Haben die US-Unternehmensmargen den Höhepunkt erreicht?

Vor einigen Tagen habe ich die Studie besprochen, die als Ursache für die gute Entwicklung der US-Börse den nachhaltigen Anstieg des Anteils der Kapitaleinkommen am BIP identifiziert hat. Hat die Ausweitung der Margen die Börsen nach oben getrieben, muss dies doch auch umgekehrt zutreffen. Sollten die Margin also fallen, müsste es auch bergab gehen mit den Aktien. Ursachen könnten sein:

- höhere Löhne

- höhere Steuern

- bessere Überwachung des Wettbewerbs

John Authers hat in seinem Newsletter bei Bloomberg das Thema ebenfalls aufgegriffen. Tenor: Es könnte sein, dass die Margen der US-Unternehmen ihren Höhepunkt schon hinter sich haben. Hier seine Gedanken:

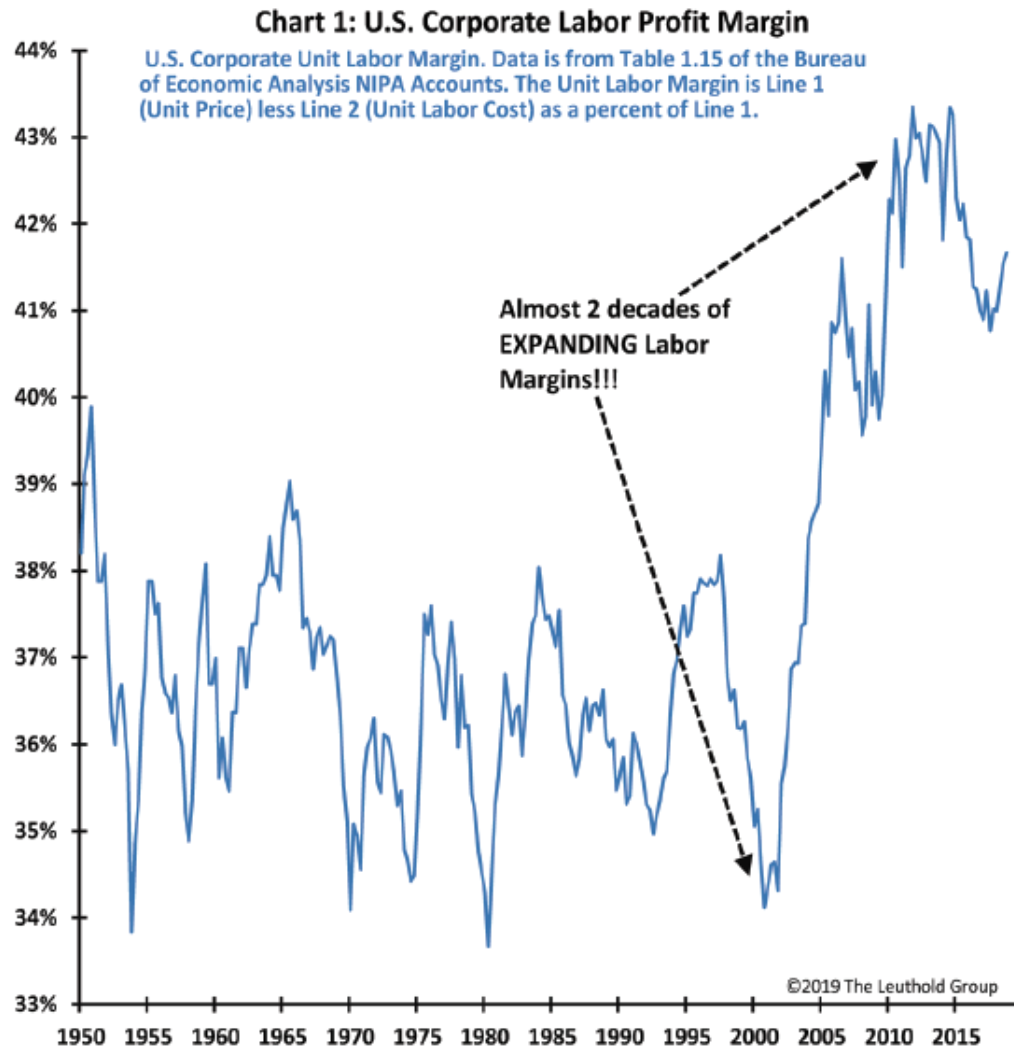

- “(…) for the remainder of this earnings season, expect a tight focus on wages and whether they are biting into corporate profit margins. The moment when Main Street finally starts to benefit at the expense of Wall Street has been anticipated for years. Many analysts think it is upon us at last. Bears have been wrong for much of the last decade, and one key reason for this has been a belief that profit margins were about to revert to the mean. Over history, margins have been reliably mean-reverting — until the last decade or so.” – bto: Und was man klar sieht ist, dass es eben nicht zur Rückkehr zu langfristigen Durchschnitten kam. Im Gegenteil:

