“Why the Next US Recession Could Be Worse Than the Last”

Die nächste Rezession wird sicherlich schlimmer als die letzte. Liegt alleine schon daran, dass der Aufschwung aus der letzten Rezession so schwach gewesen ist, trotz (oder gerade wegen?) der Politik der Notenbanken. Das gilt für Europa wie für die USA. Hier ein Kommentar, der es am Beispiel der USA erklärt:

- “For all the optimism surrounding low unemployment rates and record-high real median income, there are some signs that something is rotten in the US economy. (…) when the next recession comes, there’s reason to believe it won’t be business as usual. The structural problems that led to the 2008 financial crisis haven’t been fixed. If anything, they’ve gotten worse.” – bto: Das gilt erst recht für die Eurozone!

- “The yield curve between short-term and long-term US Treasuries is the flattest it has been at any point in the past 10 years. A flattening yield curve, is a problem in its own right, as is a declining prime-age labor force unable to secure adequate wages. But there are other longer-term forces at work that threaten to make what should be a minor cyclical recession a much more painful and prolonged affair.” – bto: bei uns bekanntlich viel schlimmer!

- “The two most consequential of these forces are increases in total household debt and the continued growth of wealth inequality within the US economy.”

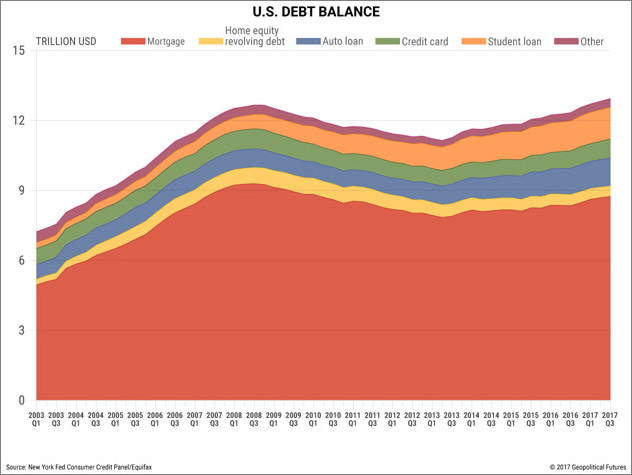

- “Household debt in the United States is now almost $13 trillion. That figure exceeds total household debt at any point during or in the recovery period after the 2008 financial crisis. Housing debt has creeped back to pre-2008 levels. Credit card debt has reached pre-2008 levels too. Student loan debt has skyrocketed by 134 percent since the first quarter of 2008 (about 9 percent on average per year).” – bto: In Europa sind es vor allem die hohen Staatsschulden.

Quelle: Mauldin

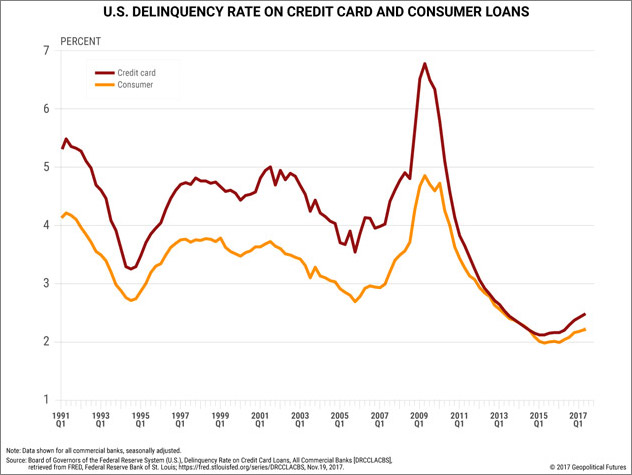

- “Increased household debt, though, doesn’t mean the end is nigh; it just means people are borrowing more money. (…) In the second quarter of 2017, the delinquency rate on credit card loans was 2.47 percent and on consumer loans was 2.21 percent. Low though these rates may be, they are trending upward. Last month, shares of JPMorgan Chase and Citigroup fell on the news that both banks had increased their reserves for consumer loan losses – just under $300 million for JPMorgan Chase and just under $500 million for Citigroup.” – bto: was noch nicht heißt, dass es morgen eine Krise geben muss.

