Diese Inversion der Zinskurve ist schlimmer als frühere

Mittlerweile haben es alle mitbekommen: Die Zinskurven haben sich in vielen Ländern “invertiert”. Damit ist gemeint, dass die Zinsen für zehnjährige Anleihen unter dem Niveau für zweijährige liegen. Gemeinhin – aufgrund historischer Erfahrung – als klarer Indikator für eine bevorstehende Rezession gesehen. In den USA war es das tägliche Thema in den Wirtschaftssendungen und TV-Sender haben sich alle Mühe gemacht, die Risiken kleinzureden und die Privatinvestoren in die Märkte zu treiben. So zumindest mein Eindruck bei meinem kürzlichen Aufenthalt.

John Authers nimmt sich in seinem exzellenten, kostenfreien Bloomberg Newsletter des Themas an. Ich finde es immer wieder faszinierend, ihn zu lesen und denke, er ist ein herber Verlust für seinen früheren Arbeitgeber FINANCIAL TIMES (FT) und ein tägliches Muss für jeden, der sich mit Geldanlage beschäftigt.

- “The most widely watched part of the U.S. Treasury market’s yield curve has finally inverted. (…) Should we care? And, if so, why should we care?” – bto: Ich finde, es ist gut, diese Frage nochmals erklärt zu bekommen.

- “Historically, yield curve inversions have been reliable early indicators of a recession. (…) But we only have a sample of seven recessions to study, and the circumstances in all those inversions were slightly different. (…) What is most notable this time is the drop in longer-dated bond yields (…) The 30-year Treasury yield hit an all-time low(and) its recent decline is shocking in historic terms.” – bto: Das ist das Entscheidende. Es ist so gesehen dramatisch, andererseits angesichts der weltweit ohnehin schon sehr tiefen Zinsen wiederum nicht so überraschend. Dachte ich zumindest.

- “This is the 7th time in 35 years that 30-year yields have declined by such a large degree over a 10-day span.

- Oct 1987 – The week after stock market crash

- Jun 1989 – The week the Fed started easing (recession 13 months later)

- Feb 2000 – Tech bubble (Mar 2000)

- Nov 2001 – In recession

- Dec 2008 – The depths of the Great Recession

- Aug 2011 – The week after the U.S. lost its AAA rating and a 20% correction in the S&P 500″

- Aug 2019 – ???” – bto: Das ist natürlich eine nicht so schöne Auflistung.

- “The sharp drop in the 30-year yield brings us to another reason that is being cited to treat this inversion differently from its predecessors. This was, in the obscene-sounding vocabulary of the bond market, a ‘bull flattener.’ (…) this means that this inversion came as a result of long-dated yields coming down (a bullish event if you own bonds when this happens), rather than because short-dated yields went up, which would be a ‘bear flattener.’ (…) bear flatteners are more common. The explanation for this is that recessions usually come as the Federal Reserve raises short-term rates. This time, the Fed stopped tightening eight months ago, and rates have been heading down all year. So if anything, this inversion does look different from its predecessors, but scarier.” – bto: Das stimmt. Die Märkte selber signalisieren “Deflation und Rezession”. Oder aber es ist wirklich nur die Flucht aus der Negativwelt in Europa und Japan.

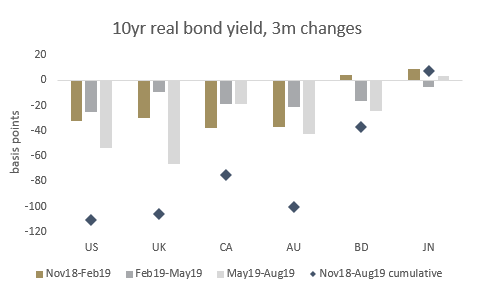

- Sodann verweist Authers auf den Aspekt, dass die Zinsen stärker gefallen sind als die Inflationserwartungen und wir es deshalb mit negativen Realzinsen zu tun haben. “Declines in real yields show specific anxiety about future growth among investors. And the last few months have seen a remarkable and coordinated drop in real yields around the world.” – bto: Das ist die Eiszeit. Eindeutig.

Quelle: Bank Mellon, Bloomberg

- “(…) the other precedents (…) without exception, happened with rates at higher levels. There is no precedent for yields this low, and therefore there is no precedent for an inversion at such low rates. This is a caveat that has hung over the financial world for a decade. Many things look alarming and unsustainable, but we simply have no experience to say whether they can be sustained with rates this low.” – bto: was die Optimisten dazu veranlasst, zu sagen, dass es diesmal anders ist. Dazu gehört dann auch Janet Yellen – wir erinnern uns, frühere Fed Chefin und berühmt für ihre Aussage, dass es keine Finanzkrise mehr in unserer Generation geben würde. Sie sagte im TV: “(…) I would really urge that on this occasion it may be a less good signal. The reason for that is there are a number of factors other than market expectations about the future path of interest rates that are pushing down long-term yields.” – bto: Na, dann ist ja alles gut!

