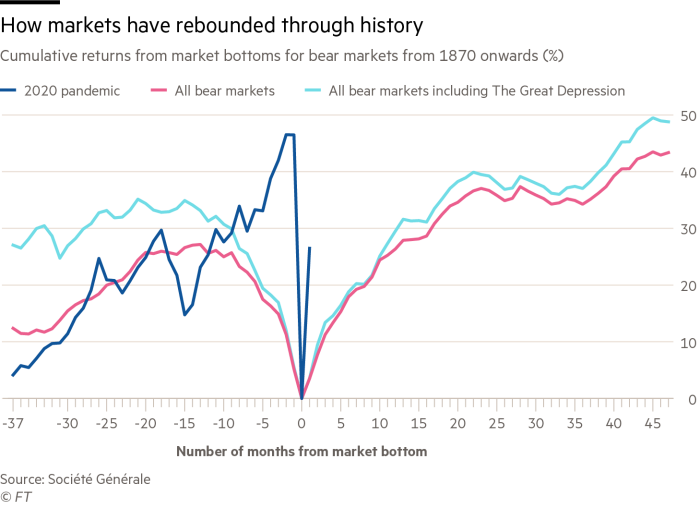

Zunächst die Feststellung der SocGen, wonach Absturz und Erholung der Börsen ohne Vorbild sind:

Quelle: SocGen, FT

Die Abbildung ist spannend. Während die anderen Bärenmärkte mit einem “Rutschen” begannen, haben wir es hier mit einem wirklich dramatisch zu nennenden Absturz zu tun. Viel schneller – und einer ebenso dramatischen Erholung. So schnell ging es noch nie wieder nach oben. Nicht wenige Beobachter meinen, dass dies auch begründet sei, handelt es sich doch um einen Absturz aufgrund von Maßnahmen zur Bekämpfung einer Pandemie, die befristet sind. Danach sollte es weiter wie zuvor gehen. “This is a policy-induced downturn, and the speed and structure of the recovery could follow a different route from previous downturns”, zitiert die FT Paul Donovan, den Chefvolkswirt von UBS Wealth Management.

Die Analysten der SocGen, die die Analyse durchgeführt haben, sind skeptischer: “Under the team’s most conservative scenario, the S&P 500 would end the year about 7 to 8 per cent lower than its current levels.” Wozu ich sagen würde, dass das Risiko dann selbst aus Sicht der Franzosen nicht hoch ist, denn sieben bis acht Prozent tiefer gegenüber heute ist keine große Nummer.

Was mich zum anderen Beitrag aus der FT führt. John Dizard geht der Frage nach, was denn hinter dem Aufschwung steht.

- “While institutions and markets have been kept from imploding by the wall of money the Fed and other central banks have thrown at the economy, they still do not have clear long-term prospects. (…) Are we in a long-term deflation or disinflation?” – bto: mit der sich daraus ergebenden Standardantwort: bei Deflation weiter Anleihen und Steigerung der Renditen mit Leverage, im Falle von Inflation Gold und Aktien von Unternehmen mit hohem Kapitalumschlag.

- “Of all the scenarios (…), the most popular is a relatively quick return to ‘normalcy’. That means a rapidly developing V-shaped recovery under which one could go back to considering algo-generated combinations of stock and bond indices for the clients, so their long and comfortable retirements will be comfortably paid for. That will not be possible.” – bto: in der Tat, sollte es nicht zu einer normalen Erholung kommen. Denn dazu war die Wirtschaft schon vorher zu stark angeschlagen.

- “Our political and central bank leaders do not want us to be so unhappy that we want to change governments too quickly. So the fiscal and monetary authorities have told the public in most advanced countries that we have a short-term liquidity problem. Not enough cash right now, but when the economy restarts, these trillions of dollars of short-term government backed loans can be repaid.” – bto: eine These, die ich bekanntlich für falsch halte.

- “Unfortunately, demand for goods the money can be spent on has disappeared, as businesses, rationally, can see no reason for new capital spending to meet market demand that does not exist. And nobody is taking first-class trips to New Zealand or Disney World. The supply of more modest goods and services that can be bought with the cash made available by central banks and government grants is also in short supply. They are rationing burgers at Wendy’s fast food stores in America, and you cannot buy a new mobile device at Apple stores in Europe affected by closure orders.” – bto: Also wirkt das Geld stabilisierend auf die Finanzmärkte, weil Pleiten verhindert werden, aber nicht auf die Realwirtschaft. Da die Liquidität aber irgendwo hin will, landet sie eben an den Börsen.

- “This helps explain the ‘recovery’ in asset prices over the past month and a half or so. There is no productive use for the liquidity injection, and not much supply of desirable goods available, so money has gone into speculation in securities markets. This has raised the prices of shares and bonds above reasonable levels, so what do you do when you next sit down in front of your personal-account trading screen?” – bto: Hinterherlaufen dürfte keine gute Idee sein. Denn viel Raum nach oben dürften die Märkte nicht haben.

- “Treasuries will not disappear or instantly crash. They are too much needed as collateral for other transactions. But the rally is finished. Over time, their principal and interest payments will be eroded by inflation, as all that liquidity finds its way into the prices of goods and services.” – bto: Interessanterweise spricht auch er von höherer Inflation, vor der wir stehen. Ich denke, dies zu Recht.

- “Gold sounds like a great hedge for uncertain times. If you can carry it from one place to another. It is physically very heavy and in short supply as it moves from its incarnation as jewellery and transient art through several forms of gold bullion. Until you have a safe guarded by a trusted thug, you are better off with an ETF.” – bto: Ich fürchte allerdings, dass alle Formen von Papier-Gold auch gefährdet sind. Ich denke, dann lieber Goldminen als der Hedge für den Fall, dass Gold als solches besitzmäßig eingeschränkt wird.

- “Then we have Chinese government bonds. (…) China has the second-largest government bond market in the world, with an American-scale $10tn-plus in issuance across the curve. So far, its fiscal and monetary management has been among the most conservative of major countries in the post-Covid-19, post-recession world.” – bto: Interessant, ich sehe aber immer noch das Risiko einer Abwertung. Andererseits hält sich das Gerücht einer Goldbindung der chinesischen Währung, was ich allerdings nicht so recht glauben mag.

- “Assuming any of these insightful investment concepts work, and you realise large dollar, sterling or euro-denominated profits, you can sell your positions and reap your reward: more cash when there is not much to buy.” – bto: :-) Ja, so fühlt es sich am Ende des langen Weges von zentralbankmanipulierten Märkten an.

→ ft.com (Anmeldung erforderlich): “Strategists query sudden ‘sprint’ in US stocks”, 11. Mai 2020

→ ft.com (Anmeldung erforderlich): “Too much cash is chasing too few desirable assets”, 8. Mai 2020