Tiefe Zinsen rechtfertigen keine hohen Bewertungen

Aktien-Bullen begründen die hohen Bewertungen mit den tiefen Zinsen. Eine Argumentation, der ich schon in der Vergangenheit entgegengetreten bin. So hier:

Hier nun ein anderer Beitrag, der zeigt, dass es nur bis zu einem bestimmten Punkt den – erhofften – Zusammenhang gibt:

- “When the financial media continuously repeat an opinion as fact, it spawns a mainstream narrative, which produces a powerful effect on investor psychology. One mainstream narrative, repeated with certainty, is low interest rates cause high stock market valuations, which is supported by the public statements of investment luminaries such as Warren Buffett.” – bto: Es klingt ja auch sehr einleuchtend. Was die Befürworter jedoch vergessen, ist, dass die Zinsen nicht dauerhaft tief bleiben, und damit auch Wachstum und Gewinnsteigerung der Unternehmen.

- “A related mainstream truth is rising rates will cause high stock market valuations to fall. In fact, recently, both Bill Gross and Jeffrey Gundlach have commented on the level of 10-year Treasury rates and why they are destined to go higher. Gundlach even went further, suggesting that if 10-year rates were to rise above 2.63% (currently 2.55%), stock prices would begin to fall.” – bto: Es ist diese magische Grenze, die ich auch schon mehrfach bei bto besprochen habe. Doch gilt sie?

“Are the two ‚truths‘ in bold above supported by the historical record? Believe it or not, the answer is no, as we will explain.”

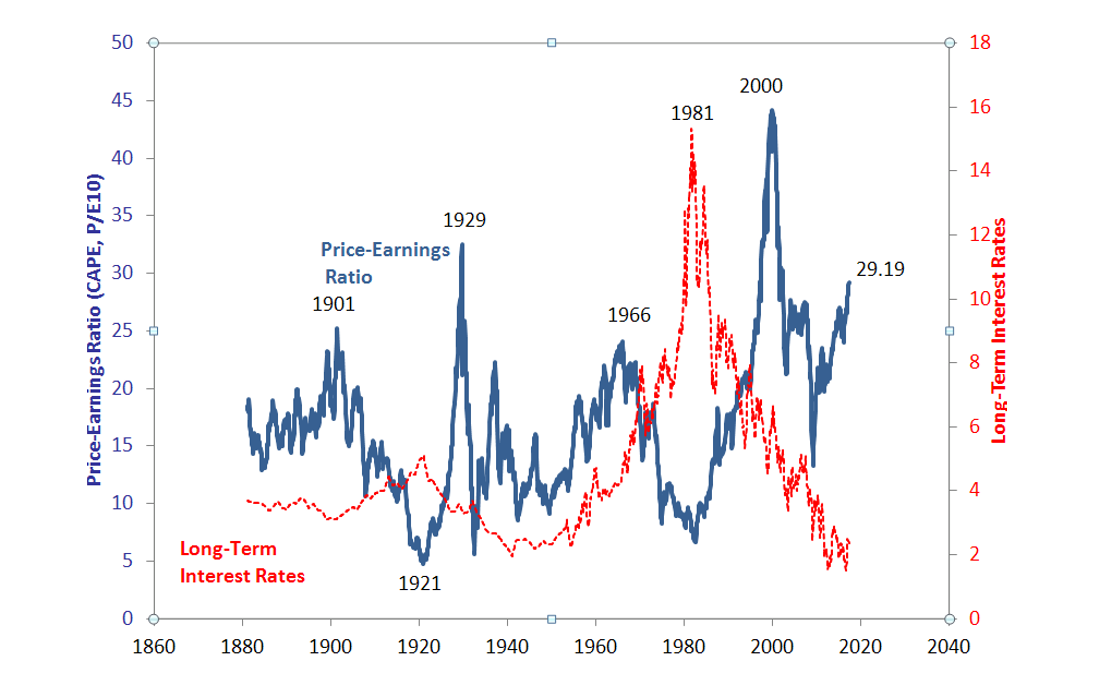

- “Let’s begin by examining stock market valuations. Most professional observers of financial markets would agree that stocks valuations are high compared to their historical range. This fact is demonstrated in the chart of the Shiller CAPE ratio (Cyclically-Adjusted PE ratio) below.” – bto: weshalb man davon ausgehen muss, dass vom derzeitigen Niveau aus auch ohne Crash nur noch geringe künftige Erträge zu erwarten sind.

