Ist die US-Unternehmensverschuldung doch kein Problem?

Immer wieder habe ich bei bto über die gestiegene Verschuldung der US-Unternehmen und daraus erwachsene Risiken gesprochen. Sogar der IWF hat vor den Folgen der gestiegenen Verschuldung gewarnt. Nun könnte es sein, dass das alles nicht so schlimm ist wie gedacht, weil die Schulden sich nur auf einzelne Sektoren beziehen und zugleich die Gewinne auf Rekordhoch sind:

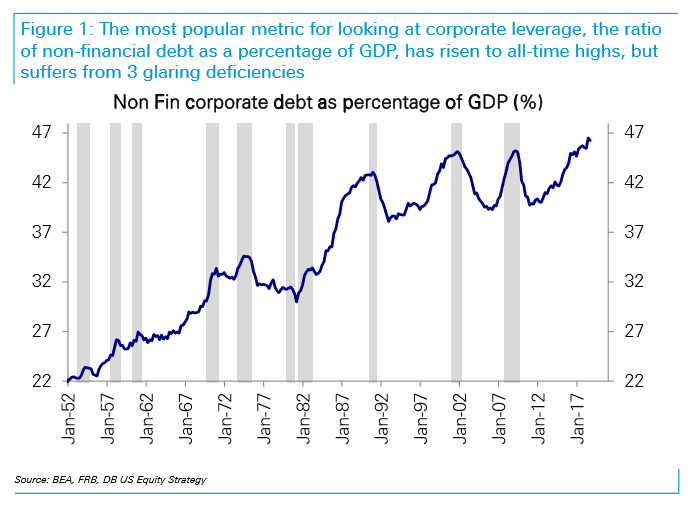

- “If you are looking for reasons to worry about the stock market, few things beat U.S. corporate leverage. (…) corporate debt has never been greater as a percentage of gross domestic product. (…) Deutsche Bank AG chief global strategist Bankim Chadha, (…) attempted in a report to show that the corporate debt issue had been overstated. He makes some very valid points (…)” – bto: Und diese Punkte schauen wir uns an:

Quelle: Deutsche Bank, Bloomberg

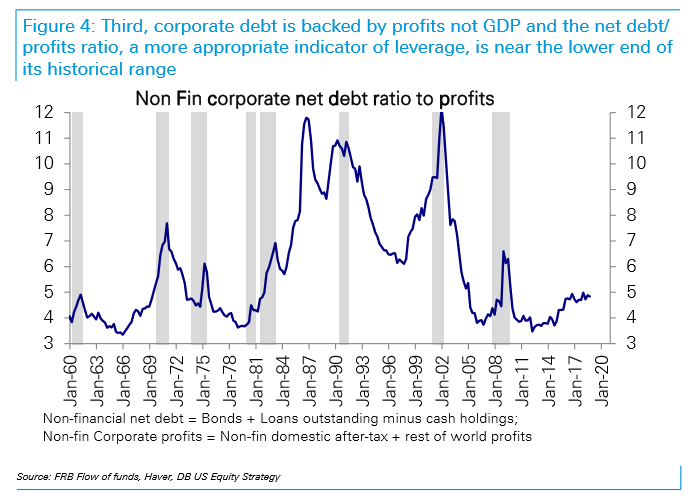

- “Chadha argues that we should be more interested in net debt, which subtracts out cash holdings, and compares that to profits rather than GDP. After all, it is from profits that the debt must ultimately be repaid. This leads to a radically different picture:” – bto: Was für ein schönes Bild! Die Verschuldung ist kein Problem, wenn man sie so bereinigt und dann über Zeit anschaut. Es sind wirklich gute Nachrichten und ich muss gestehen, Alarmismus ist nicht angebracht.

