Börsen: Ist der Zeitpunkt zum Einstieg gekommen?

Diese Frage bekomme ich in diesen Tagen immer wieder gestellt. Nun, ich bin kein Experte für Börsen und schon gar kein Hellseher. Deshalb kann ich das nicht sagen. Mein Naturell ist eher skeptisch – aber das dürfte Leser meiner Publikationen nun wirklich nicht wundern.

Deshalb behelfe ich mir mit John Authers, der bei Bloomberg einen sehr lesenswerten und unentgeltlichen Newsletter schreibt. Er bringt es in einem Kommentar zur Bewertung der US-Börse erneut durchaus gut auf den Punkt: Vorsicht bleibt angezeigt.

- “It is common to refer to any peak-to-trough fall of 20% as a ‘bear market’. I don’t know where this definition came from, and it isn’t terribly useful. But even if we accept it, it doesn’t follow that a 20% gain from the bottom, briefly made for the S&P 500, is a new bull market. It might be, but we can only tell in hindsight. If stocks go on to set a new high without revisiting their low, we might come to recognize that we are already in a bull market. Why doubt this? After big falls, big rebounds are to be expected. This chart compares the S&P 500 since its pre-Covid peak on Feb. 19 with its performance after Sept. 12, 2008, the last trading day before Lehman Brothers declared bankruptcy.” – bto: Das zeigt, dass es eben nicht risikofrei ist, und wer kann schon ausschließen, dass es doch noch zu neuen negativen Überraschungen kommt?

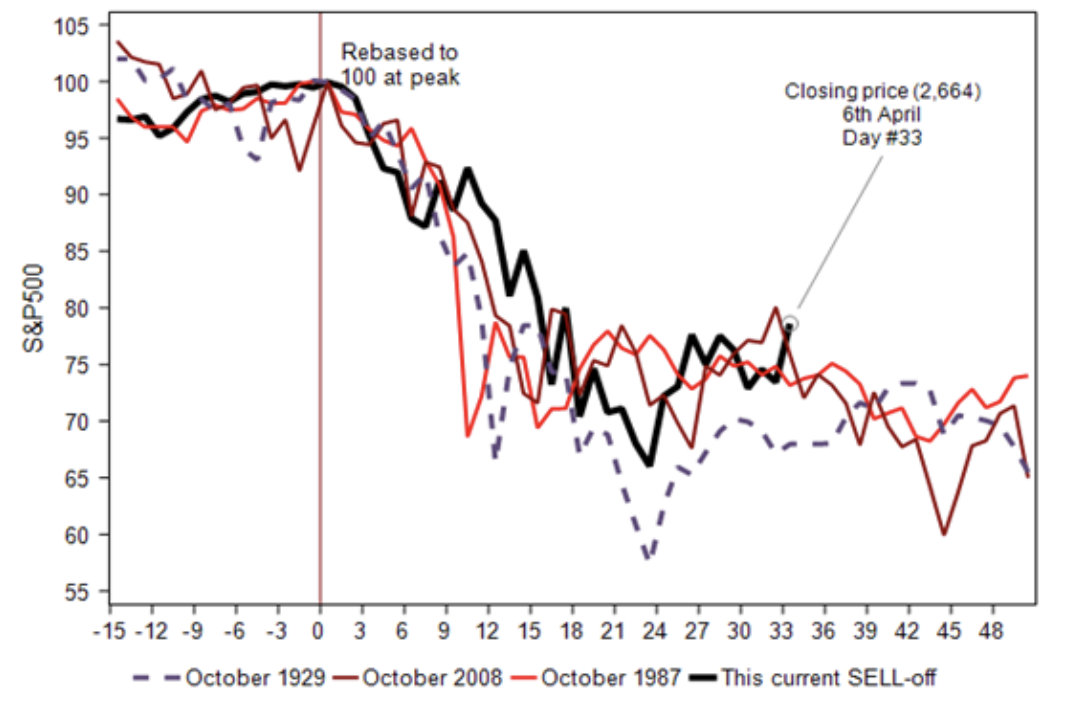

- “We are following that road map very closely — and back in 2008 there would be two new downdrafts, and two new lows, before the U.S. stock market bottomed for good in March 2009. (…) The following chart from Chris Watling of Longview Economics in London throws in the market’s behavior from the Great Crash of October 1929 and Black Monday in October 1987. The patterns are startlingly similar.” – bto: Natürlich ist es Kaffeesatzleserei, es einfach nur so zu vergleichen. Andererseits genügt es als Mahnung, dass es nicht so sicher ist mit einer Erholung vom heutigen Niveau.

