“The Recession of 2019”

Heute Morgen die New York Times, jetzt in Ergänzung GaveKal, schon früher auf bto mit einer Sicht auf Konjunktur- und Börsenaussichten:

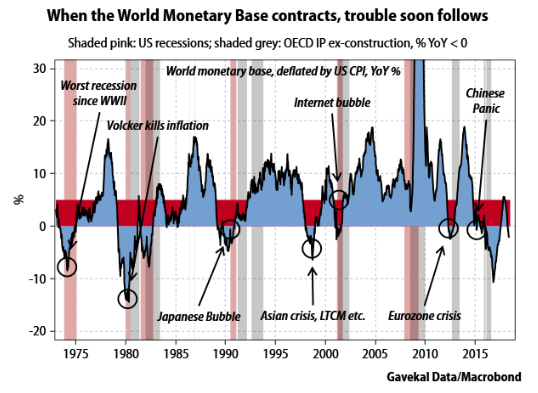

- “(…) I have become increasingly concerned that a recession will hit the world economy in 2019 (…) based on the behavior of (…) the World Monetary Base, or WMB. Every time in the past that this monetary aggregate has shown a year-on-year decline in real terms, a recession has followed, often accompanied by a flock of “black swans.” And, since the end of March, the WMB has again been in negative territory in year-on-year terms. As a result, and as I shall explain, there is a significant risk of a recession next year.” – bto: Und das wäre auf jeden Fall ein Margin Call für die Weltwirtschaft.

- “It starts with the US Federal Reserve, which, because it controls the dominant reserve currency, acts as de facto central bank to the world. (…) The Fed also provides ‚reserves‘ to other central banks. Typically, this happens when the US dollar is overvalued and/or when the US economy grows faster than the rest of the world. This combination leads to a deterioration in the US current account deficit, which means that the US starts to pump more money abroad. These excess dollars appear first in the hands of foreign private sector companies. But if they earn more than they need for working capital, they sell the excess to their local central banks in exchange for local currency. As a result, local monetary bases rise, and the surplus US dollars get parked in central bank foreign reserves, where they show up as a line item of the Fed’s balance sheet called ‚assets held at the Federal Reserve Bank for the account of foreign central banks‘.” – bto: Und da haben wir sie wieder, die zu hohen Schulden. Denn diese entstehen, wenn die Weltliquidität so explodiert.

- “So, if I take the US monetary base, and add to it the reserves deposited by foreign central banks at the Fed, I get my figure for the World Monetary Base. From this aggregate, I can get a rough idea of the pace of base money creation around the world, either through direct intervention by the Fed in the US banking system, or indirectly through US dollar accumulation by foreign central banks. When the WMB is growing, I can be relatively confident about the future nominal growth of the global economy. And when it’s contracting, it makes very good sense to worry about a recession.” – bto: Wenn die Schulden wachsen, ist alles gut. Wenn die Wachstumsrate abnimmt, drohen Probleme.

“(…) it seems likely that the world is entering its seventh international dollar liquidity crisis since 1973:

“(…) it seems likely that the world is entering its seventh international dollar liquidity crisis since 1973:

- Already the usual suspects—Argentina, Brazil, Turkey, South Africa—are having a tough time. (…)

- Already, the US stock market is outperforming all other major stock markets (most of which are actually going down) — a sure sign that the world is starting to suffer from a shortage of US dollars.

- Already the spreads between the US bond market and a number of government bond markets outside the US have started to widen. (…) Unfortunately, the attempt is destined to fail, if, as I believe, the problem is not an overabundance of local currencies but a shortage of US dollars.” – bto: Das kann man allerdings für Europa nicht sagen! Die US-Zinsen liegen deutlich über den deutschen. Da sieht man das Wirken der EZB.

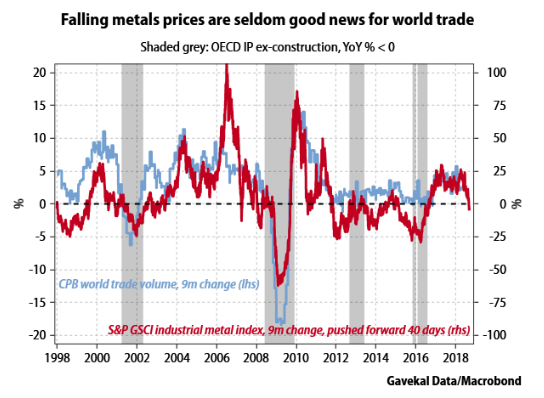

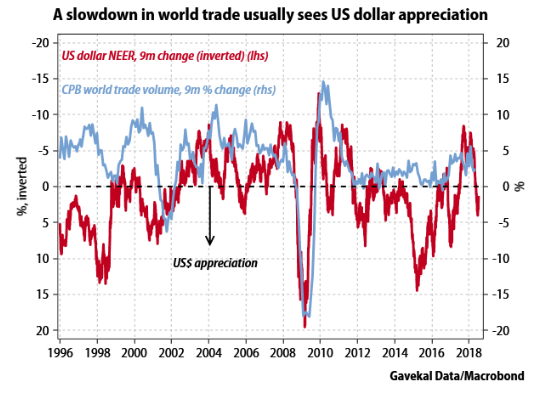

- “The first effect to watch out for is a contraction in international trade as a consequence of the US dollar shortage. Every time in the past that there has been a contraction in the WMB, six or so months later there has been a steep decline in the volume of world trade (at least since 1994 — I only have the data back that far). These declines have almost always led to a recession, either in the OECD, or outside the OECD, as in the case of the Asian crisis. I see no reason why the same should not happen again this time around, especially as I am starting to detect a range of other signs that typically accompany the march towards a recession.” – bto: vor allem, weil die Verschuldung in US-Dollar so zugenommen hat. Es ist halt ein Margin Call.