Quelle: Bloomberg

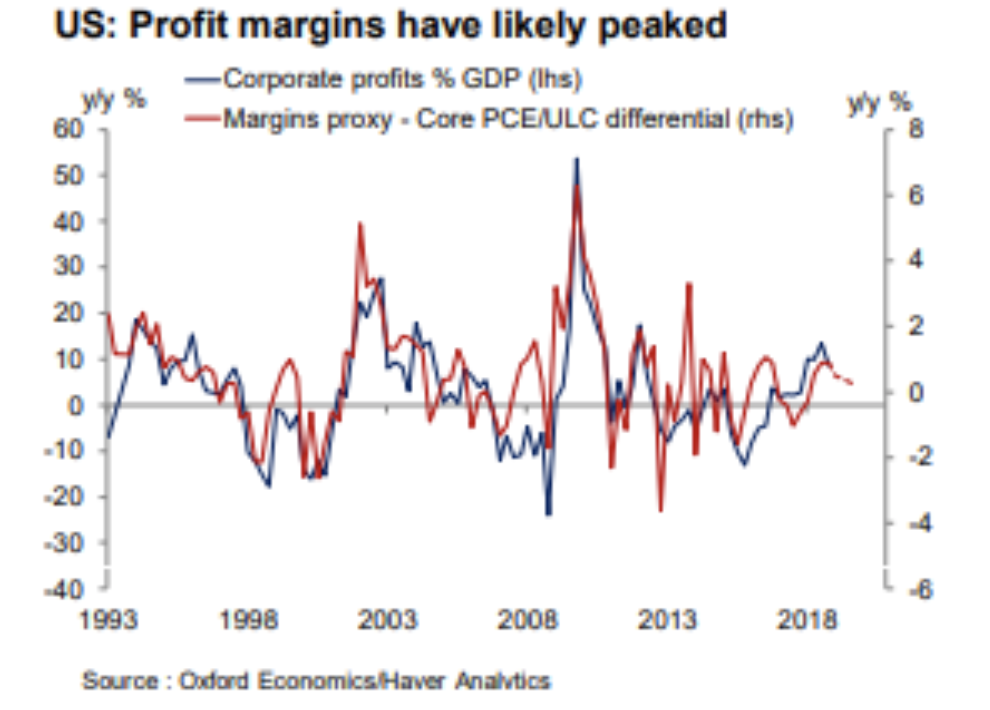

- “Average earnings growth is ticking up. It’s not yet sparking faster inflation to any extent that would make central bankers uncomfortable. But that may be because companies feel unable to pass on their costs to consumers, which implies tighter margins. Further, margins have improved in the last few quarters, in a way that Oxford Economics suggests could be unsustainable. Their predictions for slow inflation and rising unit labor costs suggest margins are about to tighten.” – bto: Leider wird nicht gesagt, was an dem Anstieg “unsustainable” war. Jedoch würden sinkende Margen ohne Zweifel dem Markt zusetzen.

Quelle: Bloomberg

- “Goldman Sachs is also suggesting that margins are under pressure from rising labor costs. Its low-labor-cost basket covering the 50 stocks in the S&P 500 which have the lowest proportionate labor costs tends to track expected inflation. If there is evidence that wage costs are rising and creating inflationary pressure, then expect these stocks to outperform.” – bto: was sie aber offensichtlich noch nicht tun. Also alles gut?

Quelle: Bloomberg

- “Rising wage costs would be bad news for the S&P 500.” – bto: So ist es.

Ich habe nicht verlinkt, um mein Kontingent bei Bloomberg nicht aufzubrauchen. Ich empfehle meinen Lesern aber, den kostenfreien Newsletter von John Authers bei Bloomberg zu abonnieren.