“The Eurozone’s Long Depression”

Ein Leser hat mich auf einen interessanten Blogbeitrag hingewiesen, der sich mit der Struktur der Eurozonen-Wirtschaft beschäftigt. Dabei werden die Daten der EZB nüchtern betrachtet. So, wie es auch bei bto von mir immer wieder versucht wird, klar und nachvollziehbar. Deshalb heute hier zum ersten Mal als Quelle: Coppola Comment

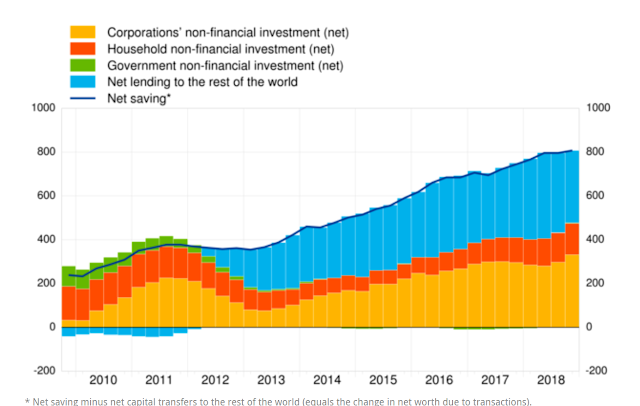

Zunächst zeigt der Beitrag die Entwicklung des Sparens in der Eurozone. Leser von bto kennen den Zusammenhang zwischen Ersparnisüberschüssen und Handelsüberschüssen, hier immer wieder mit Blick auf Deutschland diskutiert und kritisiert. Genau so sieht es nach Daten der EZB auch auf Eben der Eurozone seit 2011 aus:

Quelle: EZB

Beeindruckend ist zum einen der starke Anstieg, aber vor allem, was da gestiegen ist. Es ist der Forderungsaufbau an das Ausland außerhalb der Eurozone. Gleichzeitig haben die Staaten netto nichts mehr investiert! Unternehmen und private Haushalte investieren hingegen wieder auf normalem Niveau. Dazu Coppola:

- “The chart shows that collapsing corporate investment is the real story of the Eurozone crisis. European corporations all but stopped investing in the Eurozone in 2012-13. Even now, corporate investment in the Eurozone is barely higher than it was in 2011, in the wake of the Great Financial Crisis.But European corporations didn’t stop investing. They simply looked elsewhere. Net saving didn’t dip much in the Eurozone crisis – but the associated investment no longer went into the Eurozone economy. It flowed out of the Eurozone to the rest of the world. Ever since the crisis, as net saving has increased in the Eurozone, the rest of the world has benefited from its rising exports of capital.” – bto: Und das ist aus vielen Gründen rationales Verhalten: ungelöste Krise, schlechte Demografie, mehr Wachstum in anderen Regionen. Es ist das Symbol für den Niedergang Europas und die deutlich höhere relative Attraktivität anderer Regionen der Welt. So wie auch ich immer empfehle, sich woanders hin zu orientieren.

- “(…) the Eurozone authorities have very good reasons for pursuing policies that discourage external investment.(bto: gemeint ist hier von Ausländern in der Eurozone). The ‘sudden stop’ in 2011 nearly destroyed the Euro. Those in charge in the Eurozone daren’t risk another one. The current account surplus, and associated capital exports, are protective. After all, if you never borrow from the outside world, they can’t hurt you.” – bto: Das ist aber meines Erachtens nicht die Motivation. Die Politiker verstehen nicht, wie unattraktiv Europa fundamental als Investitionsstandort geworden ist.

- “In fact the Eurozone is behaving in much the same way as developing countries have since the Asian crisis of 1997, and for much the same reasons. Just as developing countries pursued export-led growth strategies and built up large FX reserves to protect themselves (…) Perhaps Eurozone leaders think the investment chill that is causing the Eurozone’s poor growth, high unemployment and stubbornly low inflation is a fair price to pay to keep the Eurozone together.” – bto: Das kann gut sein, finden sie doch auch Negativzinsen zunehmend normal.

- “But the Eurozone is not a young developing country whose population is generally living on a low income. It is a mature Western economy with a population that is used to a relatively high standard of living and whose net worth took an absolute beating not only in the 2007-8 financial crisis, but also in the Eurozone crisis.” – bto: Was klar ist, denn Deleveraging geht immer mit verfallenden Assetpreisen einher. Soweit also zu erwarten.

Quelle: EZB

Fazit Coppola: “Rising property prices seem to be the only means the people of the Eurozone have of restoring their lost wealth. But for the young, already suffering from high unemployment, rising house prices mean an even more impoverished future. For how much longer will they tolerate this Long Depression?” – bto: Das führt zu meiner immer wieder gemachten Feststellung: Es ist eine Frage des politischen Durchhaltevermögens, wie lange die Eurozone überlebt. Dieses ist allerdings endlich.

→ coppolacomment.com: “The Eurozone’s Long Depression”, 30. April 2019