“The Fed, QE, & Why Rates Are Going To Zero”

Es wird immer offensichtlicher, dass die schon vor Jahren aufgestellte These der Bank für Internationalen Zahlungsausgleich zutrifft: Die Zinsen müssen morgen noch tiefer sein, weil sie heute schon tief sind. Nur so gelingt es, dass immer höher verschuldete und deshalb langsamer wachsende System noch eine Runde weiter zu bekommen. Hier ein weiterer Blickwinkel auf das Thema:

Zunächst zitieren wir Federal Reserve Chairman Jerome Powell, der kürzlich äußerte: “In short, the proximity of interest rates to the ELB has become the preeminent monetary policy challenge of our time, tainting all manner of issues with ELB risk and imbuing many old challenges with greater significance. Perhaps it is time to retire the term ‘unconventional’ when referring to tools that were used in the crisis. We know that tools like these are likely to be needed in some form in future ELB spells, which we hope will be rare.” – bto: Klartext − da wir uns dauerhaft an der Nulllinie der Zinsen befinden, bleibt uns keine andere Wahl, als die Instrumente, die früher als ungewöhnlich galten, als normal anzusehen und deshalb offensiv einzusetzen.

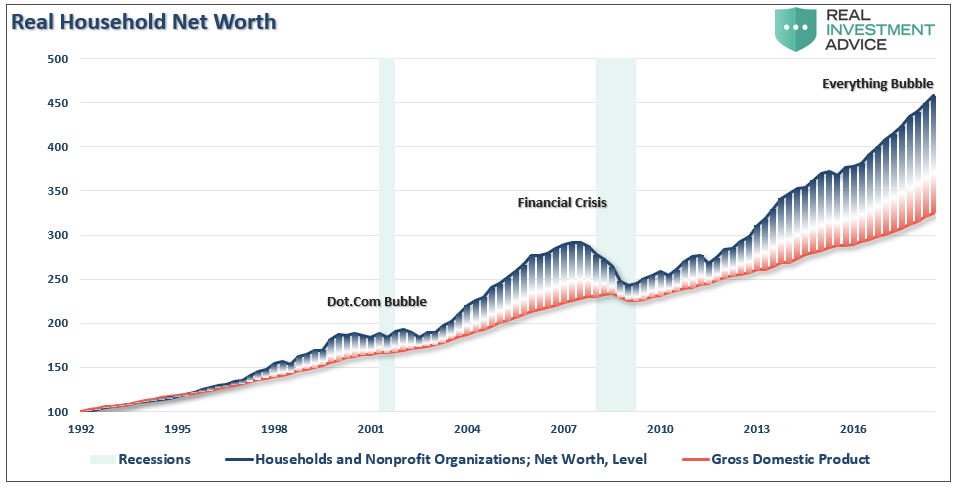

- “Clearly, QE worked well in lifting asset prices, but not so much for the economy. In other words, QE was ultimately a massive ‘wealth transfer’ from the middle class to the rich which has created one of the greatest wealth gaps in the history of the U.S., not to mention an asset bubble of historic proportions.” – bto: Das gilt abgeschwächt natürlich auch in Europa.

Quelle: Real Investment Advice

- Das Problem: “(…) no one knows for certain whether the bubbles created by monetary policies are infinitely sustainable? Or, what the consequences will be if they aren’t.” – bto: Ich denke, wir können uns ausmalen, was passiert, wenn die Effektivität bei null liegt. Dann setzt die Flucht ein. Entweder aus dem Geld oder aus den inflationierten Assets. Inflation oder deflationärer Kollaps sind die Optionen.

