Nächster Schritt in die Eiszeit: der Währungskrieg

In einer Welt mit Überkapazitäten, Überschuldung, ungedeckten Verbindlichkeiten für eine alternde Gesellschaft und unzureichendem Wachstum, um die Lasten tragbar zu machen, ist es nur eine Frage der Zeit bis gilt: Jeder kämpft für sich alleine. Dazu gehören Protektionismus und Abwertung der eigenen Währung. Haben die USA – und alle anderen, wenn auch weniger laut – dieses Instrument schon in den letzten Jahren genutzt, stehen wir nun vor einer Neuauflage der massiveren Art, denkt Albert Edwards und bto schließt sich an:

- “SocGen’s Albert Edwards (…) brings attention to the barrage of recent tweets from President Trump indicating that ‘his tolerance for the strong dollar has just about run out’ (…) as the global economy falls ever closer towards outright deflation, Edwards predicts that ‘the global currency war will explode into life. Countries will fight to avoid deflation in the next recession and competitive devaluation will be the tool of choice.’” – bto: Wir wissen aus der Großen Depression, dass jene, die abgewertet haben wie Japan, besser gefahren sind. Wer weiß, wie Deutschland heute aussähe, wenn Brüning diesen Weg auch hätte gehen können?

- “Indeed this was the solution Ben Bernanke suggested in his famous 2002 speech about how to avoid ending up like Japan, to wit: (…) it’s worth noting that there have been times when exchange rate policy has been an effective weapon against deflation. A striking example from US history is Franklin Roosevelt’s 40% devaluation of the dollar against gold in 1933-34, enforced by a program of gold purchases and domestic money creation. The devaluation and the rapid increase in money supply it permitted ended the U.S. deflation remarkably quickly.” – bto: Das leuchtet auch ein. Es ist massive Monetarisierung und damit Entwertung von echtem Geld.

- “Edwards (…) writes, ‘it would not have missed President Trumps attention that while the US recorded an overall $625bn trade deficit in 2018, the eurozone ran a huge $600bn surplus (over 4% of GDP). By contrast China and Japan ran surpluses of only $100bn and a $10bn respectively.’ In other words, ‘when it comes to global trade imbalances China and Japan are not the problem’.” – bto: Richtig, und auch wer das Problem darstellt, ist für Leser von bto keine Überraschung. Es ist Deutschland, was am meisten vom schwachen Euro profitiert:

Quelle: SocGen, Zero Hedge

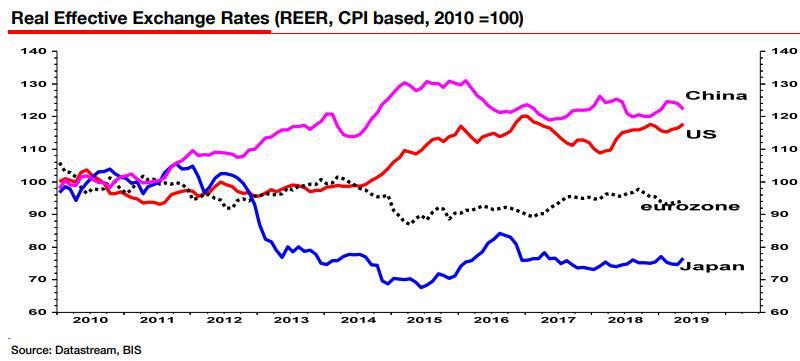

- “Edwards explains further, ‘there is no doubt that the dollar is overvalued, not just against the euro but against a basket of currencies. But so too is the Chinese renminbi (although the gap versus the US has narrowed as the Chinese have allowed the bilateral rate to slide towards $7.0/Rmb). But if you really want to see a major currency that is cheap, it is the yen and not the euro that stands out as anomalously undervalued (see chart below).’” – bto: Aber der Euro hat weniger Munition, um sich gegen den Dollar zu verteidigen, weil die Schwäche schon jetzt von der EZB organisiert ist. Normalerweise werten Währungen von Überschussländern auf. Siehe Schweiz.

