(Wie) Wirkt die EZB Politik?

Vorletzte Woche habe ich mich intensiv mit der Geldpolitik beschäftigt. Heute werfe ich nochmals einen Blick auf das Thema und gehe der Frage nach, ob die Politik der EZB “wirkt” und zwar in der Realwirtschaft – und wenn ja wie. Der Telegraph zitiert in diesem Zusammenhang eine neue Studie.

- “Setting monetary policy for nations as diverse as export-heavy Germany and stagnant Italy is, in the view of many analysts, an impossible task. A few years ago a senior analyst at JP Morgan used World Economic Forum data and found the 13 random countries of the world beginning with the letter ‘M’ – from Madagascar to Mexico – were more suited to a currency union than the members of the euro.” – bto: Die Studie habe ich auch schon mehrfach an dieser Stelle zitiert. Nachdem es in den vergangenen Jahren zu mehr Divergenz gekommen ist, dürfte es für die Eurozone noch schlechter aussehen.

- “(…) Draghi can reasonably claim to be the individual most directly responsible for keeping the entire project on the road. (…) His big bazooka – potentially hundreds of billions to prop up the sovereign debt of Eurozone strugglers through so-called Outright Monetary Transactions – was never needed, because bond markets afraid to take on a 600lb gorilla with unlimited firepower never called his bluff.” – bto: Diese Einschätzung teile ich. Nur hat Draghi damit die Krise unterdrückt, nicht gelöst und die Probleme sind immer weiter angewachsen.

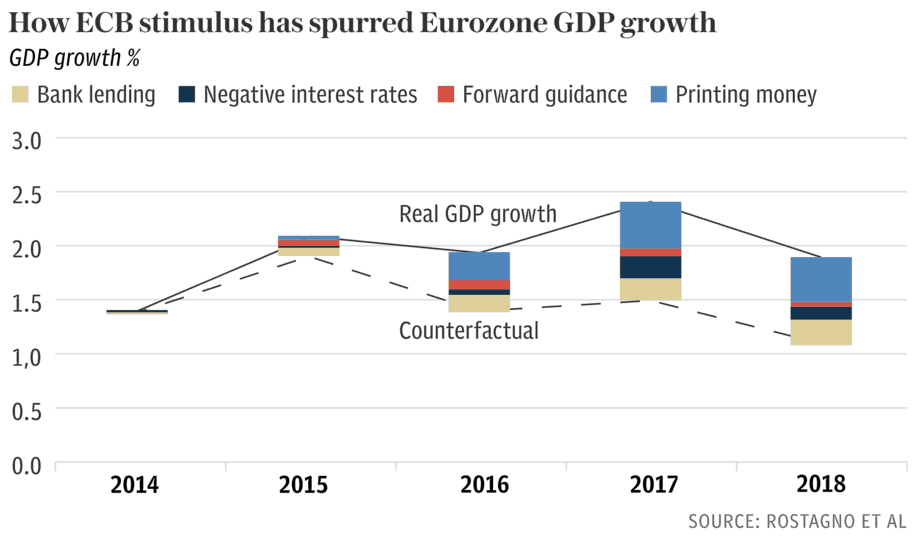

Dazu zeigt der Telegraph diese Darstellung, leider, ohne sie weiter zu kommentieren. Dennoch fand ich sie so interessant, dass ich sie hier bringe (der Rest des Artikels vom Telegraph enthält auch nicht viel Erhellendes):

Quelle: Telegraph

Die Darstellung zeigt einen Vergleich eines fiktiven BIP-Wachstums (“counterfactual”) mit dem tatsächlichen Verlauf. Demnach hat die EZB das Wachstum um rund einen Prozentpunkt erhöht. Quelle für diese Einschätzung ist die EZB selbst. In einem Paper versuchen die Analysten der EZB nachzuweisen, wie die Maßnahmen der EZB wirken. Leider ist das erst “forthcoming” also noch nicht erschienen, wenn man auf der Webpage der EZB nachschaut. Sobald es verfügbar ist, werde ich es bei bto besprechen.

Was mich zum Ende des Artikels im Telegraph führt:

- “(…) inflation falls consistently short of the ECB’s targets of ‘close to 2pc’ amid moribund growth.The central banking chief has tried almost everything: interest rates went negative in 2014, (…) Cheap funding lines for banks, so-called ‘targeted longer-term refinancing operations’ (TLTROs) has seen a total €750bn injected in two tranches in 2014 and 2016, (…) Arguably his biggest achievement was getting a quantitative easing program away in 2015, (…) That now stands at €2.6trn and is likely to be restarted in October.” – bto: Und mit Lagarde kommen Helikopter und MMT.

- “Professional economists surveyed by the ECB also predict an undershoot, stoking fears over a creeping ‘Japanification’ of the eurozone. (…) The fact is we have structural factors are forcing inflation down. The Eurozone suffers from a permanently weak economy and people have got very little confidence it will grow at a sustainable rate to raise inflation pressure. After all a central banker can only do so much with monetary policy when fiscal firepower is needed. (…) Draghi has also called all but explicitly for those countries with ‘fiscal space’ – that is, Berlin – to open the taps.” – bto: Das stimmt zwar, vergessen sollte man aber nicht, dass es selbst, wenn wir Schulden machen, nichts an der Tatsache ändert, dass der Euro fundamental nicht funktioniert.

- “Experts suggest for example that Lagarde, if needed, could change the quantitative easing rules which currently limit the ECB to buying 33pc of the various bonds it buys. If Draghi’s ‘whatever it takes’ moment years ago saved the euro, his successor needs some of that spirit to finally get to grips with the eurozone’s lingering inflation pain.” – bto: Und daran zweifle ich keine Sekunde.

-