Jetzt kommen die Goldenen Zwanziger 2.0

Der Charttechniker der F.A.Z. sah in seiner Kolumne in der vergangenen Woche den DAX vor einem möglicherweise historischen Ausbruch nach oben als Auftakt für einen mehrjährigen Bullenmarkt. Vorstellen mag man sich dies angesichts der demografischen Entwicklung nicht so recht und schon gar nicht angesichts der ungelösten Probleme von Schulden, schlechter Produktivitätsentwicklung und dysfunktionaler EU und Eurozone.

Die Optimisten sagen, dass das die Folge des neuen Wirtschaftswunders sei, getrieben vom Umbau zur Rettung des Klimas. Pessimisten sagen, es sei einfach die Folge anhaltenden Schuldenmachens und gleich finanziert durch die Zentralbanken. Dann muss alles steigen, was stabile Cashflows hat.

Aber was soll es? Ich muss darüber nicht philosophieren. Habe ich doch bei Zero Hedge gelesen, dass Goldman Sachs schon für 2022 neue Höchststände für die Börsen erwartet. Und wer jetzt sagt, mein Titel wäre zu reißerisch, hier der offizielle Titel der Studie von Goldman:

Quelle: Zero Hedge

Das ist schon cool: die “wiederauferstandenen 20er-Jahre” und das, nachdem wir uns seit mehr als dreißig Jahren in einem Börsenaufschwung befinden. Warum das zu dem gleichen Ergebnis wie 100 Jahre zuvor führen soll?

- “We lift our S&P 500 EPS growth estimates to $136 in 2020 (-17%), $175 in 2021 (+29%), $195 in 2022 (+12%), $207 in 2023 (+6%), and $218 in 2024 (+5%). Our revised growth estimates are roughly in line with our previous estimates, but the level of 2024 EPS is $4 or 2% higher to reflect the increased starting point of 2020 profits. Our increased estimates primarily reflect much better-than-expected results in 3Q. S&P 500 EPS in 3Q 2020 was expected to fall by 21% but realized growth of just -8% (+$5 swing).” – bto: Es ist also zunächst Erleichterung, dass es nicht so schlimm gekommen ist wie befürchtet. Für die Goldenen Zwanziger langt das noch nicht.

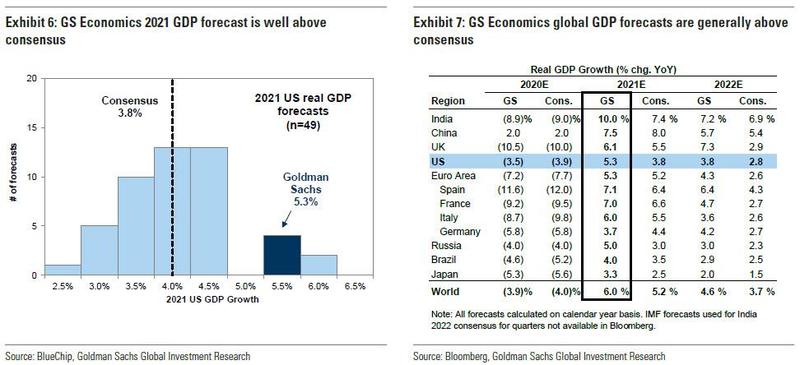

- “Goldman Sachs Economics US GDP growth forecasts reflect a continued “V-shaped” recovery and are well above-consensus at +5.3% in 2021 (consensus +3.8%) and +3.8% in 2022 (consensus +2.8%), followed by growth of +2.4% in 2023. In part due to this optimistic forecast for an economic rebound from the pandemic-induced recession, our 2021 earnings forecast is also above consensus.” – bto: nicht zuletzt wegen der Konjunkturprogramme und der Geldpolitik.

- “Outside of economic activity, a weakening USD and slack in the labor market should support S&P 500 sales and margins, respectively. The US unemployment rate registered 6.9% in October, well above the estimated natural rate of unemployment (4.4%). Our top-down model demonstrates that a loose labor market is typically positive for earnings growth, as wage growth exerts limited pressure on margin growth. Our FX strategists expect the trade-weighted US Dollar is in a structural downtrend, which typically acts as a tailwind to S&P 500 revenues, particularly for international-facing sectors. Their FX estimates assume the USD weakens by 5% vs. the Yen (to 100) and by 6% vs. the Euro (to 1.25).” – bto: Die Margen setzen voraus, dass man Nachfrage auch bei stagnierenden Gehältern aufrecht erhält und der schwache Dollar mag ja nett sein für die USA – nur ist er nicht erfreulich für die Exportländer.

