Die Bären kommen zurück

Russell Napier habe ich auf bto mehrfach zitiert. In einem Blog wurden die Thesen Napiers zur Entwicklung von Bärenmärkten aus seinem Buch “Anatomy of a Bear Market” auf die aktuelle Situation angewendet. Eine angesichts der aktuellen Unsicherheiten lohnende Lektüre:

- „Every bear awakes from hibernation for different reasons. However, when studying the four great bottoms of bears in 1921, 1932, 1949, and 1982, there are several common traits to these horrendous cycles.” – bto: Ich denke aber, es sind nur Auslöser, nicht Ursachen. Die Ursachen sind immer zu hohe Bewertung und zu viel Liquidität.

- „Every financial crisis, market upheaval, major correction, recession, etc. all came from one thing – an exogenous, unanticipated, event. Such is why bear markets are always vicious, brutal, devastating, and fast. It is the exogenous event, usually credit-related, which sucks the liquidity out of the market causing prices to plunge. As prices fall, investors panic-sell driving prices lower. Such forces more selling in the market until, ultimately, it exhausts the sellers.“ – bto: immer wieder im Zusammenhang mit Margin Calls erläutert.

- „Throughout history, financial bubbles are only recognized in hindsight when their existence becomes ‘apparently obvious’ to everyone. Of course, by that point it was far too late to be of any use to investors and the subsequent destruction of invested capital. This time will not be different. Only the catalyst, magnitude, and duration will be. (…) therein lies the lessons from of the ‘Bear Market Anatomy’ and Russell Napier.“ – bto: Und ich würde sagen, wir sehen schon länger, dass der Markt „exhausted“.

Gehen wir Indikatoren durch:

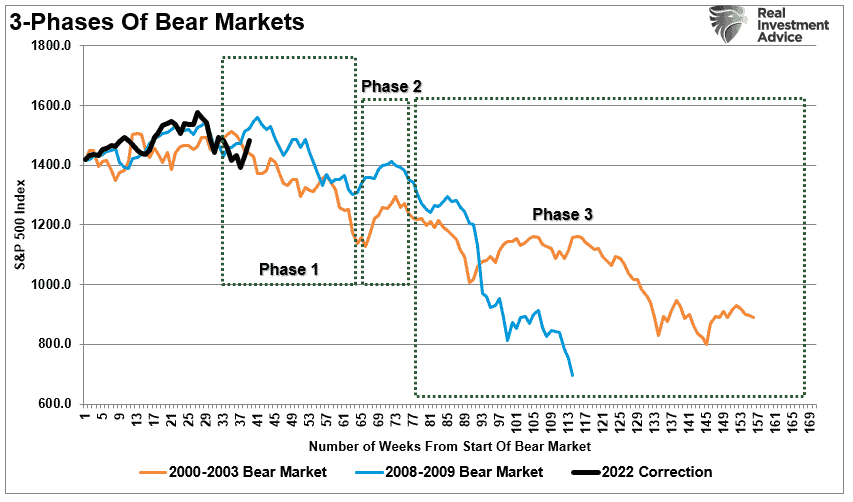

- “Bears Tend To Die On Low Volume

Low volume represents a complete disinterest in stocks. Keep in mind this contradicts the tenet, which states that bears end with one act of massive capitulation – a downward cascade on great volume. Those actions tend to mark the beginning of a bear cycle, not the end. A rise in volume on rebounds, falling volumes on weakness would better mark a bottoming process in a bear market.” Using that analysis, we can see volume did pick up during the recent decline. However, volume is far below the 2020 ‘bear market bottom,’ suggesting investors remain complacent.” – bto: Die Börsianer sind also noch zu ruhig. - “Bears Are Tricky

There will appear to be a recovery, an ‘all-clear’ for stock prices. It will suck investors back into the market, only to financially ravage them once again. Anecdotally, I know this cycle isn’t over as I still receive calls from people who are anxious to get into the market and perceive the current market a buying opportunity. At the bottom of a bear, I should hear great despair and a disdain for stock investing.” – bto: Mir hat gerade jemand von einem SPAC vorgeschwärmt. Ein klares Zeichen für ungebremsten Optimismus.

