Italiens Position im Euro ist unhaltbar

Es ist bekannt, dass die Position Italiens im Euro nicht haltbar ist. Offen bleibt, wie lange es noch dauert, bis es zum Knall kommt. Die Hintergründe habe ich immer wieder bei bto besprochen und sie finden sich im Italien-Special, besser gesagt im Uscitalia-Special.

Hier aber zur Erinnerung nochmals die Betrachtung von der Insel, die – wie ich immer wieder betone – keineswegs irre ist, sondern einfach ökonomisch nüchterner und damit rationaler:

- “The markets seem to be fairly relaxed about the Italian situation. (…) They are focused on the immediate future. For all the sabre-rattling, the Italian government will not want an early showdown with the commission. And the commission would probably accept some sort of fudge. It will surely strive to avoid fining Italy.” – bto: Ohnehin ist es eine Frechheit, so gegen Italien vorzugehen und die Franzosen seit Jahren nicht anzupacken. Zeigt deutlich, wie die EU funktioniert.

- “(…) the government actually runs a budget surplus. Indeed, it has done so for 25 of the last 27 years. Italy shouldn’t have to squeeze its budget still further. The fiscal problem derives from a combination of a heavy weight of debt incurred in the past and very sluggish economic growth, continuing into the present.” – bto: Auch das ist bekannt und zeigt, dass man sich aus der Überschuldung nicht heraussparen kann. Möglich wäre natürlich eine hohe Vermögensbesteuerung in Italien, doch das Gegenteil ist der Fall. So ist die Erbschaftssteuer ein Witz im Vergleich zur hiesigen Belastung.

