Globales Schulden-Update: nicht gut

“Schulden-Blog” wird bto nicht selten genannt. Ein guter Grund, um mal auf die aktuellen Zahlen zu blicken, zusammenzugestellt von der Bank of America und von Zero Hedge der Allgemeinheit zugänglich gemacht:

- “As BofA’s Barnaby Martin succinctly puts it, much more debt is coming since ‘the legacy of the COVID shock is debt, debt and more debt.’ In short: use even more debt to ‘fix’ a debt problem.” – bto: Wir bekämpfen seit Jahren die Probleme zu hoher Schulden mit noch mehr Schulden.

- “Global debt/GDP surged to an all-time high in Q1 ’20, with overall debt for the non-financial sector now worth 252% of global GDP. This is up from 241% at the end of 2019, the biggest quarterly jump ever according to BIS data.”

Quelle: BofA

- “This increase reflects the fallout from the first few weeks of the COVID crisis, with most advanced economies implementing total or partial lockdowns in March. Hence, the historical contraction in GDP growth observed worldwide in Q2 and the debt surge from both governments and non-financial corporations will translate into an even bigger rise in the global leverage ratio in Q2 ’20.” – bto: Nur bei uns kommt man auf die Idee, dieses über Steuern lösen zu wollen. Was für ein Blödsinn.

- “While both advanced economies (DM) and emerging markets (EM) have seen their leverage ratios jump, the latter have observed a rapid increase since 2012 (Chart 13). The relatively deeper COVID recession expected for some EM economies – the OECD Sep ‘2020 Economic Outlook sees India and South Africa GDP falling by 10.2% and 11.5%, respectively – will likely magnify the jump in some EM’s leverage ratios.” – bto: weshalb bereits offen von einer neuen Schuldenkrise gesprochen wird.

Quelle: BofA

- “By sectors, governments drove the big uptick in debt/GDP in Q1 ’20. The global sovereign debt-to-GDP ratio has reached 89%, up 10 percentage points, the largest quarterly rise on record.” – bto: Das überrascht weder noch besorgt es. Denn es spielt ja dank MMT keine Rolle.

- “Debt service ratios ticked up, but only marginally, reflective of the tremendous QE support unleashed by central banks this year.” – bto: Richtig, die Zauberlehrlinge haben das Schuldenmonster, das sie schufen, weiter aufgepumpt.

Quelle: BofA

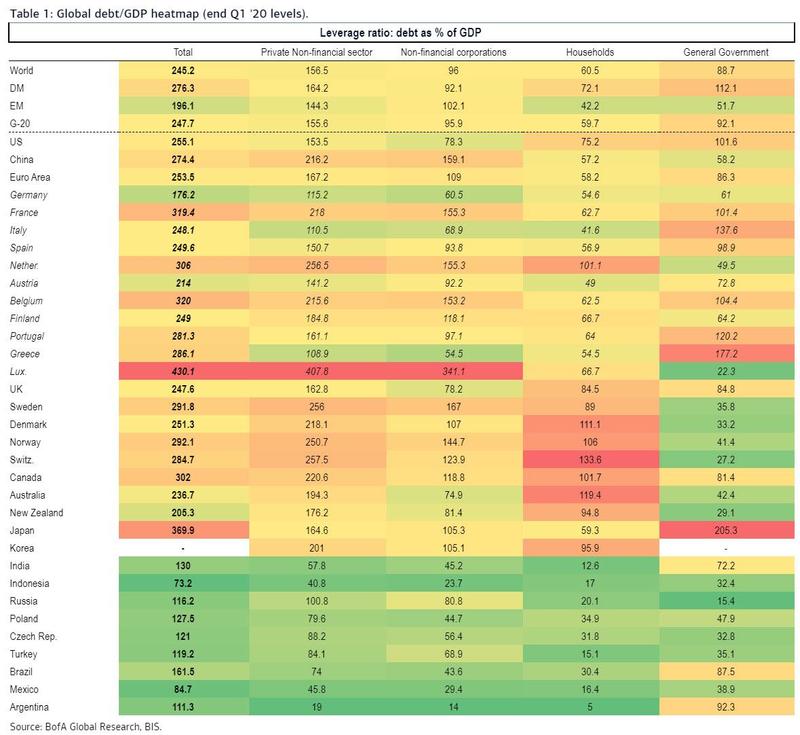

- “The total leverage ratio for Euro Area, China and the US are mostly in line now.” – bto: Es bedeutet auch, dass alle dasselbe Interesse haben, nämlich die Schulden zu entwerten.

- “In Europe, a number of core countries (Belgium, Finland and Norway) saw a bigger increase in their total debt/GDP ratio than in the periphery in Q1 ’20.” – bto: weil sie es konnten oder weil sie – wie Belgien – wissen, dass sie von der EU “gerettet” werden.

- “While the rise in household debt has generally been more modest as consumers have moved into wait-and-see mode, China household debt/GDP rose 3.1% QoQ in Q1 ’20.” – bto: von einer deutlich tieferen Basis ausgehend.

Finally, the table below show global debt/GDP leverage ratio across the globe, broken down by countries and segments. – bto: Ich finde, die ist sehr interessant:

Quelle: BofA

Italien und Deutschland sind “grün”. Ja, Italien. Der dortige Privatsektor hat – Leser von bto wissen das! – tiefere Schulden als wir Deutsche … So viel zum Thema, wir müssen retten.

→ zerohedge.com: “Global Debt Is Exploding At A Shocking Rate”, 20. September 2020