Stimmt: Frankreich ist das größte Risiko für Euro und unsere Ersparnisse

Heute Morgen habe ich gezeigt, wie falsch die Haltung der EU zu Italien ist – was nichts daran ändert, dass wir uns damit abfinden müssen, dass der Euro nicht funktionieren kann und in großem Knall mit erheblichen Verlusten für uns enden wird.

Auch klar ist, dass das Problem Italien von dem noch größeren Problem Frankreich übertroffen wird. Beide Länder versuchen, den Kollaps so lange wie möglich aufzuschieben. Das geht nur, indem man

a) an die deutsche Verschuldungskapazität kommt – deshalb Eurozonen-Budget, -parlament und letztlich auch -finanzminister.

b) die EZB zur unbegrenzten Finanzierung und letztlich Monetarisierung nutzt.

Beides ist “im Plan”, würde ich sagen. Da b) ohnehin kommt, könnten wir doch auf a) verzichten. Doch irgendwie macht es wohl nur so richtig Spaß.

Einen Blick auf Frankreich wirft Ambroise Evans-Pritchard im Telegraph. Es ist wie immer eine konzise Beschreibung der Lage:

- “(Macron) had pledged root-and-branch reform of the French economy and a restoration of spending discipline after 11 years in breach of the EU’s Stability Pact. The calculation was that Berlin would in return drop its long-standing opposition to fiscal union and shared liabilities, agreeing to rebuild the euro on stronger foundations.” – bto: obwohl die Studien zeigen, dass die Umverteilung gar nicht groß genug sein kann.

- “To the extent that this bargain was ever more than wishful thinking, it is dead now. The German Kanzleramt and finance ministry have watched near insurrection sweep the major cities of France over the last four weeks – with ‘Act V’ already announced for next weekend – and watched a belated riposte from Élysée Palace that amounts to a climbdown.” – bto: falsch. Die deutsche Öffentlichkeit will jetzt erst recht “mehr Europa”. Wir müssen immer in der Rolle des Retters der Welt sein, um unsere Geschichte zu kompensieren.

- Sodann zitiert er Clemens Fuest: “Macron’s response suggests that a rioting and pillaging mob can dictate politics, while those who demonstrate peacefully – or not at all – are ignored. His whole ability to push has been called into question. What he has announced are just tax giveaways. France should face the normal (disciplinary) procedure from the Commission. It would be quite wrong if Italy is subjected to all this criticism while the French do what they want.” – bto: Da wird jedem klar, warum der Euro scheitern muss. Man kann ihn nicht mit Umverteilung retten, man sollte ihn auch nicht mit Umverteilung retten. Man kann ihn aber auch mit Sparpolitik nicht retten. Nicht dann, wenn man den Staat so abgewirtschaftet hat, wie wir es in Westeuropa alle getan haben (außer die Schweizer). Zu viele Transferempfänger, zu hohe Lasten und zu hohe Schulden. Game over. Dann Austerität zu fordern, macht massiv unbeliebt.

- “‘It is quite obvious that the budget deficit will be at least 3.5pc of GDP next year, and probably 4pc because the economy is heading for a light recession,’ said Professor Jacques Sapir from the École des Hautes Études en Sciences Sociales in Paris. ‘Macron is now in the same boat as Salvini and di Maio in Italy. This is very embarrassing because he castigated them as populists over their budget.’” – bto: Ach, die Franzosen sind doch etwas Besonderes. Kürzlich habe ich einen führenden deutschen Ökonomen mit gutem Kontakt zum Kanzleramt gehört, wie er meinte, dass die Franzosen doch einmal in 2019 das Drei-Prozentziel “leicht” verfehlen dürften. Hmm. Was ist mit den letzten elf Malen?

- “Risk spreads on French 10-year debt jumped to 48 basis points on Tuesday as bond vigilantes began to digest the scale of fiscal slippage. This is the highest level since the ‘Frexit’ scare before the French elections in early 2017, when the Front National’s Marine Le Pen was riding high in the polls.” – bto: Und Frexit wird wieder auf die Agenda kommen beim nächsten Mal.

