Die wahre Wirkung der EZB-Politik

Jetzt, wo sich das (vorübergehende) Ende der Politik des billigen Geldes zumindest in den USA (und abgeschwächt in der Eurozone) abzeichnet, ein kurzer Blick auf die Wirkungen. Vom Sommer 2017:

Junk wurde gekauft wie wild:

Quelle: zerohedge.com

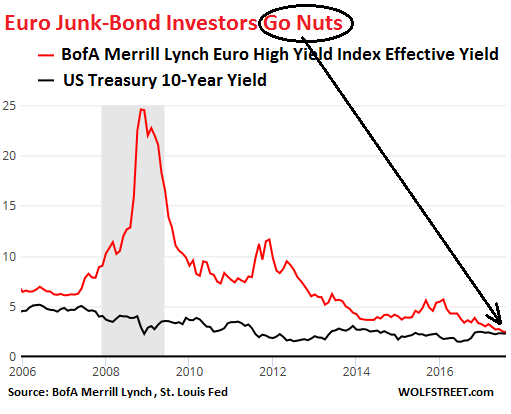

Damit wurden europäische Junk Bonds “sicherer” als US-Staatsanleihen – was sich, seitdem die Zinsen in USA steigen, weiter vergrößert hat:

Quelle: zerohedge.com

“‚European HY yields have almost declined to the yield on BofAML’s US Treasury index‘ adding that while ‚there are indeed duration differences between the two markets, it doesn’t detract from the eye-watering levels that European high-yield has now reached.‘”

Quelle: zerohedge.com

Quelle: zerohedge.com

“The results become even more eyewatering if one drills down on the ‚higher rated‘ European junk bonds, those in the BB bucket: here the relative value is ‚even more eye-watering‘ as over 60% of BBs rated HY bonds yield less than similar-maturity USTs and, ‚ironically, €23bn of Italian BBs now yield less than Treasuries.‘”

Quelle: zerohedge.com

“(…) the plunge in bonds yielding more than matched-maturity Treasurys started roughly around the time Draghi unleashed the CSPP, confirming yet again (in addition to the chart on top), that it was the ECB that made European junk bonds ‚safer‘ than US government paper.” – bto: und was nun? Wie lange hält sie das durch?

Quelle: zerohedge.com

Quelle: zerohedge.com

Das hat sich in den letzten Monaten allerdings geändert: “(…) around €23bn of Italian Euro BB-rated junk bonds yield less than equivalent-maturity US Treasuries.” – bto: Und hier wird es spannend werden in den kommenden Monaten. Die Zinsen in den USA steigen, der Spread für italienische Anleihen auch. Beides nicht verkraftbar in einer Welt mit zu vielen Schulden.

Quelle: zerohedge.com

Quelle: zerohedge.com