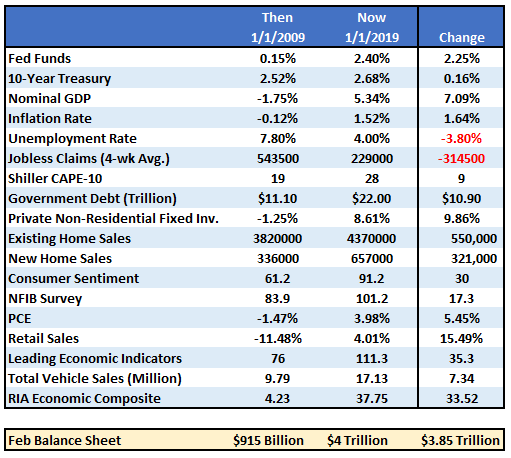

- “If the market fell into a recession tomorrow, the Fed would be starting with roughly a $4 Trillion balance sheet with interest rates 2% lower than they were in 2009. In other words, the ability of the Fed to ‘bail out’ the markets today, is much more limited than it was in 2008.” – bto: aber immer noch signifikant besser als die Optionen der EZB. Selbst in Japan liegen die Zinsen höher als in Deutschland, wenn es noch eines Beweises für die schlechte Lage in Europa bedurft hätte.

Diese Tabelle vergleicht einige wirtschaftliche Indikatoren 2009 und heute:

Quelle: Real Investment Advice

- “The critical point here is that QE and rate reductions have the MOST effect when the economy, markets, and investors have been ‘blown out,’ deviations from the ‘norm’ are negatively extended, confidence is hugely negative. In other words, there is nowhere to go but up.” – bto: So ist es. Am effektivsten sind die Maßnahmen, wenn sie auf technisch so extreme Märkte treffen, die nur einen Anstoß brauchen, um in die andere Richtung zu drehen.

- “(…) QE4 (…) will only be employed when rate reductions aren’t enough. Such was noted (…) a staff working paper entitled ‘Gauging The Ability Of The FOMC To Respond To Future Recessions.’ The conclusion was simply this: ‘Simulations of the FRB/US model of a severe recession suggest that large-scale asset purchases and forward guidance about the future path of the federal funds rate should be able to provide enough additional accommodation to fully compensate for a more limited [ability] to cut short-term interest rates in most, but probably not all, circumstances.’” – bto: natürlich nicht. Man braucht erst die echte Krise, also Chaos an den Märkten, bevor es etwas bringt. Man kann also nur effektiv löschen, wenn es richtig brennt.

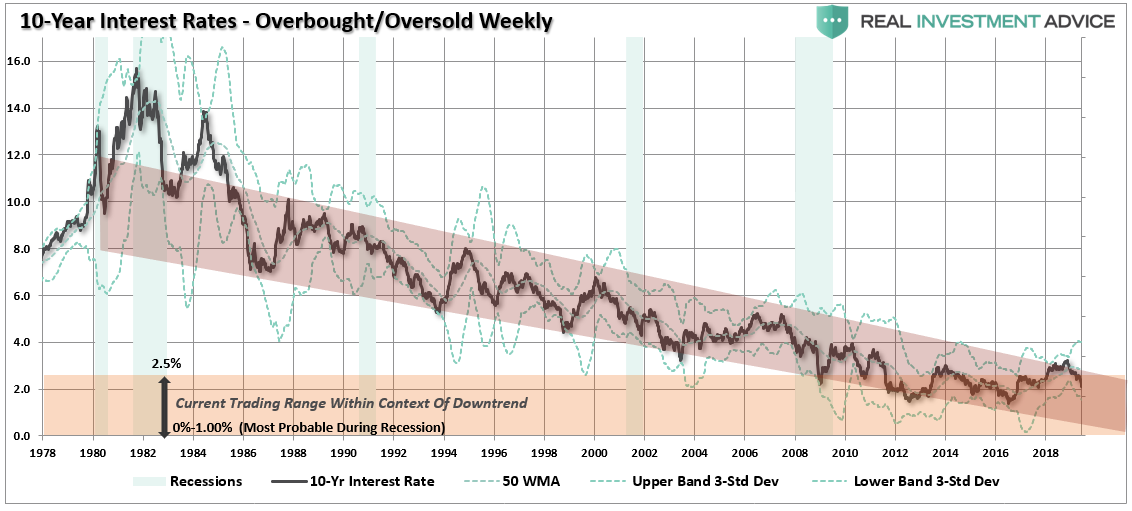

- “Even from a purely technical perspective, the trend of interest rates suggested at that time a rate below one-percent was likely during the next economic recession.” – bto: was das Bild eindeutig zeigt. Und was auch zu dem passt, was andere Beobachter wie Albert Edwards immer wieder beschreiben:

