Die BIZ warnt und warnt und warnt … Ergeht es der Notenbank der Notenbanken wie den “normalen” Krisengurus?

In den vergangenen Jahren habe ich immer wieder die Bank für Internationalen Zahlungsausgleich (BIZ, oder englisch BIS) an dieser Stelle zitiert und manchmal auch den Jahresbericht ausführlich besprochen. Die dort gemachten Aussagen gelten noch immer:

→ Kreditbooms und Krise: Die BIZ sieht es kritisch

→ BIZ beweist (erneut), dass wir verdammt sind zur Politik billigen Geldes

Wobei nicht alle die BIZ so positiv sehen:

→ Die uneinsichtigen Starrköpfe der BIZ?

Heute nun eine erneute Warnung der BIZ. Diesmal hatte ich keine Zeit, die Vorabveröffentlichung der BIZ zu lesen, deshalb etwas verspätet und basierend auf der Zusammenfassung im Telegraph und bei Zero Hedge. Zunächst der Telegraph:

- “Central banks have reached exhaustion. Further monetary stimulus has little economic value at this juncture and ‘short-term turbo charges’ may be doing more harm than good, (…) zero rates and quantitative easing alone cannot deliver genuine growth, and the trade-off from asset booms is becoming ever harder to justify. Frothy forms of leverage akin to 2008 risk a cascade of fire sales in the next downturn.” – bto: Das Problem, was ich damit habe, ist folgendes: Dies alles kann sehen, wer es sehen will, und zwar schon sehr lange. Wieso also ist es so eine Überraschung, dass die BIZ es auch sieht. Ich denke, die erstaunliche Sache ist, dass die BIZ warnt, alle wissen, sie hat recht und keiner tut etwas gegen die Entwicklung.

- “Agustín Carstens, BIS general manager, said little would be achieved by another round of loosening by central banks in countries with interest rates already at rock-bottom levels. Yields on some $13 trillion of bonds are negative and the yield curve is close to inversion in a string of countries. (…) how much more stimulus will you get if interest rates are reduced in the margin another 25 basis points?” – bto: banal einleuchtend …

- “Over-reliance on monetary tools since the Lehman crisis has led to surging debt ratios and to forms of financial engineering that are in some cases as extreme or even worse than excesses seen in 2008. This edifice of leverage is inherently unstable and leaves the global financial system acutely sensitive to any tightening of conditions. The longer it goes on, the harder it is for the financial system to break free of debt addiction.” – bto: Auch das ist bekannt, was aber nichts an den fatalen Folgen dieser Politik ändert.” (…) the world’s $3 trillion leveraged loan market (…) – defined as loans to firms with debt over four times cash flow – accounted for half of publicly disclosed loan issuance worldwide in 2018 (excluding credit lines). The bulk was ‘cov-lite’ debt with minimal covenant protection for creditors. (…) collateralised loan obligations (CLOs) used to package leveraged loans can transmit tremors through the banking system (…)” – bto: Das ist nun wirklich nicht neu und wir befinden uns in einem unangenehmen Umfeld.

- Und dann kommt die BIS auch noch mit den BBB-Bonds um die Ecke, die bekanntlich einen Hauch vom Junk entfernt sind und eigentlich nach den harten Zahlen oftmals schon als solcher eingestuft sein müssten: “What worries the BIS is the fat cluster of BBB-rated bonds perched precariously just above junk status, up from 14pc to 45pc in Europe since 2000. A modest shock could push these high-debt firms into a downward spiral. Some funds would be forced by their mandates to liquidate holdings of these ‘fallen angels’.” – bto: auch bekannt und bei mir unter anderem in meiner WiWo-Kolumne diskutiert.