Quelle: Deutsche Bank, Bloomberg

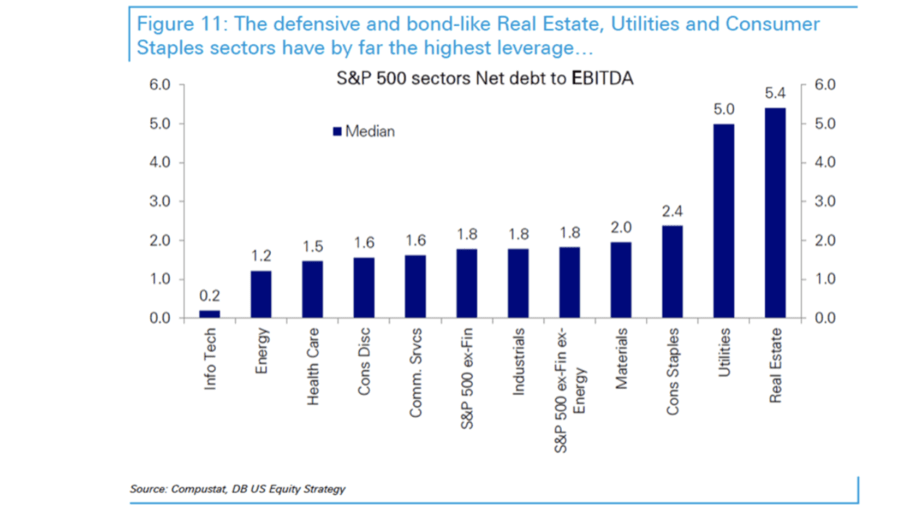

- “He also points out that leverage is heavily concentrated in the most relatively safe and boring sectors, led by utilities and real estate, which have reliable cash flows:” – bto: Das ist sinnvoll. Denn zum einen bekommen diese Sektoren am leichtesten Kredit, zum anderen wirkt der Leverage-Effekt hier über Zeit deutlich renditesteigernd.

Quelle: Deutsche Bank, Bloomberg

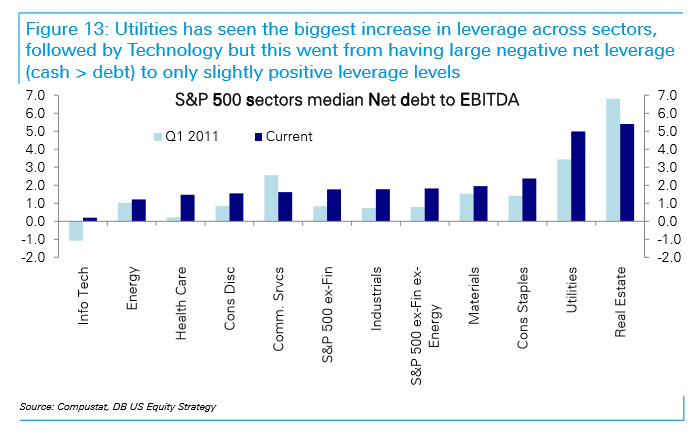

- “In particular, it is a story about utilities.” – bto: Das zeigt das Chart deutlich. Zwar ist die Verschuldung zum Teil deutlich gestiegen, aber von sehr tiefen Niveaus aus (zumindest, wenn man es mit Versorgern und Immobilienfirmen vergleicht).

Quelle: Deutsche Bank, Bloomberg

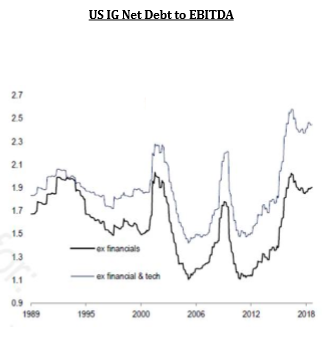

- “But there are still reasons for concern. (…) Rather than compare to profits, which many believe to be unrealistically high, the following chart compares investment-grade net debt to earnings before interest, tax, depreciation and amortization, which is a decent measure for cash flow. Non-financial corporates look almost as leveraged on this measure as they have at any time since the peak hit during the dot-com boom two decades ago. Excluding the tech sector, where companies are able to borrow against impressively high cash flows, corporate investment-grade debt looks as though it is at a historic high. Even if the debt is primarily taken on by companies with relatively strong cash flows, it is worth asking why they did not borrow so much before:” – bto: Ich finde, das ist ein gewichtiges Argument: vor allem die Bezugnahme auf die Cashflows, die eben nicht so verzerrt sind durch Leverage, das tiefe Zinsniveau und die Gestaltung der Jahresabschlüsse.

