Wie die EZB ihre Rolle im Klimaschutz begründet

Die EZB und der Klimaschutz – interessantes Thema, stellt sich doch die Frage, wie eine Zentralbank den Klimawandel bekämpfen kann. Nun, wir wissen es: indem sie Geld zur Verfügung stellt und damit genau das macht, was die Politik ohnehin möchte: die Wirtschaft beleben. Und genau das bekommen wir nun. Martin Sandbu in der FINANCIAL TIMES (FT) ist hier in seiner Argumentation verlässlich. Immer wieder spricht er sich für mehr EZB aus, wenn es um die Themen in Europa gibt. Er sieht auch in der Transferunion eine Lösung, obwohl er es war, der mich auf die Studie des IWF gebracht hat, wonach eine Transferunion in Europa nicht groß genug sein kann, weil die privaten Geldströme fehlen.

- “(…) Isabel Schnabel (…) gave the punchiest argument I have seen for the ECB taking an active role in pushing forward the decarbonisation of the eurozone economy. The key message was that “collective action, by governments, firms, investors, households and central banks, including the European Central Bank, is required to accelerate the transition towards a carbon-neutral economy and correct prevailing market failures”. – bto: Das ist eine klare Aussage. Die Notenbank findet einen Weg, zur Dekarbonisierung der Wirtschaft beizutragen.

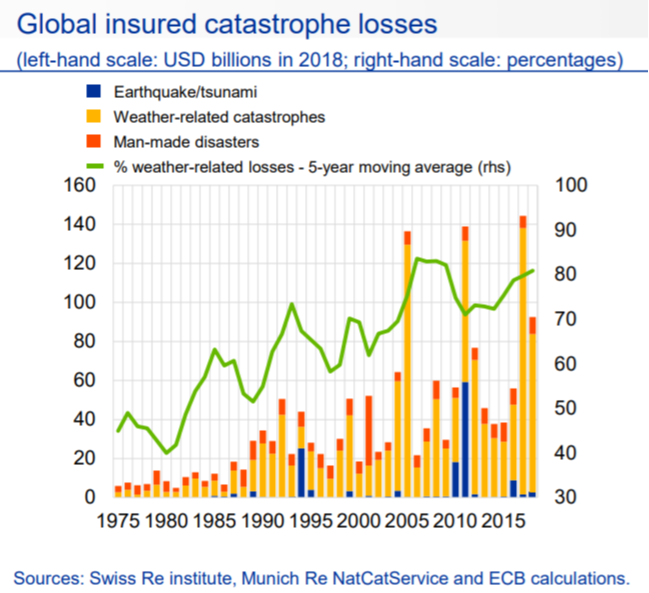

- “(…) the speech brings surprising economic knowledge to the table. Schnabel makes clear that the economic costs of climate change are not just something in the future; they are already with us. Judging from the chart reproduced below, from the 1980s to the past decade average annual insured losses from climate-related catastrophes increased perhaps sixfold.” – bto: Das führt mich zu der Frage, ob man das so sagen kann. Wir haben doch in den letzten 50 Jahren Folgendes auch erlebt: Menschen siedeln in Gegenden, in denen sie früher nicht gewohnt haben und sie haben mehr Versicherungen. Ich sage damit nicht, dass es Klimawandel nicht gibt, ich frage aber, ob man diese Zahlen als Beleg nehmen kann.