Quelle: FT

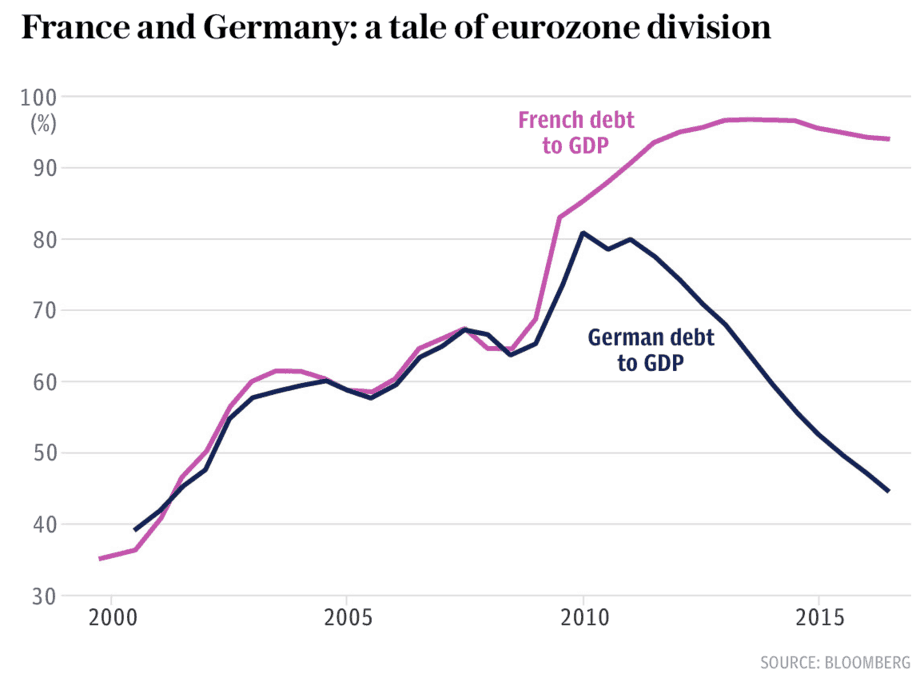

- “The French economy is already close to stall speed. The Banque de France has cut its forecast for growth in the fourth quarter to 0.2pc. The PMI surveys for manufacturing are near contraction levels. This slowdown is already eroding debt dynamics. (…) The cancellation of the fuel tax rise and latest sweeteners will together cost €14bn. France’s debt-to-GDP will likely rise beyond 100pc as a result” – bto: klar. Aber es ist ohnehin illusorisch, sich aus den Schulden durch Wachstum zu befreien. Der Point of no Return liegt hinter uns.

- “Professor Brigitte Granville, a French economist at Queen Mary University of London, said the European Commission is in a serious bind. Any demand for harsh budget cuts in France in this volatile political mood could spin out of control. ‘If they make the French too angry, it’s the end of the euro,’ she said. ‘The biggest danger for monetary union is not Greece, or Italy, it is France.’” – bto: Das ist doch mal super. Wenn die Franzosen zu sehr verärgert sind, endet der Euro. Na dann sollten wir unsere Portemonnaies rasch öffnen …

Und in diese Richtung gehen die Kommentare der EU-Kommission, angeführt vom französischen (!) Kommissar für Wirtschaft Pierre Moscovici, den der Telegraph in einem anderen Beitrag so zitiert: “There is no question of privileged treatment for some and exaggerated toughness for others.” – bto: nein, natürlich nicht. Frankreich ist ja nunmal was Besonderes. Der Telegraph zitiert weiter: “The spending measures from President Macron were acceptable as they were being made amid increased risk of ‘social disintergration, Mr Mosovici suggested. Mr Moscovici also noted that while France might be set for a one-off breach of the 3pc rule, Italy’s spending plans would break the rules for three years in a row. The rules were ‘subtle and complex’, he added.” – bto: So erzählt man Geschichten! “One-off-Breach”?? Elf Jahre in Folge, die dann so aussehen:

Quelle: The Telegraph

- Weshalb es auch kritische Stimmen gibt: “(…) some economists believe that the French fiscal situation is not being treated with sufficient gravity compared to its peers by both the market and the Commission.Angel Talavera of Oxford Economics said: ‘If you look at the sovereign ratings for France, currently it’s about five notches above Spain. I think the fiscal numbers from France do not justify this. You could make a case that France’s deficit has been one of the highest in the eurozone for years. If you look at [its] debt, it is rising. France has had quite a lack of fiscal discipline for several years. I think ratings [on credit, gilt yields,] seem to be more lenient on France than other countries.’” – bto: weil der Markt (wohl zu Recht) davon ausgeht, dass wir das schon bezahlen, siehe oben.

- “Defenders of Mr Macron insist that there is no valid comparison with political events in Italy. He is determined to press ahead with reforms to liberalize the economy, reduce the incentive for early retirement, and free up the labour markets. (…) By contrast, the Lega-Five Star coalition is rolling back pension reforms already in place. The Italian economy has deeper structural problems and lower trend growth, and is therefore less able to whittle down its high debt levels. The EU fiscal police weigh all these different factors in making their judgment.” – bto: Nun ja, aber die Italiener haben in den letzten Jahren wirklich gespart, das sollte etwas Goodwill geben.

- “(…) it is becoming harder to argue that Mr Macron’s reforms amount to deep transformation, let alone a genuine shake-up of a bloated French state that gobbles up 55pc of GDP. His labour reform has merely chipped away at the antique ‘code de travail’, a door-stopper of 3,000 pages. He has decentralized wage bargaining, making it easier for firms to deal directly with their own workers rather than having to negotiate with unions – often militant – that make up just 7.7pc of the workforce.” – bto: so viel zum Thema “Reformen”.

- “(…) the ‘gilets jaunes’ – supported by 80pc of the French people – show the limits of his election mandate in 2017. He won as the ‘anti-Le Pen’ candidate, not because the country endorsed his neo-liberal europhile policies.” – bto: So ist es. Die EU muss sich ändern, um zu überleben.