Quelle: Bloomberg

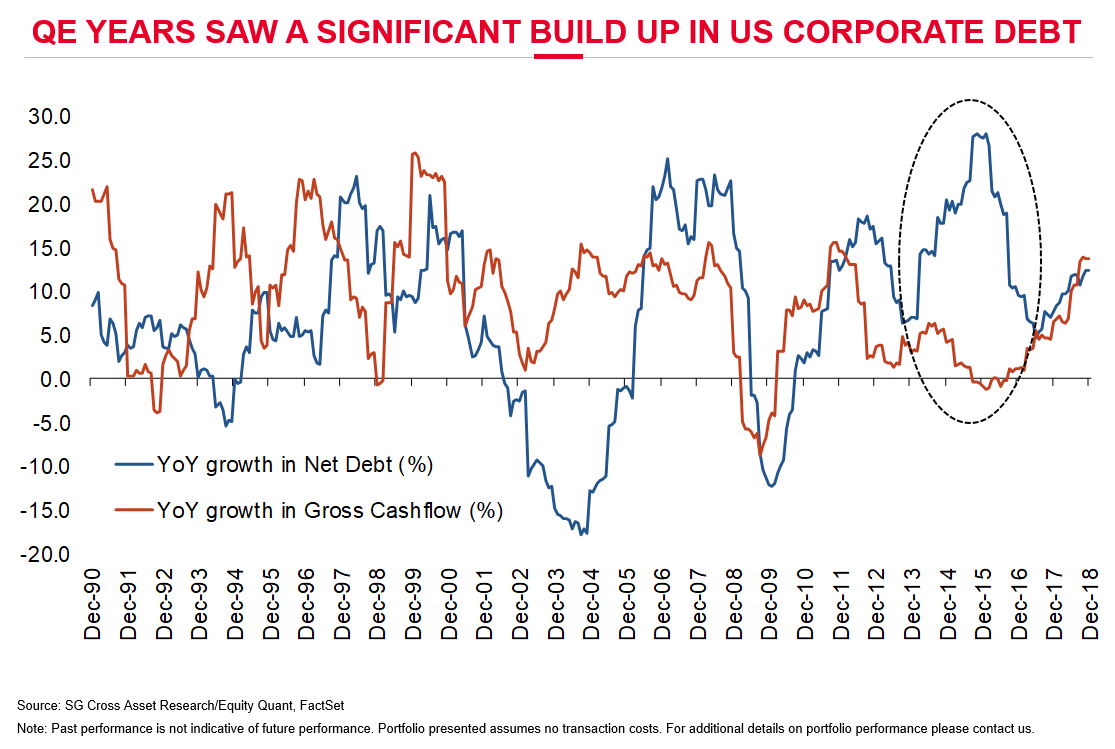

- “(…) this chart from Andrew Lapthorne, the chief quantitative strategist at Societe Generale (shows) in the era of quantitative easing following the financial crisis, net debt has increased far faster than cash flows:” – bto: Irgendwie mussten die Aktienrückkäufe ja finanziert werden und wenn Geld nichts kostet.

Quelle: SocGen, Bloomberg

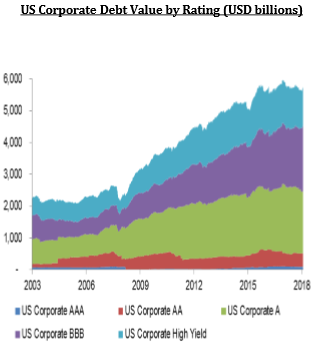

- “A further issue (…) is the obvious and persistent dilution of credit quality.” – bto: intensiv besprochen bei bto.