Quelle: Mauldin

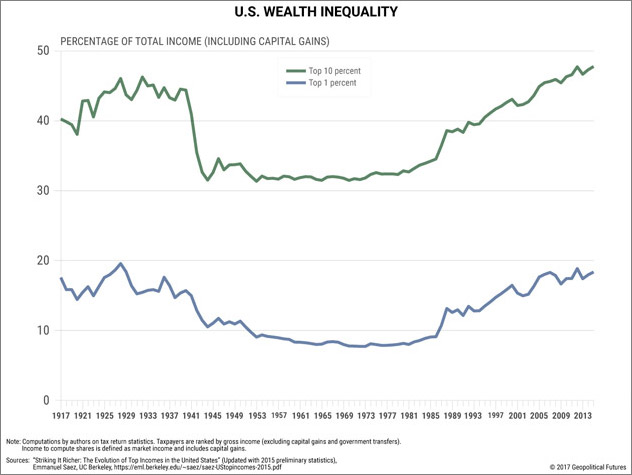

- “More serious than higher household debt, though, is increased income and wealth inequality in the United States since the 1970s. In 2015, the top 10 percent of all US earners accounted for just under 49 percent of total income – a share greater than at any time during the Great Depression. The top 1 percent accounted for 20 percent of total income. This kind of disparity is a refrain in US economic history. It characterized the Gilded Age of the late 19th century as well as the decade or so before the Great Depression. Both were eras of immense wealth generation that benefited only the top, (…).” – bto: was nicht bedeutet, dass es eine Krise gibt, wegen der Ungleichverteilung. Es kann aber eine negative Wirkung auf die Wirtschaft nicht geleugnet werden.

Quelle: Mauldin

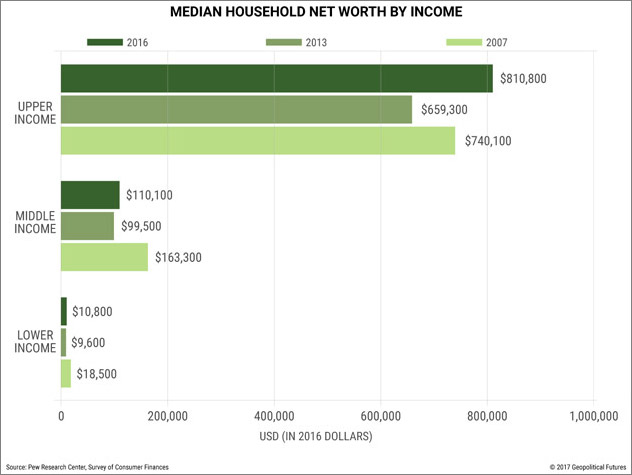

- “According to the Pew Research Center, only upper income families have recouped the wealth they lost during the financial crisis. (…) For those hardest hit, the tales of recovery ring hollow.” – bto: was natürlich nicht funktionieren kann auf Dauer.

Quelle: Mauldin

- “Real median income can rise even as the gap between those above and below the median widens. For example, the share of adults living in middle-income households has fallen since 1970. That year, 61 percent of adults lived in a middle-income household. In 2015, that number had fallen to 50 percent. The share of those living in a low-income household increased by 4 percent, and the share of those living in an upper-income household increased by 7 percent. The underlying problem is wealth inequality, and real median income does not necessarily capture wealth inequality.” – bto: Das ist natürlich ein Kernproblem auch in anderen Ländern und eine Folge der Globalisierung und der Geldpolitik.

Quelle: Mauldin

- “Analysis performed by Pew in 2015, based on the last US census, estimated that in 2012, 60 percent of American households were dual-income households. The purchasing power of the real median income has decreased even as US households have added a second breadwinner to the home.” – bto: was widerspiegelt, dass in den USA fehlende Einkommen durch mehr Arbeit und vor allem mehr Schulden ausgeglichen wurden.

- “For the past 40 years in the US, the rich have been getting richer, the poor have been getting poorer, and the middle class has been disappearing. The crisis of 2008 was a global phenomenon, but in the US, it was also an episode in an era of increasing inequality that began in the 1970s. The American dream was never about just making ends meet – it was about social mobility and giving your children a better life than you had growing up. That is beyond the means of an increasing number of US households. When the next recession comes, it will come as inequality reaches new heights, and if US history is any indication, that will translate into massive political change.” – bto: Das denke ich auch!

→ Mauldin: “Why the Next US Recession Could Be Worse Than the Last”, 20. November 2017