Quelle: Robert Shiller, multipl.com, Real Investment Advice

- “The CAPE chart is more than a historical chart of valuation. It is also a chart of investor psychology compared to historical norms, because the chart measures the investing public’s fear or mania to “buy” a dollar’s worth of stock market earnings at any point in time.” – bto: Das ist ein ganz wichtiger Aspekt. Die Mehrheit glaubt an das Märchen der bewältigten Krise und der allmächtigen Notenbanken. Ich nicht.

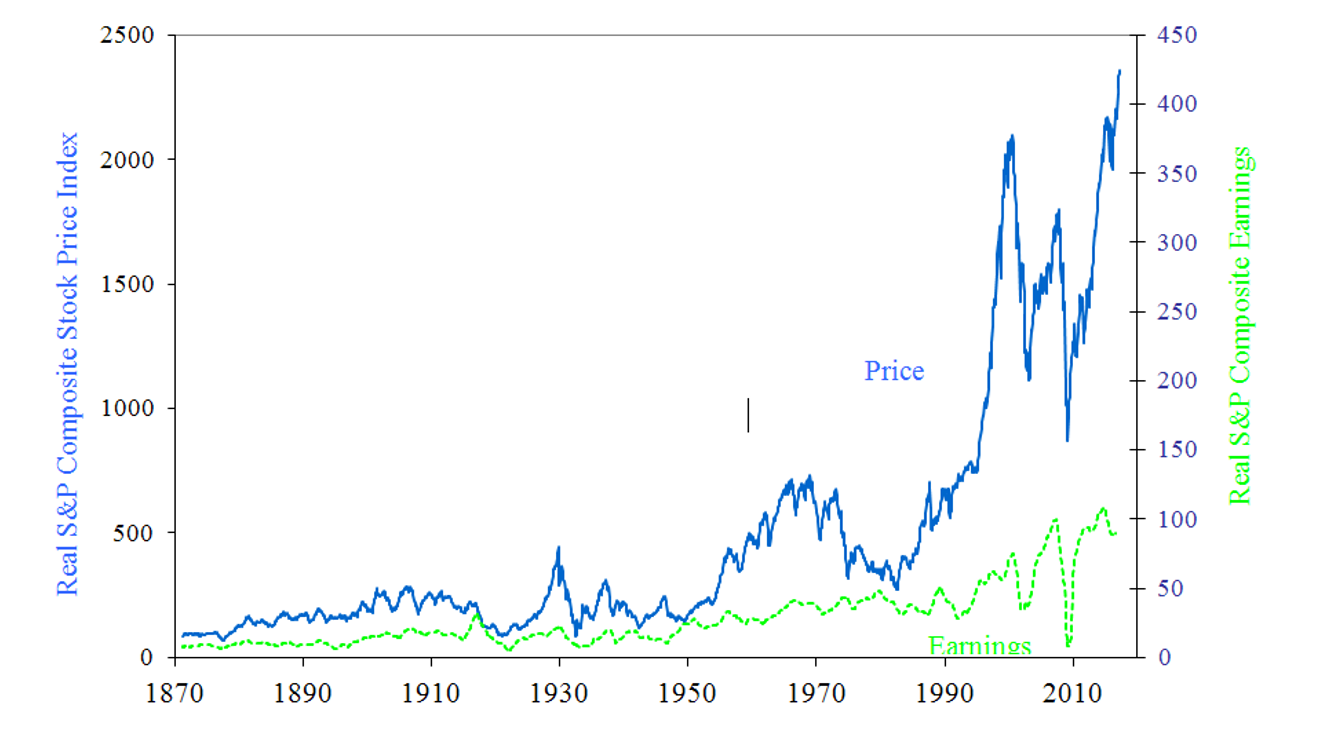

- “The psychological effect on stock prices can also be seen in the chart below, which breaks down the PE ratio into P (price) and E (earnings). When the gap between price (blue line) and earnings (green line) is high, investors are willing to pay high a price to buy a dollar of earnings. (…) Most recently, during the past few years earnings have been flat while stocks were rising dramatically. While bidding up stock prices during this period, it appears investors were expecting a big jump in earnings.” – bto: was natürlich nur dann geht, wenn die Gewinne irgendwann aufholen, zumindest nominell (also durch Inflation). Sonst kommt die unabwendbare Enttäuschung.

Quelle: Robert Shiller, multipl.com, Real Investment Advice

- “When interest rates (Y) are extremely low, it makes intuitive sense that stock prices (X) would be high, because interest rates are a main theoretical factor in the valuation of stocks. Another sensible argument is that prevailing interest rates provide competition for an investor’s dollar relative to an investment in the stock market. For these reasons, when rates (Y) are low, stocks (X) are perceived to be more attractive, relatively.” – bto: Das ist genau die Argumentation, die wir von allen Seiten bekommen.

- “(…) let’s look at the interaction of interest rates and stock valuations over the broad sweep of time. As shown below, extremely high stock market valuations occurred in 1929, 2000, and recently. But interest rates were extremely low only once (recently) during those three occurrences. If low interest rates coincide with extremely high stock valuations only one time out of three, then it is obvious that low interest rates cannot cause high stock valuations.” – bto: Hier bin ich allerdings noch nicht überzeugt. Es könnte doch sein, dass Blasen auch bei normalen Zinsen entstehen, weshalb man eigentlich nur dann eine Feststellung treffen könnte, wenn in Phasen tiefer Zinsen die Börsen nicht immer hoch sind. In den 40er-/50er-Jahren war das so. Umgekehrt gehen die sehr hohen Zinsen in den 70er-/80er-Jahren mit tiefen Bewertungen einher.