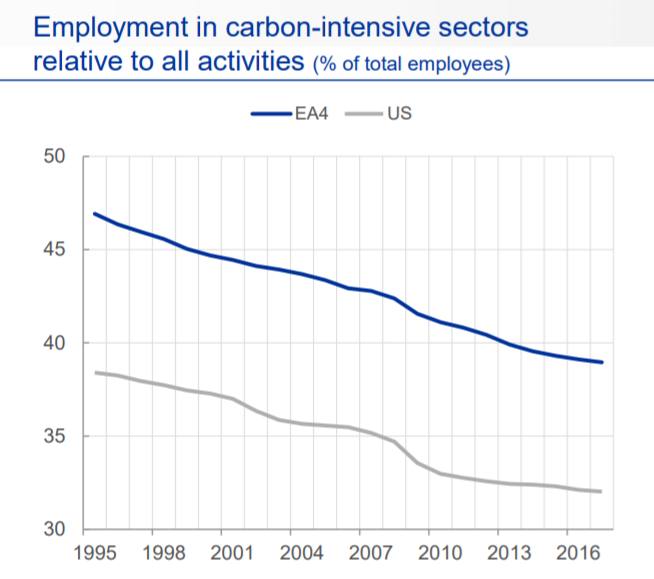

- “Another chart from the speech shows that a larger share of European workers are employed in the most carbon-emitting sectors compared with the US. While the US may have further to go in absolute emissions cuts, Europe may, in other words, have a bigger political challenge in reallocating workers from “brown” to “green” jobs.” – bto: Ursache ist, die USA haben mehr Jobs nach China verloren als die EU. Ist das also ein Grund zur Freude? Offensichtlich fanden das die Wähler in den USA vor vier Jahren nicht. Hinzu kommt, dass es wenig nutzt, weil die Emissionen nun in China anfallen.

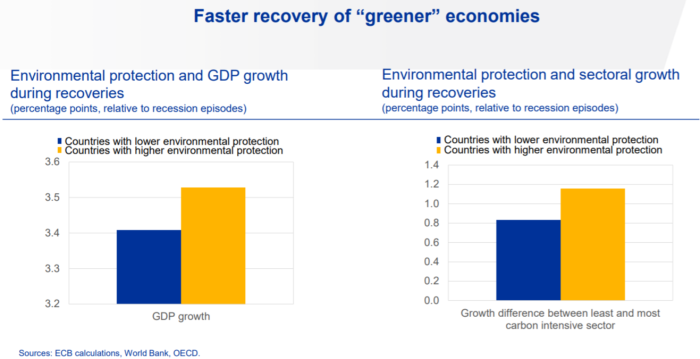

- “At the same time, Schnabel shows that environmental regulation need not hold back growth. In particular, recoveries from recessions are not threatened by decarbonisation policies; indeed, recoveries can be particularly fruitful times to shift the economy from more to less carbon-intensive activities, as the chart below suggests.” – bto: In meiner Zeit bei BCG hätte ich einen Associate mit so einem Chart wieder zurück zum Bearbeiten geschickt. Das sagt nämlich gar nichts aus. Könnte es nicht sein, dass es sich bei den Ländern mit “besserer Umweltschutzregulierung” um genau jene handelt, die ohnehin wirtschaftlich stärker sind? So ist Deutschland da sicherlich enthalten und zieht die EU. Das Chart zeigt also, dass starke Länder sich besser erholen und meist auch besseren Umweltschutz betreiben. Schwach!

- “The most significant line in Schnabel’s speech entails precisely that: “In the presence of market failures, market neutrality may not be the appropriate benchmark for a central bank when the market by itself is not achieving efficient outcomes.” – bto: Da haben wir es. Man muss aggressiv intervenieren.

- “It means the ECB is ready to at least contemplate outright targeting what I have called the ‘green spread’ — the difference in financing conditions for low-carbon and high-carbon activities. Schnabel does not use that terminology, but does present research showing that the green spread is unhelpfully narrow at the moment.” – bto: Dazu brauche ich keine Studie! Wenn Geld generell nichts kostet – auch wegen der EZB –, dann gibt es auch faktisch keine Differenzierung. Vor allem, wenn man davon ausgeht, dass “braun” die Farbe vieler Zombies sein dürfte.

- “(…) monetary policymakers have plenty of tools to target the green spread. Schnabel’s speech mentions excluding bonds from being eligible for ECB collateral or bond-buying, adjusting haircuts (discounts) to reflect climate considerations, and even proposals (in a footnote, but still) for green targeted lending to banks. The central bank’s ability to affect financing conditions for the carbon transition is not in doubt; what matters is whether it wants to do so.” – bto: Das ist doch praktisch, dass die EU nun “grüne Bonds” ausgibt. Da hat die EZB was, was sie kaufen kann …

Der Link zur Rede war auch dabei: → ECB: “When markets fail – the need for collective action in tackling climate change”, 28. September 2020

→ ft.com (Anmeldung erforderlich): “ECB gets ready to target the ‘green spread’”, 1. Oktober 2020