Hat Italien Angst, dass der Geldfluss aufhört?

Heute Morgen ging es darum, wie die EZB und die italienische Notenbank das Schuldenproblem Italiens aus der Welt schaffen. Durch die gezielte Monetarisierung der Schulden, sicherlich mehr als geduldet von der Bundesregierung, die unstrittig andere Interessen vertritt, als Schaden vom deutschen Volk abzuwenden. Deshalb ist auch klar, dass Herr Weidmann, so sehr ich ihn auch schätze, nicht die Nachfolge von Mario Draghi antritt. Es geht einfach nicht.

Das zeigt sich an den Kommentaren, die auf das Risiko für Italien hinweisen, sollte die Bundesbank wieder mehr zu sagen haben. So Ambroise Evans-Pritchard im Telegraph. Alleine ist er mit seiner Meinung sicherlich nicht:

- “The approaching end to the QE-era pulls away the protective shield for Italy and the high-debt Latin states, and for thousands of ‚zombie companies‘ kept afloat on monetary life-support.” – bto: So ist es. Ohne billiges Geld platzt der Traum von der gelungenen Eurorettung.

- “The (…) tightening of policy, even though the bank admitted that it will not come close to achieving its 2pc inflation target this decade. This leaves the eurozone with minimal safety buffers in the next cyclical downturn, vulnerable to a Japanese deflation trap.” – bto: Auch das Problem ist klar. Es wäre nicht wie in Japan, weil wir verschiedene Länder sind und die Leidensbereitschaft nicht so ausgeprägt ist.

- “The ECB has been soaking up eurozone sovereign bonds for the last three years under its QE programme, masking the true fiscal position of vulnerable states. This ‘golden age‘ is coming to end. The loss of the ECB shield leaves Italy nakedly exposed to market discipline at a delicate time.” – bto: Ich denke nicht, dass es wirklich zu Problemen kommt, eben weil die EZB allen öffentlichen Aussagen zum Trotz alles tun wird, um eine solche Krise zu verhindern.

- “Bond purchases have fallen from a monthly peak of €80bn (£70bn) to €30bn. (…) (The) gauge of money supply growth – real six-month M1 – has dropped to the lowest level since the Great Recession. It points to a marked economic slowdown later this year.” – bto: was dann natürlich, sollte es so kommen, die politischen Spannungen weiter erhöht.

- “(…) the bar for further QE is high. A major shock would be required for the ECB to change its mind, (…) There are technical reasons for this. The ECB’s balance sheet will reach 44pc of GDP by the autumn, beyond levels thought safe by the US Federal Reserve. Former Fed chief Alan Greenspan says the ECB is already out of its depth in treacherous waters.” – bto: Ach! Die Schweizer Nationalbank hat mehr als 100 Prozent vom BIP. Ich denke, die Richtung bleibt klar.

- “There is mounting anger in the Bundestag – where the anti-euro AfD party chairs the budget committee – over the true motives for emergency policies so late in the business cycle. Real interest rates in Germany are minus 2.5pc, (…).” – bto: Da bei diesem Thema ein (Medien)-Kartell der “Euroretter“ besteht, denke ich nicht, dass es den erforderlichen Politikwechsel geben wird.

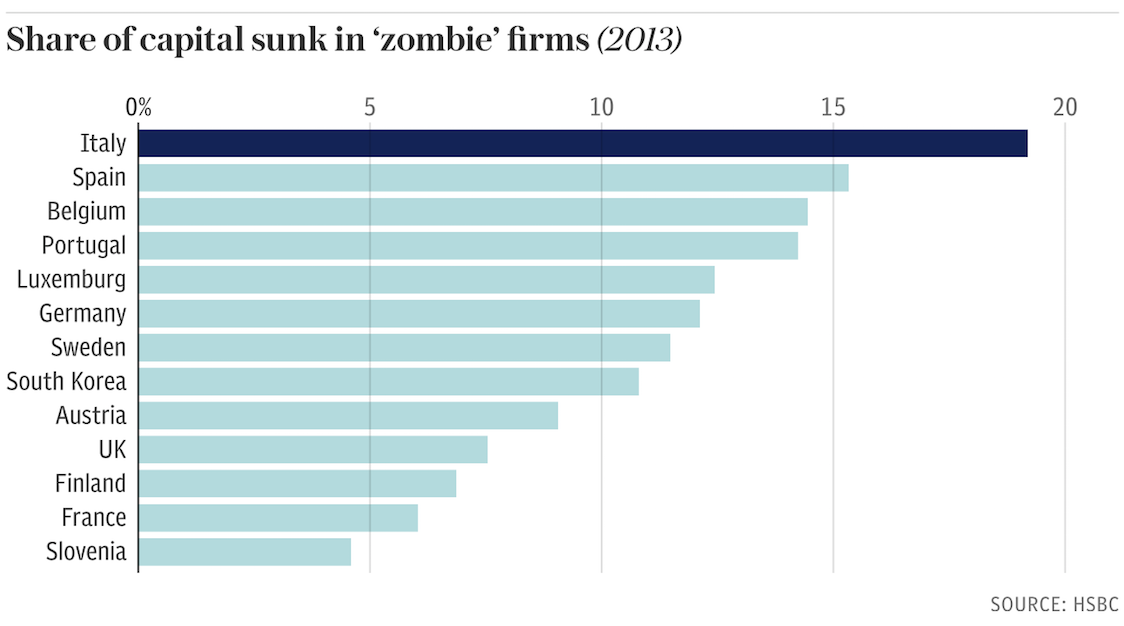

- “As September draws nearer, all those kept afloat by QE and easy money policies may come under scrutiny. (…) 9pc of Europe’s companies are walking dead with interest payment costs above their earnings. This has led to a systemic misallocation of capital that will come home to roost. (…) Europe may experience a “flash” jump in default rates.” – bto: Das wäre sicherlich so, wenn es so weit käme. Ich bleibe aber skeptisch.

Quelle: HSBC, Telegraph

- “The problem for Italy is that QE has flattered its fiscal profile. (…) the ECB has mopped up half the gross supply of Italian debt and shaved at least 100 basis points off Rome’s borrowing costs. The underlying picture – adjusted for the cycle – has been worsening. A depreciation allowance of up to 250pc turbo-charged investment and gave the economy a sugar rush, but only by drawing forward fiscal stimulus.” – bto: Und weil Italien so wichtig ist, ist es undenkbar, dass diese EZB-Hilfe ausläuft. Es geht schlichtweg nicht.

- “The county must refinance debt equal 17pc of GDP this year, one of the highest ratios in the world. There are no obvious buyers. Italian banks have been selling, rotating the proceeds into accounts in Germany or Luxembourg. It is slow capital flight. This pushed Italy’s Target2 liabilities in the ECB’s internal payment system to a record €444bn even before the victory of the Five Star Movement and the anti-euro Lega in the elections. It may take a mucher higher yield to entice the money back.” – bto: Das ist undenkbar, weil die Zinsen signifikant höher sein müssten!

Ich denke, der große Irrtum der Beobachter ist, dass sie es für denkbar halten, dass

- die deutsche Politik einen echten Wandel will – will sie sicherlich nicht.

- die Bundesbank mehr Einfluss bekommt – sicherlich nicht.

- Herr Weidmann die Nachfolge von Herrn Draghi antritt. Undenkbar!

→ The Telegraph: “Bundesbank back in charge of ECB, sending shivers through Italy”, 8. März 2018