Europa auf dem Weg nach Japan – nur schlimmer

Europa ist fest auf dem Weg in ein japanisches Szenario. Aus mehreren Gründen wird es bei uns allerdings nicht so kommod ablaufen:

- Die EZB wird anders als die Bank of Japan später handeln und damit die Flughöhe der Japaner nicht erreichen.

- Die Produktivität pro Kopf wächst hier deutlich schlechter, was mit fehlenden Investitionen und abnehmender Bildungsqualität zu tun hat.

- Die Bevölkerung ist aufgrund der Zuwanderung der letzten Jahrzehnte nicht so homogen und deshalb vermutlich weniger bereit als die Japaner, Einschränkungen hinzunehmen.

- Die Eurozone ist nicht ein Land, sondern eine Ansammlung mehrerer Länder, die eigene Interessen in den Vordergrund stellen werden, was die Spannungen verschärft.

Die Märkte signalisieren zumindest, dass wir ökonomisch auf dem Weg sind:

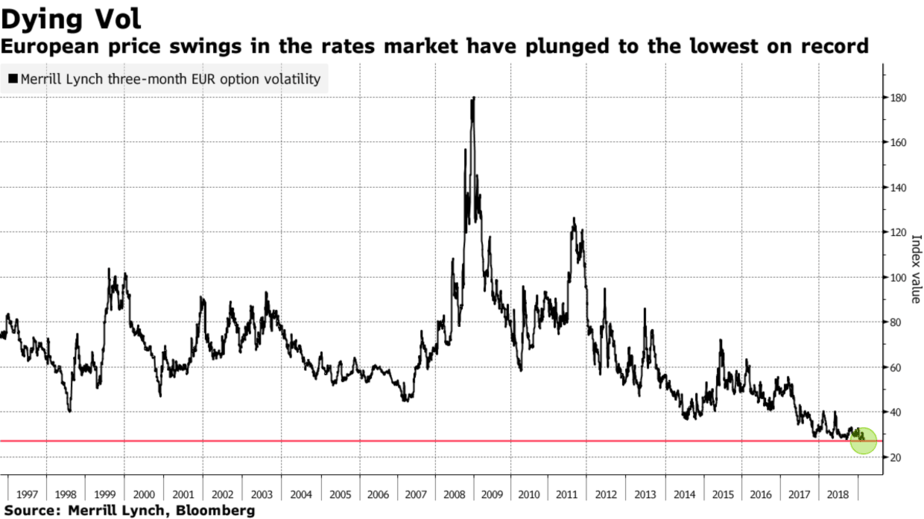

- “Europe’s bond volatility is grinding to a halt, leading investors including Pimco to fear the region’s economy and markets are spiraling toward their own version of Japan’s lost decade. ‘There’s a strong probability that what happened in Japan two decades ago is currently unfolding in the euro zone right now,’ said Andrew Bosomworth, a money manager at Pacific Investment Management Co. ‘It probably means the Japanification of capital markets – lower yields for a longer time. Maybe forever.’” – bto: was ein entsprechendes realwirtschaftliches Szenario bedeutet.

- “Price swings in the European sovereign debt market are the most depressed in history, (…) That has already helped push benchmark German Bund yields to the lowest in two years and spurred record demand for the higher returns from riskier peripheral debt.” – bto: Das ist nicht so riskant, weil es klar ist, dass im Zweifel die EZB alle raushaut.

Quelle: Bloomberg

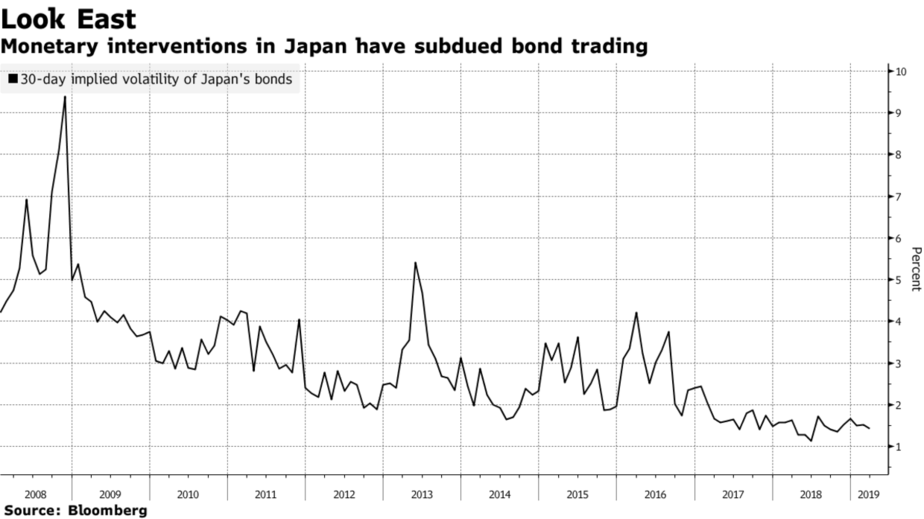

- “That leaves investors doubting the European Central Bank will be able to extricate itself from a negative interest-rate policy, mirroring Japan’s struggle to revive its economy from years of flat-lining growth. The Asian nation became the first to cut borrowing costs to zero 20 years ago, eroding debt-price swings and trading volumes. The low volatility trend was exacerbated by the country’s central bank implementing a bond curve control policy in 2016, limiting the range that 10-year yields could go either side of zero percent.” – bto: Das bekommen wir alles, wenngleich es bei der EZB wegen des Streits mit den Nordländern dauert. Deutschland hat hier ohnehin schon resigniert.

- “(…) parallels between the euro zone and Japan’s experience on the time it’s taking to clean up non-performing loans in the banking sector and on ageing populations, an ‘elephant in the room’ that is leading to lower structural inflation. That is likely to mean central banks keep rates low for decades (…).” – bto: Das ist nur vordergründig eine gute Nachricht, weil die Europäer, anders als die Japaner, nicht so leidensfähig sind.

Quelle: Bloomberg

- “The collapse of bond volatility and convergence of European core bond yields to Japanese government bonds is a sign Europe is facing the risk of structural low inflation, (…) Traders betting on ‘lower-for-longer’ are flattening both nominal and inflation-linked yield curves in Europe, while bonds of historically riskier nations, such as Spain and Portugal, have rallied. Those bonds offer some of the highest ‘carry,’ or larger coupon payments, that are a worthy investment should volatility stay low and political turbulence muted.” – bto: und mit der Versicherung der EZB.

- “It’s also why the rally in Bunds may not be done yet. The securities provided one of the few sources of returns for investors last year as the Federal Reserve hiked and the bull run in equities drew to an end.” – bto: Es zeigt, wie krank das System mittlerweile ist. Ja, es hat viel mit Demografie zu tun. Aber eben auch mit den ungelösten Problemen bei Schulden und Produktivität.

→ bloomberg.com: “Death of Bond Volatility Has Pimco Fearing for Europe’s Future”, 6. März 2019