- “(…) an inverted yield curve has real world effects (…). Banks make their money by borrowing for the short-term from depositors and lending at higher rates for the longer term. When those rates invert (or merely flatten), it becomes far harder for them to make profits. They have less incentive to lend, and they have less capital with which to withstand any risks. The inverted yield curve has quite rationally spurred a tumble for bank stocks in the U.S. and particularly in the euro zone. Banks are arguably less important to the U.S. economy than they were a generation ago; they are still central to the European economy, and further problems for European banks will create problems for the U.S.” – bto: Und die Banken sind ohnehin in Europa nicht von der Krise genesen.

- “That leads to yet another argument to ignore this latest yield curve inversion: that the pressure on the U.S. market at this point is largely from beyond American shores. Europe is in the midst of a deflation scare, and investors there are rushing to get yield wherever they can – which means buying Treasuries. (…) this makes sense but only to a point. Post-globalization, it is far harder for the U.S. to ignore events elsewhere in the world. The dollar is a critical point of pressure. If its economy remains strong, its currency will be bid up and that will dent American companies’ profits and render American exporters less competitive.” – bto: Und ein starker Dollar erhöht die Probleme all jener, die sich in US-Dollar verschuldet haben, aber in anderer Währung ihr Geld verdienen. Vor allem in den Schwellenländern. Das hat gewisse Margin-Call-Aspekte.

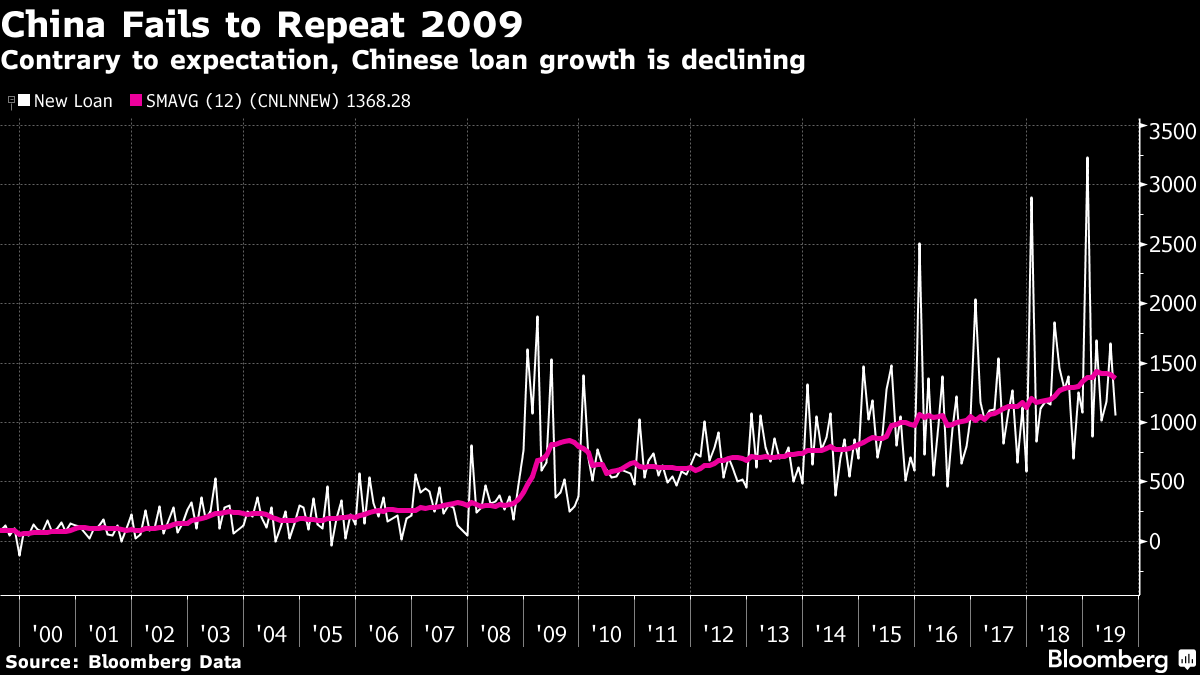

- “China was critical in allowing the rest of the world to escape from the recession that followed the Global Financial Crisis. The huge stimulus it announced in late 2008, in the form of extra loans, fired up the global economy. A the beginning of this year, investors’ working assumption that another big stimulus was on the way from China, to avert the risk of slowing. But the data (…) showed almost the opposite. If we look at a 12-month average (to avoid the distorting effects caused by China’s shutdown for the lunar new year), we see that new loan growth is actually slowing. This is nothing at all like the huge stimulus of 2009.” – bto: womit China der Welt nicht hilft. Warum auch, wenn es doch von den USA gerade unter Druck gesetzt wird?

Quelle: Bloomberg

“Does all of this prove that a recession is inevitable? No, nothing can do that. But it would be wise to take this yield curve inversion seriously, and act on the assumption that the chances of a recession have greatly increased. We should care about the inversion, and we should care because it will affect the world we live in.” – bto: Gerade für die Eurozone wird das ein Desaster werden. Trotz Helikoptern und MMT. Madame Lagarde kann eben auch kein Wachstum erzeugen.