Quelle: Bloomberg

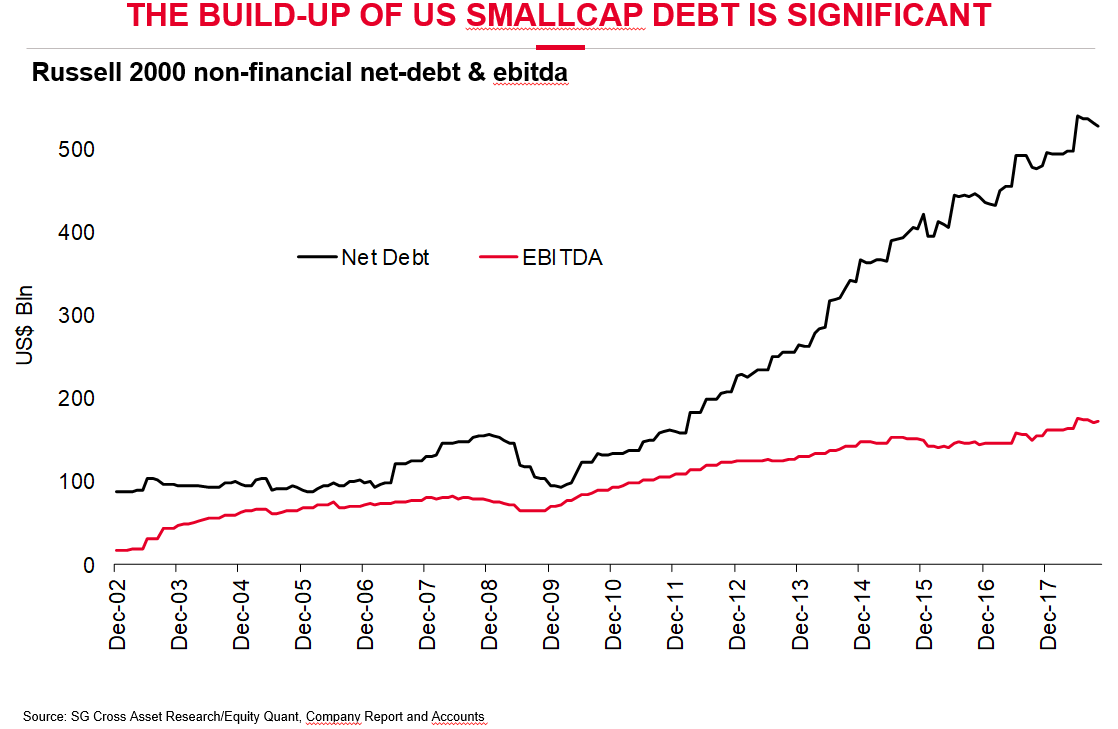

- “Debt with the highest AAA ratings has almost ceased to exist. And the greatest increase in debt volume by far has come in the lowest-quality investment-grade credits and in below-investment-grade. It looks like corporate borrowers are gaming the ratings firms (and not for the first time) by making sure they borrow as much as they can while not suffering the downgrade that would lead to higher borrowing costs. While Chadha’s numbers are for the larger companies in the S&P 500, Lapthorne produces this alarming data showing that the net debt of the smaller companies in the Russell 2000 has run far ahead of their cash flows:” – bto: Dieses Chart hatte ich auch schon mal.

Quelle: SocGen, Bloomberg

- “This is alarming, even if it does not imply a risk of imminent disaster for the S&P 500. The presence of leverage increases risks and it is plain that a lot of companies have taken the opportunity to stretch themselves to an unprecedented extent. Even if this corporate leverage doesn’t drive investors out of equities broadly, balance-sheet quality is likely to be a critical issue for anyone picking stocks. Avoiding the many companies that have over-levered looks imperative.” – bto: Das stimmt.

Außerdem lässt sich festhalten:

- Der Analyst der Deutschen Bank wollte auffallen. Ist aber nach hinten losgegangen, wenn Bloomberg ihn so einfach und deutlich zerlegt.

- Die US-Unternehmensverschuldung ist ein Problem, weil sie sich auf die schwächeren Unternehmen konzentriert

- und schon vor der Krise mit einer deutlichen Verschlechterung der Qualität einhergeht.

- Die Schulden wurden für Konsum verwendet, nicht für Investitionen. Das macht sie noch problematischer.

Ohnehin halte ich mehr von Handlungen als von Studien. So berichtet die New York Times, dass die Wall Street sich schon auf das Schlachtfest mit gefallenen Unternehmen und deren Anleihen vorbereitet. Es werden entsprechende Experten eingestellt:

- “Wall Street is hiring like gangbusters — because of a looming global credit crunch that could roil markets, and torpedo funds and businesses. Firms are signing on professionals to profit off a mountain of near-junk corporate debt, according to insiders. The Street is thought to be gearing up for the doomsday scenario some are expecting: a massive wave of corporate debt defaults, bankruptcies, restructurings and widespread layoffs.(…) hedge funds and banks snatch up teams of traders, credit and legal analysts, and managers tasked with profiting from this rising tide of high-risk corporate debt worldwide.” – bto: So verdient man doppelt; erst am Verkauf der Papiere, dann an den Problemen.

- “The US is awash in BBB-rated bonds. In the past decade, the triple-B bond market — a notch above junk — has catapulted from $686 billion to $2.5 trillion, an unsurpassed record, (…) Many worry about a surge of triple-B bonds being downgraded to junk, a step that would result in huge losses for many funds — some now leveraged to the hilt — and also undermine economic confidence. And while subprime was center stage during the 2008 financial crisis, this bad corporate debt could be the cause of the next recession.” – bto: was den Bankern egal ist, Hauptsache die Kasse klingelt!

→ nypost.com: “Wall Street prepares to profit off looming global credit crunch”, 8. April 2019