- “For example, if a recession is coming, it is natural to expect commodities prices to roll over. And as the chart below shows, that is what is happening.” – bto: Auch für die Rohstoffexporteure ist das ein Problem.

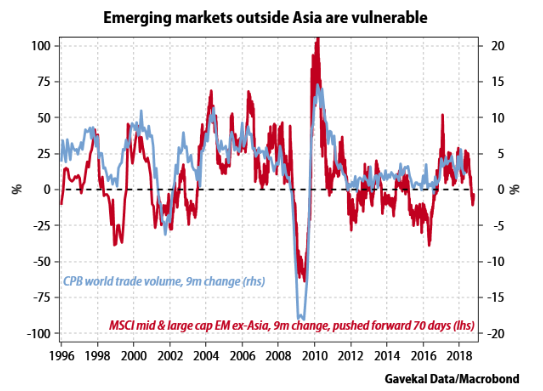

- “When the volume of trade goes down, together with the prices of commodities, commodity-producers (essentially the emerging markets outside Asia) usually see their stock markets tank. And ex-Asian emerging markets have certainly taken a beating recently.” – bto: Und damit wachsen die Probleme weiter, vor allem, wenn man sich verschuldet hat.

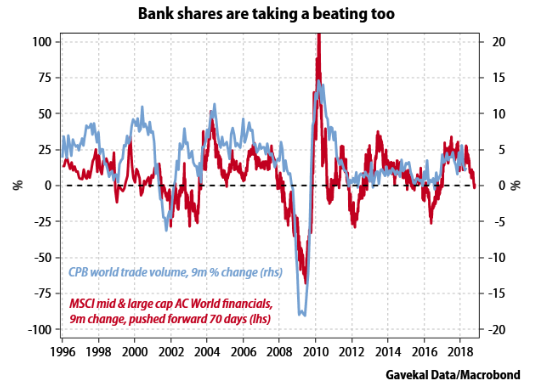

- “Needless to say, if these countries are having a hard time today because they have borrowed too freely in US dollars in the past, then it stands to reason that whoever lent them those dollars must be feeling the heat too. And sure enough, bank shares have cratered lately.” – bto: Und dabei haben sie sich noch nicht von der letzten Rezession erholt.

- “(…) the US dollar is going up, as it tends to do every time world trade slows down or contracts.” – bto: Und er tut es.

- “A world-wide recession is looking more and more probable. And if the time lag is similar to those in the past, it could hit by March 2019. Indeed, looking at the performance of markets over the last six months, it looks as if a bear market may have already started everywhere but in the US. As I have written repeatedly in recent months, bears are sneaky animals. Their victims seldom see them coming.” – bto: Dazu passen auch die Rotation in “sicherere” Bereiche und die beginnende Schwäche der FANGs.

Und dann ein paar korrekte Schlussfolgerungen:

- “The eurozone economies in general, and Italy and France in particular, are not in a position to navigate another recession.” – bto: darum auch der Ruf nach der Transferunion.

- “China has foreseen the danger of a US dollar shortage, and has tried to arrange things in Asia to allow the region to ride out a dollar squeeze. As a result, Asia is likely to be a zone of relative stability in the coming turmoil.” – bto: wobei China genug eigene Probleme hat.

- “For the first time in almost 20 years, cash is an alternative to risk assets. The yen is probably the cheapest currency there is today. Cash should be held in yen.” – bto: was natürlich eine riskante Spekulation ist.

- “Investors should hedge the equity risk in their portfolios with US long bonds and Chinese long bonds.” – bto: wobei die langen Bonds immer auch ein erhebliches Risiko darstellen.

- “Investors should avoid financials everywhere, as I have repeated until I am blue in the face.” – bto: was immer meine Meinung war.

- “Investors should sell the shares of companies with negative cash flow, especially if they are short US dollars.” – bto: Klar, denn diese können am ehesten Pleite machen.

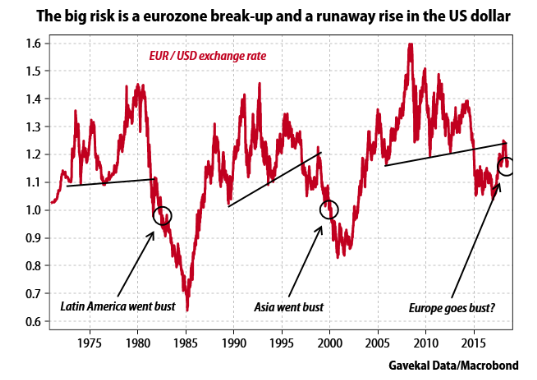

- “The big risk is an uncontrollable rise in the US dollar if Europe’s fixed exchange rate system falls apart, much as earlier US dollar liquidity crises led to the collapse of fixed exchange rate systems in Latin America and Asia. Buy calls on the US dollar against the euro.” – bto: Die Eurozone dürfte die nächste Krise nicht überstehen.

_________________________