Quelle: The Telegraph

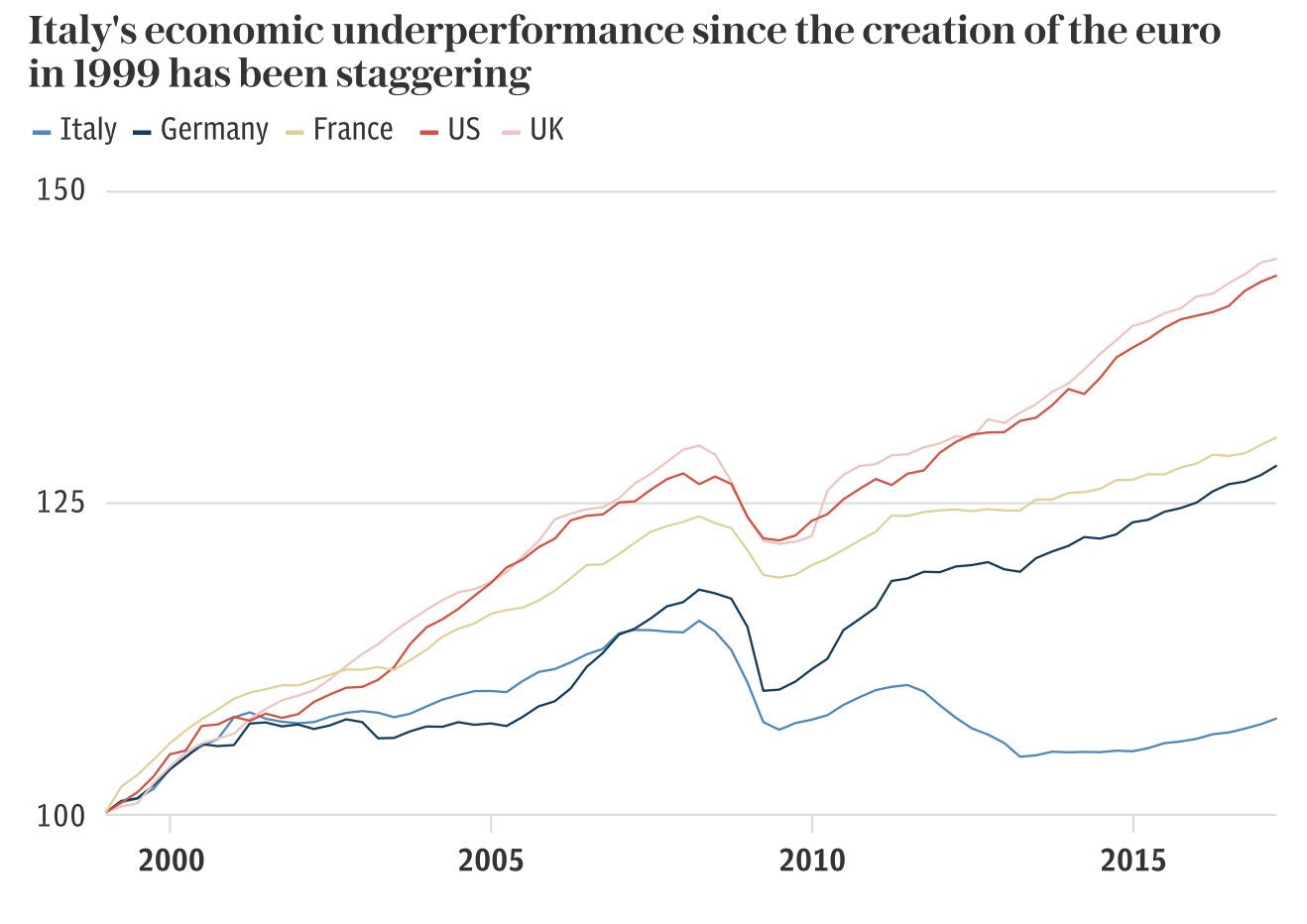

- “(…) if Italy’s sclerotic economy has hardly managed to achieve any growth when its leading trading partners have been growing well, then what is going to happen if and when they experience a serious economic slowdown, such as is now under way? (…) It is difficult to see how the Italian people or their political leaders will accept such a result meekly.” – bto: Und das dürfte wohl stimmen. Bisher ist das Land eigentlich schon erstaunlich friedlich.

- “The course that would be open to Italy if it were not a member of the euro would be a depreciation of its exchange rate, combined with a more stimulatory fiscal and monetary policy.” – bto: im Euro nicht möglich, also außerhalb?

- “(…) a majority of Italians still do not want to leave the euro. This is a major political barrier stopping any Italian government from taking Italy out of the euro.” – bto: was auch daran liegt, dass die Italiener Vermögen haben und fürchten, dass es entwertet wird.

- Aber man soll nicht so viel auf die Meinungsumfragen geben, meint Roger Bootle: “If there had been a poll of British people before we left the Gold Standard in 1931 I am sure that there would have been an overwhelming majority for staying on it, even though it was the cause of major economic difficulties. Similarly, if you had conducted a poll of British voters on continued membership of the European Exchange Rate Mechanism before we were forcibly ejected on Sept 16 1992, a day that was soon dubbed Black Wednesday, a majority would have voted to stay in.” Der Grund dahinter: “People tend not to like such radical shifts. Accordingly, they need to occur through some sort of shock, without people having a choice in the matter.” – bto: ein interessanter Gedanke, der auch auf die Öffentlichkeit hierzulande zutrifft.

- “(…) the most promising route to that result is through the introduction of a parallel currency, such as the so-called ‘mini-BOTs’, that have been touted for some time. (…) They look like bank notes and could serve as money.” – bto: Und diese Vorbereitungen laufen ja bereits.

- Und jetzt kommt der Knackpunkt: “(…) if the ECB reacted by cutting off, or even limiting, support for the Italian banking system then Italy would be ready with a new currency in waiting. Italy could support the banks with its newly issued currency. To all intents and purposes, Italy would then be out of the euro. This result could be presented as deriving, not from the Italian government’s choices, but from the European Central Bank’s actions.” – bto: Ich halte das für undenkbar! Die EZB wird das nicht machen, weil sie damit eine politische Entscheidung treffen würde. Sie wird den Geldhahn nicht zudrehen, haben wir ja bei Griechenland und den ELAs gesehen, die direkt in den griechischen Staatshaushalt flossen.

- “No one should expect such events in the next few months, let alone this week. (…) But unless and until the economy produces some decent growth, you should expect something like this to happen one day. It is only a matter of time.” – bto: Auf jeden Fall wächst der Druck an.

→ telegraph.co.uk: “It’s only a matter of time before Italy’s Black Wednesday moment”, 16. Juni 2019