Der starke Dollar als Problem

Zunächst die Fakten:

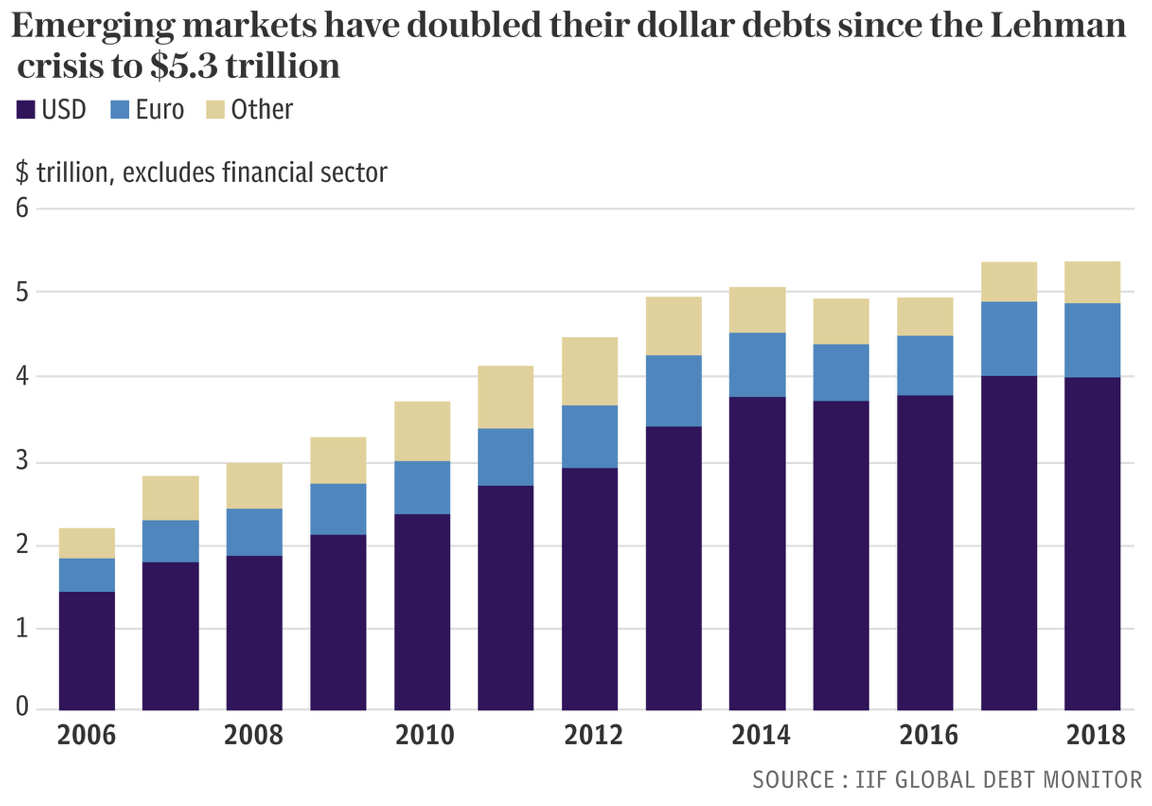

Quelle: The Telegraph

Quelle: The Telegraph

Die Aussage ist klar: Der Dollar ist so stark wie schon seit 15 Jahren nicht mehr: Ausfluss der besser laufenden Konjunktur der USA und den dort höheren Zinsen, aber auch Folge der zunehmenden Verknappung des US-Dollars. Im neuen wöchentlichen Newsletter des Telegraph diskutieren Ambroise Evans-Prithcard und Jeremy Warner die Implikationen für die Weltwirtschaft:

- “It is starting to look as if the dollar has metamorphosed into a petro-currency, logically since shale fracking has lifted US oil and gas production to top slot above Russia and Saudi Arabia. This has nasty consequences given the dollar’s other role as the anchor of international lending.” – bto: Für alle die in Dollar verschuldet sind, ist es ein Problem!

- The effect is to dial down the spigot of global liquidity, ultimately knocking away the central prop for this year’s 20pc rally in world equities. Achilles Heel No.1 in a strong-dollar world is emerging market debt. Leakage from QE and zero-rate policies in the West flooded these countries with irresistibly cheap dollar credit. Hard currency borrowing has risen from $2.2 trillion to $5.3 trillion over the last twelve years (…) This has reached 21pc of their collective GDP.” – bto: Das hatte ich oft bei bto und es kommt immer dann wieder hoch, wenn der Dollar neue Höchststände markiert. Es ist eine andere Ausprägung unserer Schuldenwirtschaft.

Quelle: The Telegraph

- “Achilles Heel No.2: the banking systems in Europe and Asia. These account for much of this dollar lending. They raise money on wholesale capital markets in London, Singapore, Hong Kong, et al, at short maturities (often 3-months) to lend worldwide.” – bto: was gefährlich ist, wie wir aus der Vergangenheit wissen!

- “This market froze in late 2008. European banks were suddenly $500bn short but their central banks could not print dollars to rescue them. The Fed saved the day with foreign currency swap lines.” – bto: Es ist auch das heißeste Geschäft, was man sich denken kann. Stellt sich die Frage, weshalb es die Banken trotz der historischen Erfahrung weitermachen. Besonders pikant diesmal: Es kann gut sein, dass die US-Fed nicht wie 2009 helfen darf, weil sich die US-Regierung querstellt. Denn ohne Zustimmung der Regierung darf die Fed ausländischen Instituten nicht helfen.

- “Achilles Heel No.3: crude oil. Barrels are priced in dollars. Brent at $75 is not as cheap as it looks for eurozone consumers. It is up by 60pc since mid-2017 when priced in euros and is again approaching levels that helped push Euroland into a manufacturing recession last year.” – bto: In der Tat führt der steigende Ölpreis zu steigenden Kosten, aber auch zu mehr Nachfrage nach US-Dollar.

- “(…) markets are not pricing in a US economic rebound. Futures contracts are discounting two Fed rate cuts this year. (…) the growth of final sales to US consumers, (slides) down to a 6-year low of 1.3pc. (…) Big Money funds think the world is a dangerous place: yes, the US has the worst economy, except for all the others. (…) The first sign of real trouble will precipitate a safe-haven scramble for scarce dollars. This will tighten global liquidity even further.” – bto: Allerdings wissen zu viele, dass es so nicht kommen darf, deshalb denke ich schon, dass koordiniert dagegen gearbeitet wird. Ob es genügt, kann ich allerdings nicht sagen.

Den Newsletter kann man hier bestellen (allerdings muss man Abonnent sein):

→ telegraph.co.uk: “Economic Intelligence”