Quelle: Robert Shiller, multipl.com, Real Investment Advice

“(…) the statement that low interest rates cause high stock valuations is supported by a .500 batting average in the historical record, which is the equivalent of a coin-flip.

- Extremely high interest rates, which have occurred twice, coincided with low stock market valuations. This fact does not prove that high interest rates ‚cause‘ low stock valuations. But at least the historical record is consistent with such a statement.

- Extremely low interest rates, which have occurred twice, have coincided with high stock market valuations only once; today. The historical record (1/2 probability) does not validate the highly-confident mainstream narrative that low interest rates ‚cause‘ or extremely high stock market valuations.

- Extremely high stock valuations have occurred three times. Only once (1/3 probability) did high stock valuations coincide with low interest rates; today.

- If extremely low interest rates do not cause extremely high stock market valuations, then a rise in rates should not necessarily cause a decline in stocks. That is, the historical record does not support the near-certain mainstream narrative that a rise in rates will torpedo stock prices.

- To demonstrate the ability of a consensus narrative to overwhelm analysis of historical facts and even current reality, consider that the Fed has hiked short-term interest rates five times since December 2015. Also, long-term rates bottomed in mid-2016 and have moved more than a full percent higher. Yet the S&P 500 index has risen more than 30% since the lows in short-term and long-term rates.”

bto: Allerdings gibt es einen Aspekt, den wir nicht vergessen dürfen: die stark gestiegene Verschuldung der US-Unternehmen, die deshalb durchaus negativ auf steigende Zinsen reagieren. Sie sind ein geleverageder Long-Bet. Das muss man bedenken, wenn man heute (US-) Aktien kauft.

→ Real Investment Advice: “Is It True? Do Low Rates Justify High Valuations”, 15. Januar 2017