“Market Excesses ‘Approaching A Threatening Level’: IMF Issues Stark Warning On Leveraged Loans”

Immer wieder schön, wenn die offiziellen Institutionen warnen. Ich denke dann immer, ob sie das tun, um hinterher sagen zu können, „wir haben gewarnt“ oder ob es doch von den Politikern gehört wird. Bei uns in Deutschland sind Zweifel angebracht. Aber nicht nur hier.

So warnt der IWF erneut vor den Risiken im Markt für Unternehmenskredite. Leveraged Loans sind Lesern von bto schon aus früheren Beiträgen bekannt. Schlecht- oder unbesicherte Kredite an Unternehmen mit sportlicher Verschuldung oft im Zusammenhang mit Übernahmen durch Private Equity Unternehmen. Diese Kredite sind nicht nur explodiert, sondern werden auch von immer mehr Investoren gegeben, die die Risiken nicht richtig einschätzen und vermutlich auch nicht tragen können. Darin liegt die Gefahr im Falle eines Abschwungs. Panik kann schnell zu Verwerfungen im gesamten Finanzsystem führen. Forbes berichtet:

- „An unusually blunt warning about the massive market in leveraged loans from a normally-circumspect International Monetary Fund should give investors pause at a time of rising concern about global financial stability.” – bto: was wie gesagt nur zeigt, dass sie auch aufpassen.

- “Fund economists Tobias Adrian, Fabio Natalucci and Thomas Piontek have published a new blogpost highlighting some fairly alarming trends. “We warned in the most recent Global Financial Stability Report that speculative excesses in some financial markets may be approaching a threatening level. For evidence, look no further than the $1.3 trillion global market for so-called leverage loans, which has some analysts and academics sounding the alarm on a dangerous deterioration in lending standards. They have a point.” – bto: Und was ist die Ursache? Die Geldpolitik der Notenbanken, die viel Liquidität auf die Suche nach Ertrag schicken.

- “This growing segment of the financial world involves loans, usually arranged by a syndicate of banks, to companies that are heavily indebted or have weak credit ratings. These loans are called ‘leveraged’ because the ratio of the borrower’s debt to assets or earnings significantly exceeds industry norms.” – bto: Und wir wissen, dass auch bei den sogenannten Investment-Grade-Anleihen einige Probleme lauern …

Quelle: Forbes, IMF

Quelle: Forbes, IMF

- “‚With interest rates extremely low for years and with ample money flowing though the financial system, yield-hungry investors are tolerating ever-higher levels of riskand betting on financial instruments that, in less speculative times, they might sensibly shun,‘ Adrian and his colleagues write.” – bto: Immer mehr Investoren kennen auch nur das heutige Umfeld der ewig tiefen Zinsen und des langfristigen Aufschwungs.