Quelle: SocGen, Zero Hedge

- “When we talk about the burgeoning eurozone external surplus, we all really know that is shorthand for Germany (…)Germany’s overall current account surplus dominates the eurozone surplus and has been topping a massive 8% of its own GDP recently (although projected by the OECD to decline to 7.3% GDP this year).” – bto: Und wir legen die Überschüsse auch noch schlecht an. Was für ein Wahnsinn!

- “Germany now runs the biggest single dollar trade and current account surplus in the world. (…) until the eurozone crisis of 2011 (…) the eurozone periphery was the mirror image of Germanys huge current account surplus (see chart below). (…) The periphery acted as a sponge, soaking up German excess saving – and the overall eurozone, by and large, remained broadly in external balance with the rest of the world. Germany’s huge surplus was nobodys concern but the eurozone’s.” – bto: Das war, als wir große Forderungen gegen die heutigen Krisenländer aufgebaut haben und nun nicht fällig stellen können, sondern stattdessen mit TARGET2 umschulden zu Nullzins und ohne Tilgung.

- “(…) the problem for the rest of the world now is that under stringent post-eurozone crisis austerity, the eurozone periphery sponge has been totally squeezed out and the rest of the world is being now forced to soak up excess German saving (ie the mirror image of the current account surplus).” – bto: genau. Heute exportieren wir mehr in die Welt außerhalb der Eurozone, was zu weiteren Problemen führt. Das Chart ist schon beeindruckend:

Quelle: SocGen, Zero Hedge

- “(…) according to Edwards, the problem going forward is ‘it won’t just be Japan and the eurozone that will be trying to devalue their way far from the deflation quagmire, but also the US.’ Specifically, US authorities under the lead of President Trump will embrace Ben Bernanke’s 2002 advice of a competitive devaluation similar to that seen in 1933/4 like a long-lost friend.” – bto: Und ich denke, habe ich schon früher geschrieben, dass die EZB in diesem Spiel nicht richtig mitmachen kann.

- “A US recession and outright deflation could be closer than many suppose. The recent slide in US ISM manufacturing new orders relative to inventories warns us of a sharp and imminent GDP slowdown as does the recent weakness in Gross Domestic Income. The NY Fed Nowcast stands at only 1.5% for Q2 and 1.7% for Q3. The US economy is at stall speed and may even already be sliding into recession and outright deflation.” – bto: Und wir alle wissen, dass Deflation für die überschuldete Welt “game over” bedeutet.

- “the US will soon be forced by events to join the eurozone and Japan in aggressively fighting deflation. I expect that in addition to President Trump using auto tariffs as a weapon in the intensifying currency war against the eurozone (Germany), he will instruct the US Treasury (via the NY Fed) to intervene directly and unilaterally to drive the dollar lower – much lower.” – bto: Ich sehe auch die sehr hohe Wahrscheinlichkeit eines Angriffes auf die deutsche Automobilindustrie, die gerade besonders anfällig ist. Das beendet das Märchen vom reichen Land und stürzt Deutschland und die EU in die Krise.

- “Edwards writes that he is surprised the US ‘has not done so already, but any additional ECB easing will surely be the straw that will break the camels back. (…) With both the ECB and BoJ key policy rates already negative, it would be madness for the US Administration not to fight the global currency war on this battlefield in addition to all the others.’” – bto: Damit haben wir den Wettlauf nach unten.

- “Edwards reminds Japan watchers that the catalyst that tipped the country into outright deflation in the 1990s was a persistently strong yen, and he goes on to point out that ‘President Trump is not about to make that same mistake. Personally, I am surprised he has put up with the ECB winning the competitive devaluation game for so long. Expect the dollar to fall – bigly.’” – bto: und den Euro am Ende zu zerbrechen, würde ich ergänzen. Denn das überlebt die Eurozone nicht.