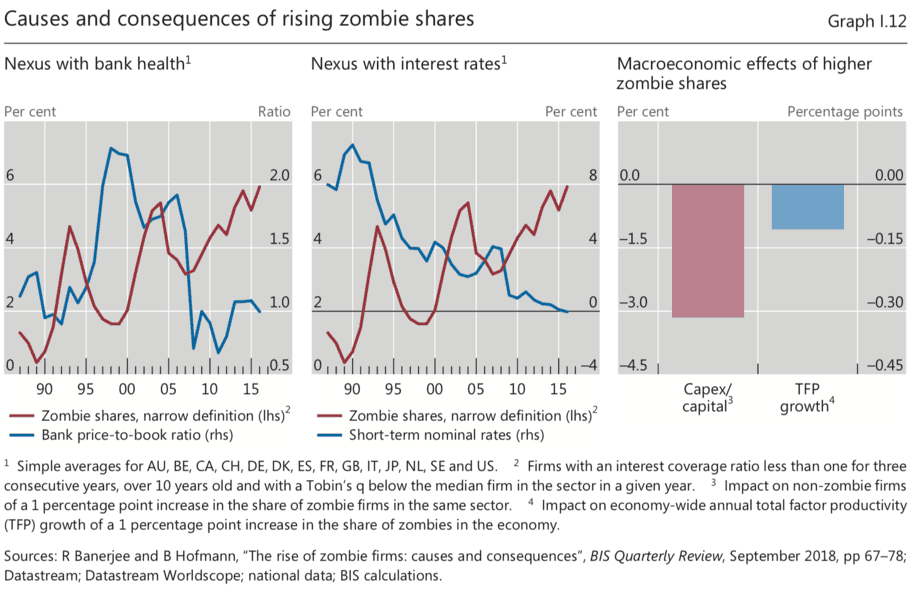

- Auch an die Zombies erinnert die BIZ erneut: “Struggling banks are one reason why productivity growth has wilted. Weak lenders are ‘more likely to evergreen loans or lend to zombie firms, thereby crowding out funding for new, more productive ones’. (…) This graveyard of ‘zombie firms’ – those that earn just enough to meet interest payments but cannot repay debt – has interfered with the Schumpeterian process of creative destruction, so vital to capitalist dynamism.” – bto: So ist es.

- “(…) a third of the world economy (…) are already tipping into a cyclical downturn. China stands out giant but Canada, Australia and Sweden are all over-stretched and at risk of a property slump. The US, UK, and parts of Europe are still far from the peak, although the debt-to-GDP ratio of US companies is even higher today (…) In the end it is the sheer scale of leverage across the world that leaves the vulnerable so sensitive to any upset. This time emerging markets cannot come to the rescue since they feasted on abundant dollar and euro liquidity during the QE heyday. It was hard for them to prevent excess capital flooding their economies.” – bto: Es sind die immer wieder dargelegten Zusammenhänge von hoher Verschuldung und dem Versuch, diese hohen Schulden mit noch mehr Schulden zu bekämpfen.

- Noch kurz die aktuellen Schuldenfakten: “The total non-financial debt ratio under the BIS measure has jumped from 107pc of GDP to 153pc over the past decade in developing economies. It has risen from 239pc to 265pc in advanced economies. France is up 74 percentage points to 311pc, Belgium up 45 points to 333pc, the Netherlands up 39 points to 331pc, and the UK up 30 points to 279pc.” – bto: Die Franzosen wissen schon, weshalb sie auf die Transferunion setzen …

Zero Hedge greift sich folgende Aspekte heraus:

- “One such vulnerability is high household debt in many advanced economies, especially those not directly affected by the Great Financial Crisis. These historically high debt levels limit the scope for households to drive economic activity.” – bto: Natürlich, Schulden sind vorweggenommener Konsum, das muss das Wachstum dämpfen.

- “Another vulnerability is clear signs of overheating in the corporate sector in a number of advanced countries. (…) There could be sharp price adjustments and funding tensions. These risks should be seen in the broader context of the longer-term deterioration in credit quality and the generally high corporate leverage in many advanced economies.” – bto: Auch dies habe ich schon oben und früher diskutiert. Es sind alles Zeichen für die zunehmende Verzerrung im System.

- “High levels of debt also point to vulnerabilities in a number of emerging market economies (EMEs). In some cases, these are in the household sector. Most often, they are in the corporate sector, not least as foreign currency debt has expanded strongly since the crisis. The current vulnerabilities reflect in part spillovers from prolonged accommodative monetary policies in advanced economies, as EMEs are especially vulnerable to capital flow reversals and exchange rate fluctuations.” – bto: Und ja, wir haben das Problem exportiert.

Hier noch die besten Charts aus dem Bericht:

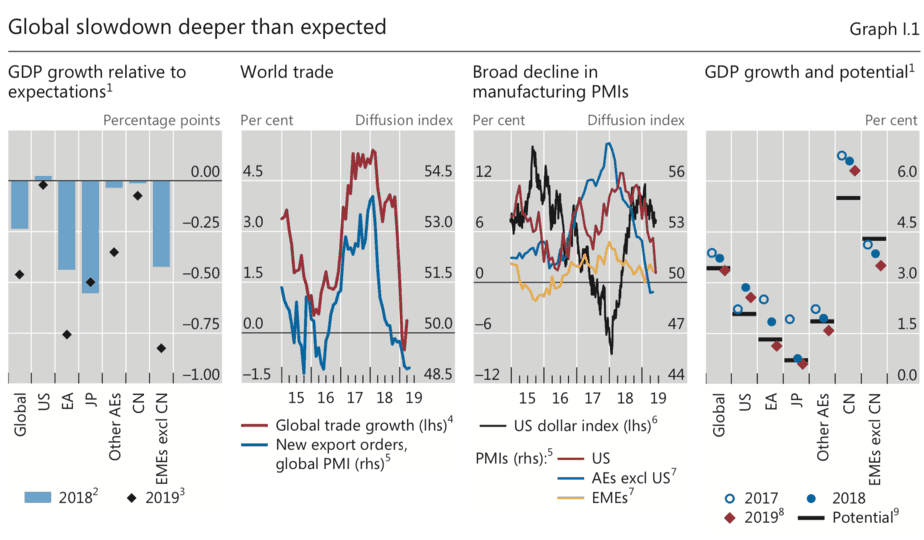

Zunächst die Erkenntnis, dass sich zumindest im ersten Halbjahr die Weltwirtschaft mehr als gedacht abgeschwächt hat:

Quelle: BIS

Quelle: BIS

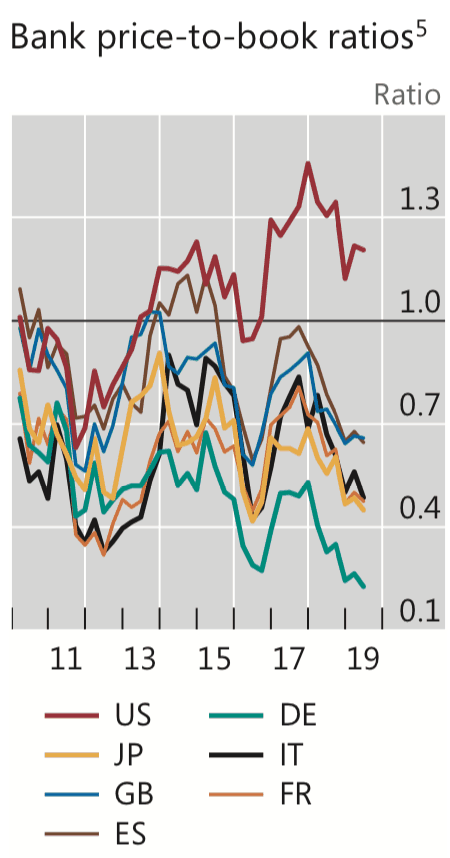

Dann als Auszug aus einem größeren Chart ein Blick auf die Bewertung von Banken. Deutschland ist superbillig – allerdings ist die Basis dafür auch sehr klein. Commerzbank und Deutsche Bank haben bekanntlich und offensichtlich ein Problem!

Quelle: BIS

Quelle: BIS

Dann die Daten zu der Verschuldung der Unternehmen:

Quelle: BIS

Nachdem die BIS auf das Prinzip des Recyclings setzt, zeigt sie auch noch mal das schöne Bild zu den Zombies, das ich bereits früher ausführlich diskutiert habe (siehe ganz oben in diesem Beitrag):

Quelle: BIS

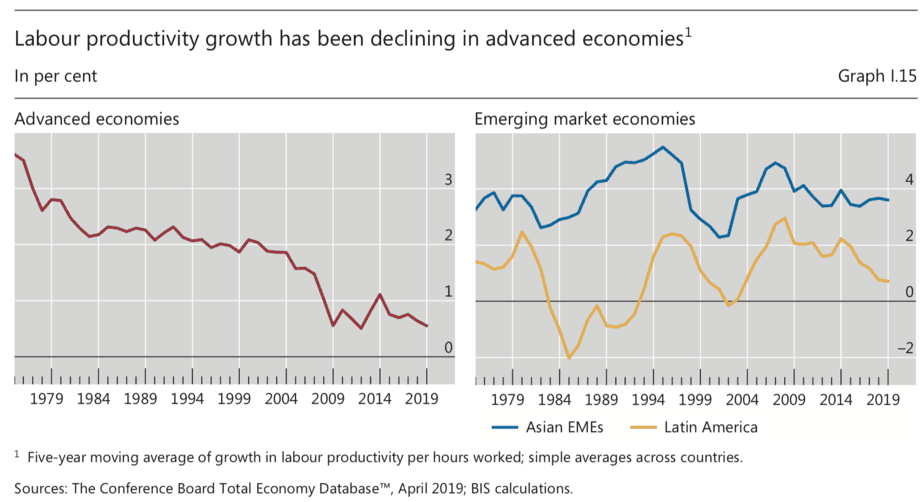

Was natürlich auch einer der Gründe für diese Entwicklung ist:

Quelle: BIS

Quelle: BIS

Was zur Eingangsfrage führt: Wenn die BIZ nun seit Jahren mit überzeugenden Argumenten warnt und zudem zu den wenigen gehört, die zutreffend vor der letzten Krise warnte, warum nimmt sie niemand ernst? Im Unterschied zu den Crash-Gurus, zu denen auch ich manchmal gezählt werde, wird sie wenigstens nicht verhöhnt.