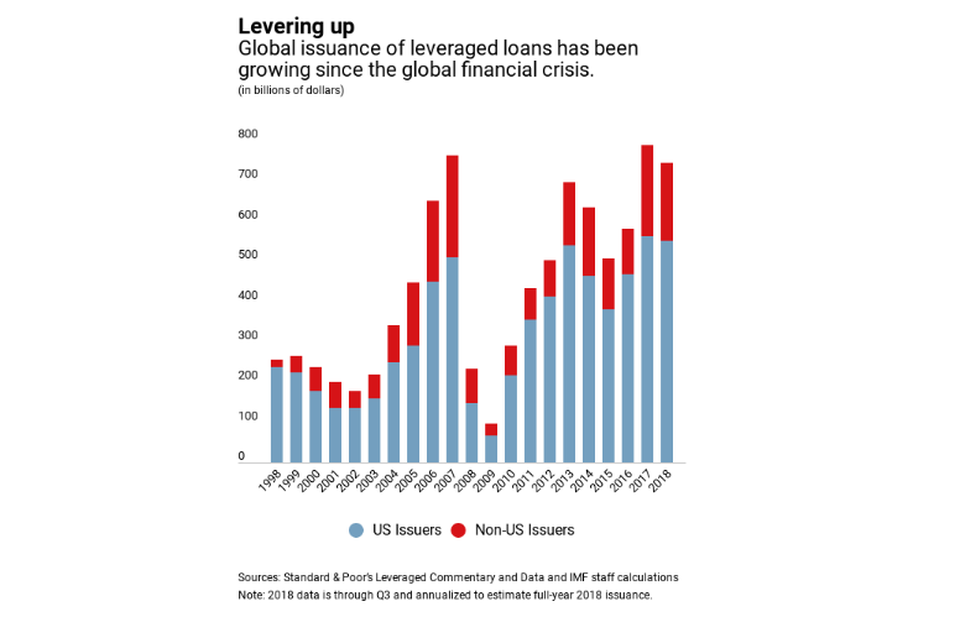

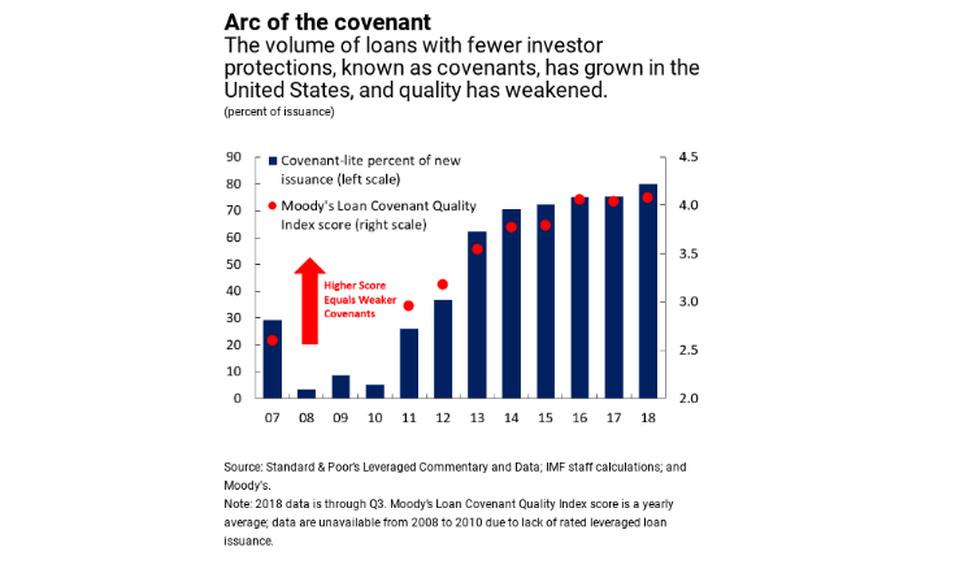

- “‚Speculative-grade companies have been eager to load up on cheap debt. Globally, new issuance of leveraged loans hit a record $788 billion in 2017, surpassing the pre-crisis high of $762 billion in 2007. The United States was by far the largest market last year, accounting for $564 billion of new loans.‘ It’s not just the market’s size and scope but also its increasingly loose underwriting standards, reminiscent of the mortgage market before the 2008 crash.” – bto: Klar, weshalb sich die Mühe machen, die Risiken zu analysieren, wenn im Zweifel die Notenbanken einen retten?

Quelle: Forbes, IWF

Quelle: Forbes, IWF

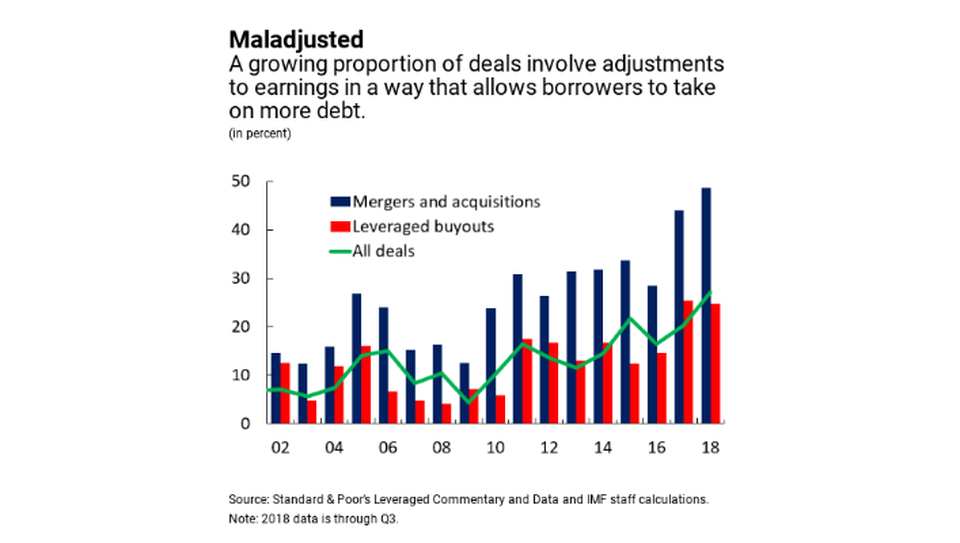

- “Some leveraged loan deals help borrowers mask their true exposures.” – bto: was dieses Chart zeigt. Da werden die Gewinne auch noch geschönt, was heißt, dass die Qualität noch deutlich schlechter ist.

Quelle: Forbes, IWF

Quelle: Forbes, IWF

- “A significant shift in the investor base is another reason for worry. Institutions now hold about $1.1 trillion of leveraged loans in the United States, almost double the pre-crisis level. That compares with $1.2 trillion in high yield, or junk bonds, outstanding. Such institutions include loan mutual funds, insurance companies, pension funds, and collateralized loan obligations (CLOs), which package loans and then resell them to still other investors. CLOs buy more than half of overall leveraged loan issuance in the United States.” – bto: Da haben wir wieder die Verteilung des Risikos, was in Wahrheit ein Verstecken ist!

Quelle: Forbes, IMF

Quelle: Forbes, IMF

- “The sobering conclusion: ‚Having learned a painful lesson a decade ago about unforeseen threats to the financial system, policymakers should not overlook another potential threat.‘ It sounds nice in theory. However, Federal Reserve officials have few tools — and have sought any new ones — does grapple with potential risks in the so-called shadow-banking system, which operates outside the part of the financial system it regulates. This gap may yet prove the gateway to the next financial crisis.” – bto: Natürlich haben sie eine Möglichkeit, zu handeln. Die Rückkehr zu einer soliden Geldpolitik mit deutlich höheren Zinsen. O. k., man darf ja mal träumen.