Quelle: RIA

- “Bears Can Be Tenacious

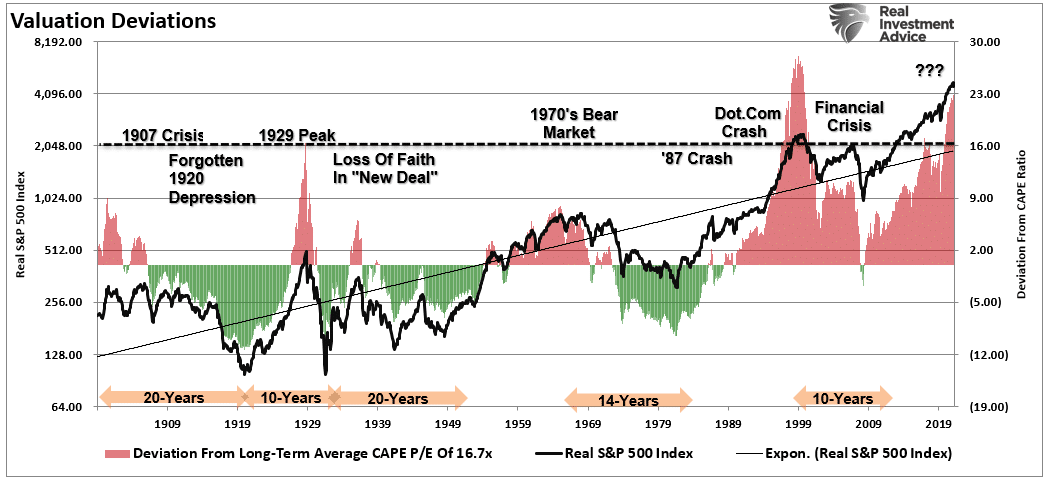

They refuse to die or, at the least, quickly return to hibernation. The 1921 move from overvaluation to undervaluation took over ten years. Bear markets, where three-year price declines make overvalued equities cheap, are the exception, not the rule. As of this writing, the Shiller P/E is at 35x – hardly a bargain. At the bottom market cycle of the Great Recession, the Shiller CAPE was at 15x. There is still valuation adjustment ahead.” – bto: immer unter der Annahme, dass wir uns in einem Bärenmarkt befinden. Ich fürchte, das tun wir. Die Risiken sind bei Weitem unterschätzt.

Quelle: RIA

- “Bears Can Depart Before Earnings Recover

Investors who wait for a complete recovery in corporate earnings will arrive late to the stock-investment party. Most likely, it will take a while (especially with the debt burden), for the majority of U.S. companies to reflect healthy earnings growth. (…) A savvy investor should look to minimize indexing, and select individual stocks with strong balance sheets, low debt, and plenty of free cash flow. A focus on sectors and industries that are nimble to adjust to the global economy post-crisis will be an added benefit.” – bto: Klar, man kann versuchen, die Ausnahmen zu finden. Das dürfte aber schwer sein, weil auch diese Art der Qualität nicht mehr billig ist. Einer Multiple-Compression werden sie sich nicht entziehen können. - “Bear Market Damage Can Be Inconceivable

The bear market of 1929-32 was characterized by an 89% decline. The average is 38% for bear markets; however, averages are misleading. I have no idea how much damage this bear ultimately unleashes. The closest comparison I have is the 1929-1932 cycle. However, with the massive fiscal and monetary stimulus, my best guess is a bear market contraction somewhere between the Great Depression and Great Recession. At the least, I believe we re-test lows, and this bear is a 40-45% retracement from the highs.” – bto: Wie gesagt, ich kann diese Aussage nicht beurteilen. Es ist aber sicherlich interessant, sich mit der Frage zu beschäftigen, ob wir angesichts des Umfelds mit einem entsprechend tiefen Einbruch rechnen müssen. - “Bear Markets End On The Return Of General Price Stability

In 1949, as in 1921 and 1932, a return of general price stability coincided with the end of the equity bear market. The demand for, and price stability of, selected commodities augured well for general price stabilization. Low valuations (not there yet), when combined with a return to normalcy in the general price level, may provide the best opportunity for future above-average equity returns. We are not there. With prices for commodities still spiking due to economic disruption, the bear market anatomy suggests that until those prices return to normal, the risk is not over.” – bto: Und wir wissen, dass wir erst am Anfang der Rohstoffpreis-Inflation stehen. - “Bear Markets That Don’t Decline On Bad News Is Positive

The combination of short positions in conjunction with a market that fails to decline on lousy news was overall a positive indicator of a rebound in 1921, 1932 and 1949. Also, limited stock purchases by retail investors may be considered an essential building block for a bottom.” – bto: Davon sind wir noch sehr weit entfernt. Die richtig schlechten Nachrichten müssen erst noch kommen und wirken.

Quelle: RIA

- “Not All Bear Markets Lead The Economy By 6-9 Months

Generally, markets lead the economy. However, this tenet failed to hold true for the four great bears. At extreme times, the bottoms for the economy and the equity market were aligned and in several cases, the economy LED stocks higher! It’s unclear whether this bear behaves similarly only because of massive fiscal and monetary stimulus. We’re not done with stimulus methods either. If anything, they’ve just begun!” – bto: Das wird allerdings mit der Inflation schwierig. Die Fed bereitet die Märkte bereits darauf vor, dass sie sich nicht um sie kümmern wird. Das gilt natürlich nur bis zu einem gewissen Maße. - „Don’t Discount The Bear Market Anatomy

Throughout history, individuals repeatedly jump into the more speculative stages of the financial market under the assumption that “this time is different.” Of course, as we now know with the benefit of hindsight, 1929, 1972, 1999, 2007, and 2020, were not different – they were just the peak of speculative investing frenzies. However, the massive surge in monetary and fiscal stimulus took market speculation to an entirely new level since the pandemic-driven lows.” – bto: Und wir erleben eine Zeitenwende. Diese wird nicht nur von der deutschen Politik voll erfasst, sondern auch an den Börsen unterschätzt. Letzteres dürfte sich eher ändern.