Quelle: Real Investment Advice

- “(…) recessionary environments are especially prone at suppressing rates further. But, given the inflation of multiple asset bubbles, a credit-driven event that impacts the corporate bond market will drive rates to zero.” – bto: zum Beispiel, wenn wir einen prominenten Absturz aus dem BBB-Rating sehen – GE? – und wir dann eine Flucht aus dem BBB-Segment erleben.

- “Furthermore, given rates are already negative in many parts of the world, which will likely be even more negative during a global recessionary environment, zero yields will still remain more attractive to foreign investors. This will be from both a potential capital appreciation perspective (expectations of negative rates in the U.S.) and the perceived safety and liquidity of the U.S. Treasury market.” – bto: also starker Dollar, Kursgewinne und bessere Bonität. Oder doch lieber Portugiesen oder Franzosen?

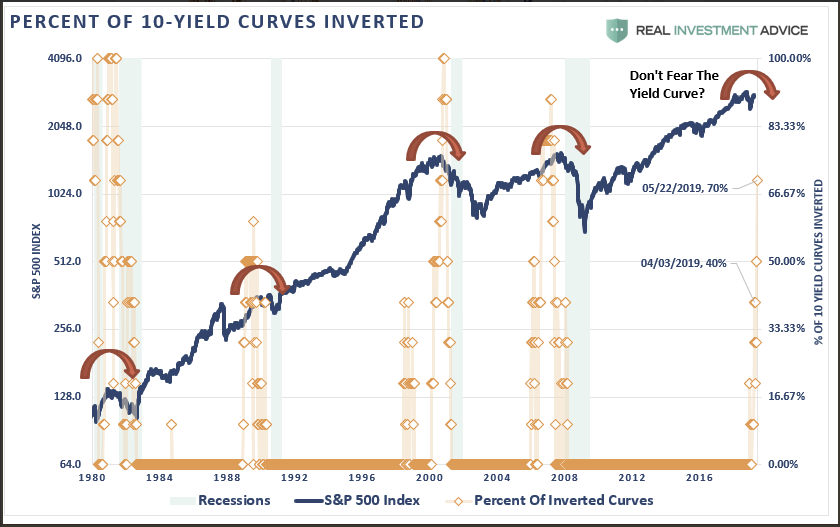

- “With the majority of yield curves that we track now inverted, many economic indicators flashing red, and financial markets dependent on “Fed action” rather than strong fundamentals, it is likely the bond market already knows a problem in brewing.” – bto: Davon kann man wohl ausgehen.

Quelle: Real Investment Advice

- “While another $2-4 Trillion in QE might indeed be successful in further inflating the third bubble in asset prices since the turn of the century, there is a finite ability to continue to pull forward future consumption to stimulate economic activity. In other words, there are only so many autos, houses, etc., which can be purchased within a given cycle.” – bto: was auch ein Grund dafür ist, dass neue Schulden immer weniger Wachstum bringen und zugleich die Spekulation eine immer größere Rolle spielt.

- “If I am correct, and the effectiveness of rate reductions and QE are diminished due to the reasons detailed herein, the subsequent destruction to the ‘wealth effect’ will be far larger than currently imagined. There is a limit to just how many bonds the Federal Reserve can buy and a deep recession will likely find the Fed powerless to offset much of the negative effects.” – bto: alles verstanden und auch einverstanden. Bleibt die Frage, wie geht man mit diesem realistischen Szenario um, vor allem wenn man in Europa sitzt, wo wir zusätzlich durch Euro und dysfunktionale Politik gehemmt sind?