Notenbanken-Falle: Jeder Zinsanstieg zieht dem System den Stecker

Ich hatte bereits 2016 in meiner Kritik von Thomas Piketty gezeigt, dass es an dem billigen Geld und der immer höheren Verschuldung liegt, dass die Vermögen schneller wachsen als die Einkommen.

Das wesentliche Asset sind dabei Immobilien. John Authers zeigt in seinem Newsletter bei Bloomberg, wie stark sich die Immobilienpreise von der realwirtschaftlichen Entwicklung gelöst haben und wie sehr alles am billigen Geld hängt:

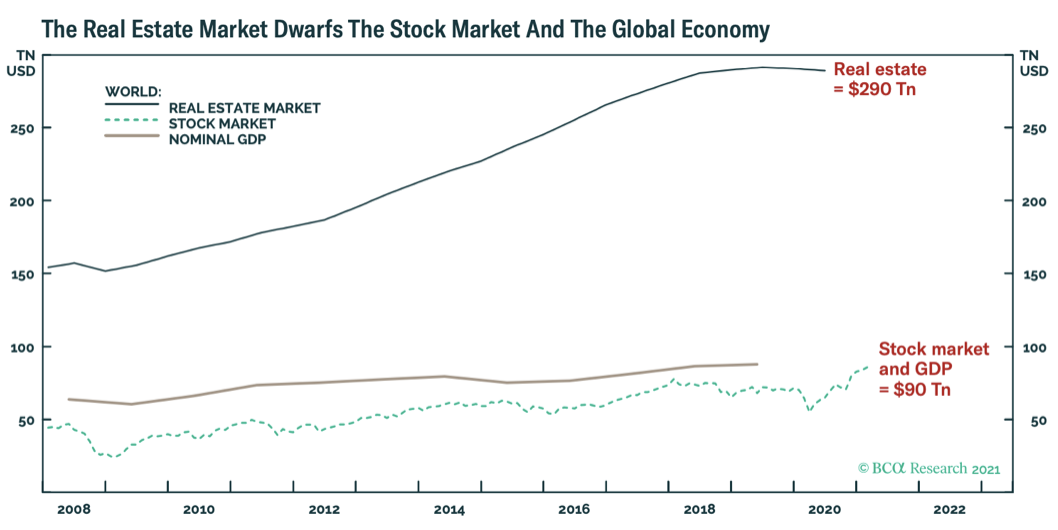

- “(…) global real estate, all bar about 10% of which is residential, is worth far more than the world’s entire supply of stocks and bonds. At some $290 trillion, it’s even worth far more than the world’s annual gross domestic product.” – bto: Die Abbildung verdeutlicht dies eindrücklich:

Quelle: Bloomberg

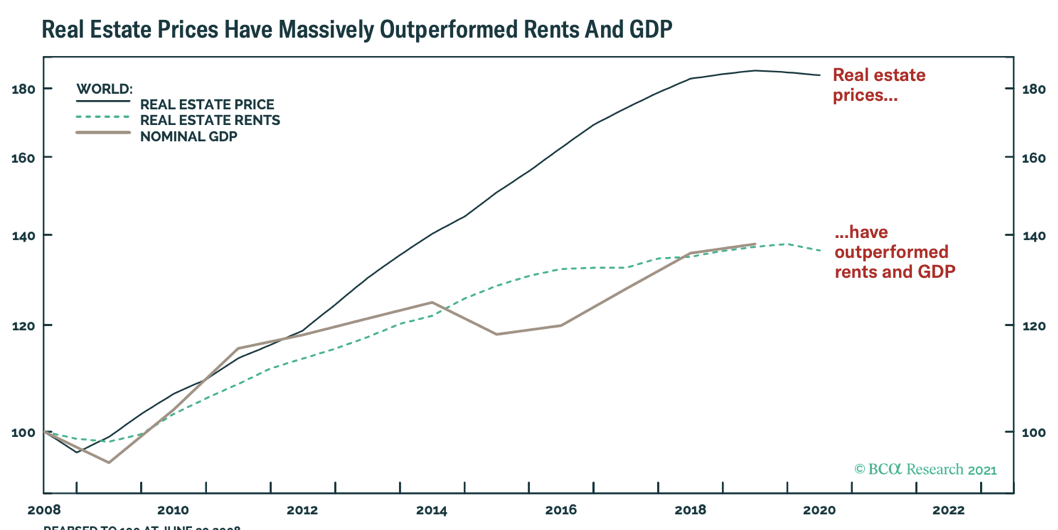

- “This is important because housing has boomed on the back of low yields just as much as stocks — in fact, probably more. (…) real estate prices have vastly outperformed rents, which have risen roughly in line with nominal GDP. Just as stocks’ P/E multiples have been buoyed by low yields, so house prices have been supported by startlingly cheap mortgage finance.” – bto: Genau das ist mein Problem: Immer höherer Leverage und immer tiefere Zinsen erzeugten einen enormen Wertzuwachs, und zwar als ultimative “Duration-Assets”.

Quelle: Bloomberg

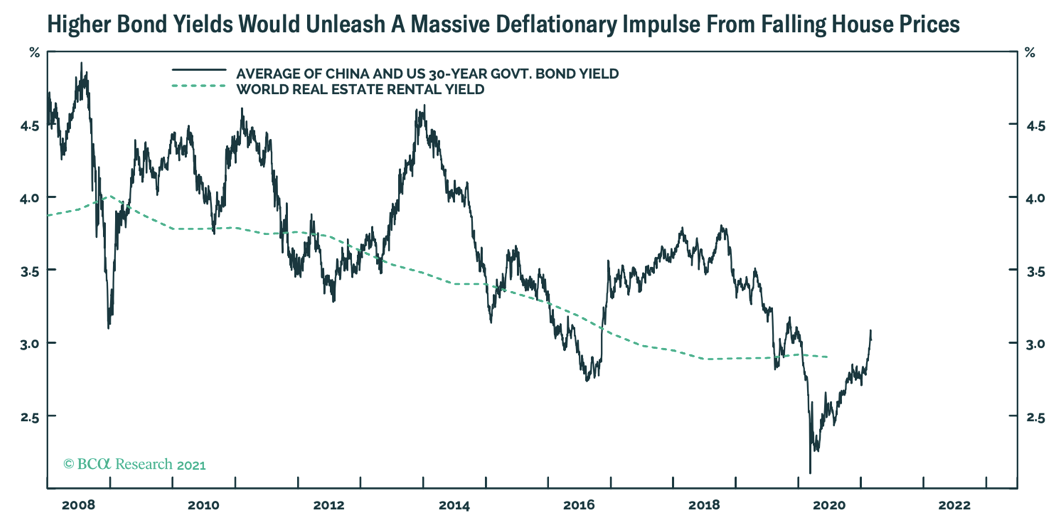

- “The implication is that we are all leveraged to low bond yields. (…) the implied rental yield paid by property has moved in line with yields on long U.S. and Chinese bonds. An increase in bond yields that in turn causes a drop of 10% in the level of global house prices isn’t hard to imagine. That would be a wealth effect of almost $30 trillion, or about a third of global GDP, and a sledgehammer to the world economy.” – bto: Deshalb muss es um jeden Preis verhindert werden. Nur wird es eben nicht zu verhindern sein.

Quelle: Bloomberg

- “(…) such a decline would inflict one last deflationary downdraft. That by extension means not betting all out on inflation just yet. (…) the crucial stress point would come when 30-year yields reach 3.75%: (…) if inflation fears lifted the average US and China 30-year bond yield to 3.75 percent (from 3 percent now), it would constitute the change in trend that would unleash a massive countervailing deflationary impulse from falling house prices.” – bto: ein in der Tat ungemütliches Szenario, wobei es natürlich auch eine positive Seite hätte: “(…) an entire generation seems to be unable to afford to buy a house, and adults are continuing to live in the parental home for many years after leaving school. That’s a clear indicator that housing is artificially expensive. Bringing prices down would be a great way to alleviate some of the ugliness and division in society — but it’s hard to see how that can happen without an accident.” – bto: Und was für einen, denn nichts nehmen die Banken so gern als Sicherheit wie Immobilien! Fallen die Immobilienpreise in dieser Größenordnung, dürfte das weltweite Bankensystem insolvent sein (so es das nicht ohnehin in vielen Ländern bereits ist!).