- Aber generell wird ein besseres Wachstum erwartet. Auch für Europa, vor allem 2022.

Quelle: Goldman via Zero Hedge

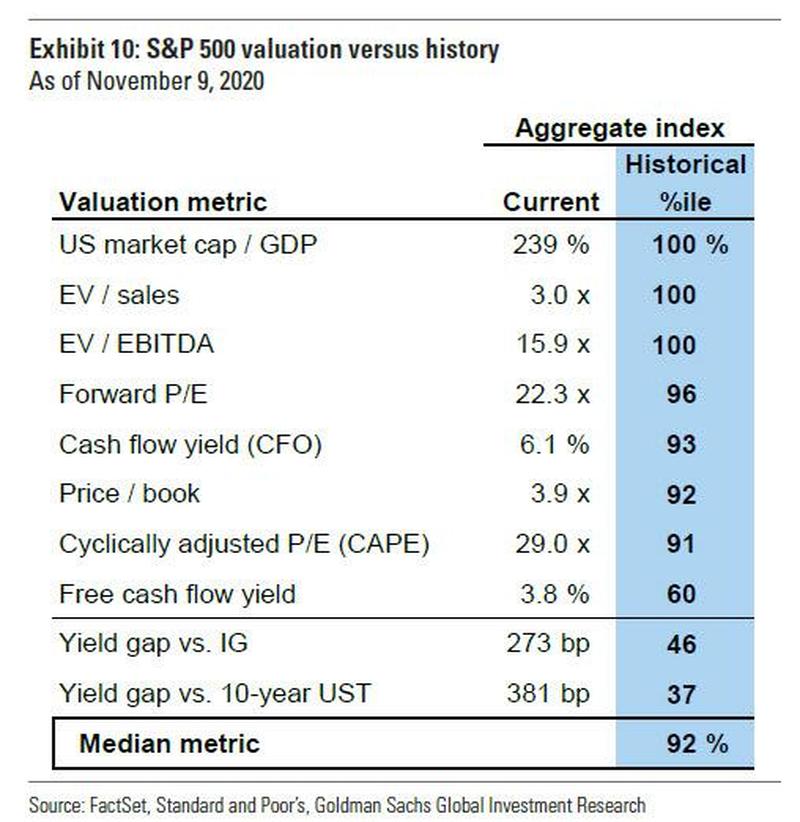

- Dabei weiß Goldman Sachs durchaus, dass die Aktien nicht billig sind. Nur im Vergleich zu den noch teureren Anleihen – sichtbar am “Yield-Gap” – sind Aktien noch relativ günstig …

Quelle: Goldman via Zero Hedge

Und wieso soll es noch weiter nach oben gehen? Genau: billiges Geld.

- “The backdrop of low interest rates and subdued policy uncertainty that we anticipate during the next two years will be constructive for equity valuations. (…) Interest rates: We assume stable Fed policy and limited yield curve steepening. Given the Fed’s new average inflation targeting (AIT) framework and its forward guidance for the funds rate, Goldman Sachs Economics forecasts the first hike in the funds rate will not occur until 2025. We assume higher breakeven inflation will drive modest yield curve steepening as the ten-year US Treasury yield climbs from 95 bp today to 1.3% at year-end 2021 and 1.7% by the end of 2022. Diminished prospects of massive fiscal spending that might have occurred under a Democratic sweep coupled with extremely low bond yields globally will limit the rise in nominal US yields.” – bto: ein Traum. Geld bleibt so lange billig, dass alles nur teurer wird.

- “Equity risk premium: Improving growth expectations and falling uncertainty will compress the ERP. Our economists’ baseline forecast for fiscal stimulus and vaccine approval should drive an improvement in growth expectations, breakeven inflation, and consumer confidence, in turn pushing the ERP lower.” – bto: Zu den tiefen Zinsen kommen also auch noch geringe Risikozuschläge für Aktien.

