Notenbanken als Hauptgläubiger der Staaten: Bereiten wir den Neustart vor?

Bekanntlich wird seit Jahren über die Möglichkeit diskutiert, die Staatsschulden auf einem sehr eleganten Weg aus der Welt zu schaffen: Die Notenbank kauft einfach alles auf und annulliert danach die Schulden. Vor Jahren noch undenkbar, dürfte es spätestens mit dem nächsten Aufflammen der Krise – die bekanntlich nicht vorbei ist – so weit sein.

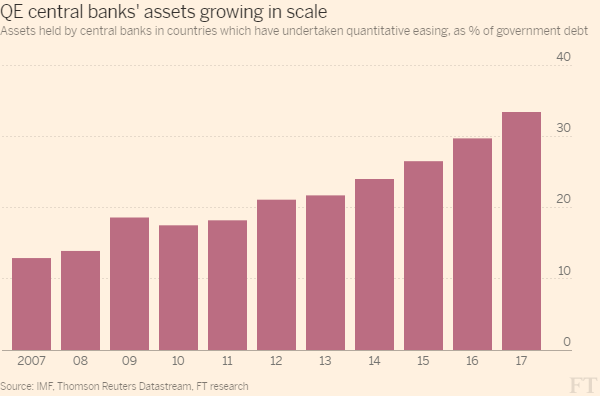

Wie weit die Notenbanken schon gekommen sind, hat die FT ausgerechnet. Zunächst das entscheidende Bild:

Quelle: FINANCIAL TIMES

Und dann noch ein paar nette Kommentare dazu:

- “In total, the six central banks that have embarked on quantitative easing over the past decade – the US Federal Reserve, the European Central Bank, the Bank of Japan and the Bank of England, along with the Swiss and Swedish central banks – now hold more than $15tn of assets..” – bto: 15.000 Milliarden US-Dollar. Nicht schlecht und ein wichtiger Schritt Richtung “Lösung” der Schuldenkrise.

- “(…) more than $9tn is government bonds – one dollar in every five of the $46tn total outstanding debt owed by their governments.” – bto: Damit wird es ein zunehmend realistisches Szenario, allerdings zunächst in Japan.

- “(…) the current era is the first time in history that such a large group of central banks have undertaken such a substantial volume of co-ordinated buying over the space of nearly a decade. (…) What was originally intended as a temporary emergency measure has now evolved into a significant challenge for policymakers as they contemplate how to return the global economy to normal monetary conditions.” – bto: Ich glaube nicht, dass sie daran ernsthaft denken. Sie überlegen, wie sie uns entschulden können!

- “Central banks’ bond-buying has helped push sovereign yields to record lows and in some cases into negative territory, with bondholders paying governments to own their paper.” – bto: Braucht es da noch weitere Informationen? Die japanische Notenbank hält übrigens schon mehr als 40 Prozent aller Staatsanleihen.

Das wird natürlich dann zu einem Problem, wenn die Notenbank, im konkreten Fall die EZB, nicht mehr genug Anleihen kaufen darf. Hier stößt man nämlich an die selbst gesetzte Grenze von maximal einem Drittel der Staatsschulden des jeweiligen Mitgliedslandes und – dummerweise – macht ausgerechnet Deutschland keine weiteren Schulden mehr. Auch hierzu die FT:

- “Mr Draghi faces a dilemma of his own: the central bank is running out of bonds to buy. Its own rules restrict it to only purchasing a third of each country’s debt in circulation, and the supply of German Bunds and Portuguese debt in particular is starting to run thin.” – bto: Ich wette, diese Grenze wird in Zukunft fallen, sobald eine Notsituation kommt. Und dies ist nur eine Frage der Zeit!

- “(…) the ECB could hit its 33 per cent purchase ceiling for German debt as early as February. That would effectively force the central bank to selectively taper its bond-buying programme by continuing to purchase the debt of peripheral countries while quitting Germany’s debt markets. (…) The asset purchase programme would become completely skewed towards purchases in France and Italy.” – bto: Die wird es auch mehr brauchen. Doch irgendwann ist auch hier Schluss. Was dann?

So sieht es übrigens zurzeit aus:

Quelle: FINANCIAL TIMES

Heißt im Klartext: Noch sind wir nicht so weit, dass es sich lohnt, die Schulden zu annullieren. Gerade Frankreich und Italien (und bei ehrlicher Rechnung auch wir!) brauchen einen größeren Schnitt. Der wird aber in den kommenden Jahren vorbereitet werden.