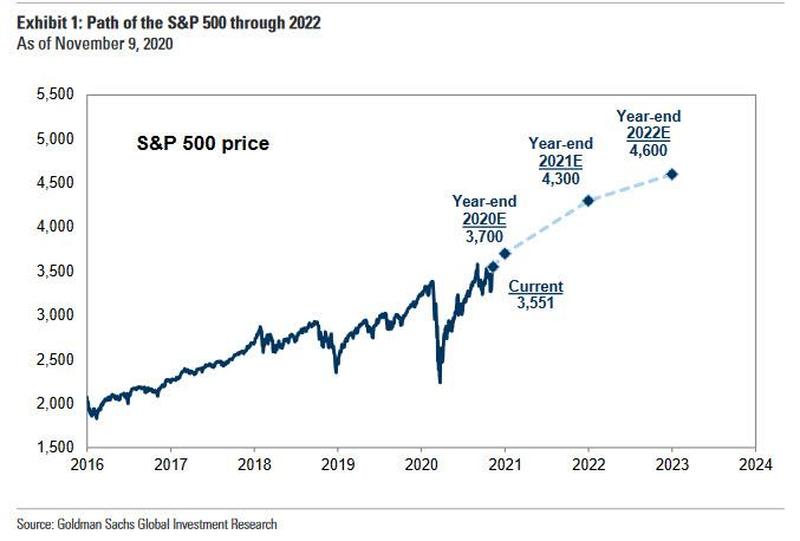

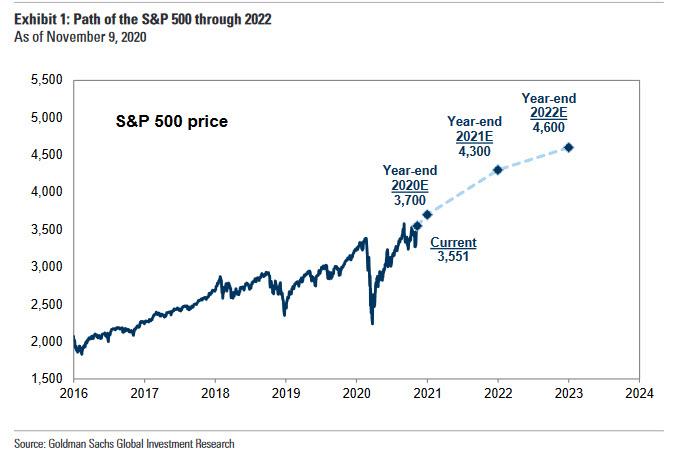

- “Under these conditions – and really Goldman will immediately flip its view as soon as the S&P tumbles because both JPM and Goldman have demonstrated that it is always and only price that sets the market narrative – Goldman forecast S&P 500 will rise by an additional 11% to reach 4100 by mid-year and end 2021 at 4300 (+5%; for a full-year return of 16% next year) and climb by 7% to reach 4600 by year-end 2022.” – bto: Und das ist ja erst der Anfang. Danach kommt die intelligente Lösung der Schuldenprobleme, das Wirtschaftswunder …

Quelle: Goldman via Zero Hedge

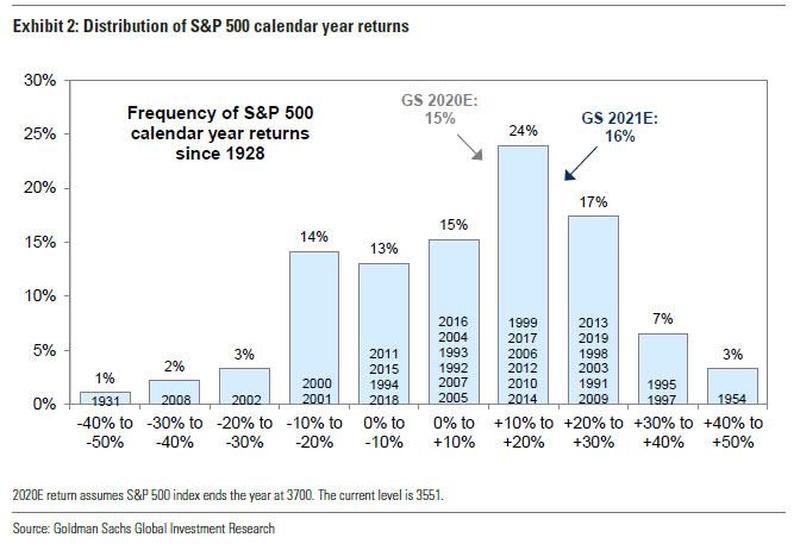

- “To justify this berserk forecast which can only happen in a world where there is no business cycle and where (digital) money literally grows on magic money trees, Goldman writes that ‘the S&P 500 annual return has been between 10% and 20% roughly 25% of the time since 1982.’” – bto: was natürlich nicht ewig sein kann, wachsen doch die Gewinne strukturell nicht schneller als die Wirtschaft.

Quelle: Goldman via Zero Hedge

{kind=link}