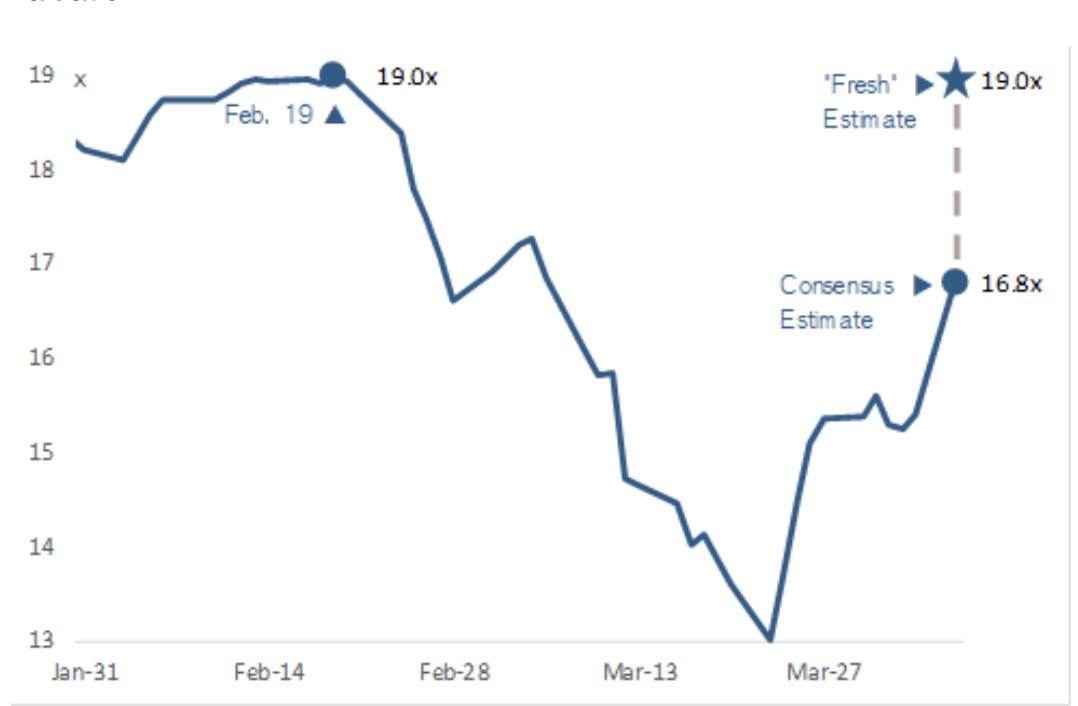

- “Another reason for caution comes from valuation. (…) if we use only estimates that have been revised in the last week, then prospective earnings multiples are already back to their Feb. 19 peak. Markets have effectively done nothing more than price in one set of bad earnings results, and returned to what already in February looked like a very expensive valuation.” – bto: Denn auch, wenn man es in Zeiten der Monetarisierung vergisst, Gewinne spielen bei Aktien eine Rolle. Und wenn die stark zurückgehen, woran kein Zweifel bestehen dürfte, muss auch der Preis der Aktie sinken.

- „Tackling this another way, look at trailing price-sales multiples. As of February, the S&P 500 was even more expensive than it had been at the top of the dot-com bubble in 2000. This reflected the belief that companies will continue to command higher profit margins — and thus justify a higher multiple of sales.“ – bto: Und genau das dürfte nicht der Fall sein. Ich habe ja in der letzten Woche schon die Studie besprochen, die gezeigt hat, dass die Reallöhne nach Pandemien steigen. Neben der De-Globalisierung der Wertschöpfungsketten dürften auch zunehmenden staatlichen Eingriffe die Kosten steigen lassen. Diese Kostensteigerungen können nicht voll über Preise weitergegeben werden, was die Margen unter Druck setzt.

- „The answer, then, appears to be that U.S. stocks aren’t in fact in another bull market. They have only been able to recover as much as they have because the extent of the long-term virus damage is still unclear and therefore unpriced. If lockdowns need to drag on and then be repeated two or three times, as many public health officials now suggest, the stock market will have to fall further.“ – bto: zumindest eine interessante Sicht. Ich denke auch, es ist zu früh, jetzt groß in die Märkte einzusteigen.

Grundsätzlichere Gedanken finden sich bei John Hussman:

“A share of stock is nothing but a claim on a very long-term stream of expected future cash flows that will be delivered into the hands of investors over time. If a security is expected to deliver a single $100 payment, a decade from today, the return that investors can expect is directly related to the price they pay.”

- Zahlt man heute 27 Dollar für eine Zahlung von 100 Dollar in zehn Jahren, entspricht das 14 Prozent jährlicher Verzinsung.

- Zahlt man 39 Dollar, ergeben sich zehn Prozent, bei 56 sechs Prozent und bei 82 Dollar zwei Prozent und bei 100 offensichtlich null.

Wenn die Preise sehr hoch sind, haben wir nicht nur eine erhebliche Anfälligkeit für höhere Renditeerwartungen, denn dann fallen die Kurse entsprechend schnell, sondern natürlich auch für Anpassungen am Endwert, zum Beispiel durch sinkende Gewinne wegen einer Rezession. Es braucht nicht viel, um heftige Kursverluste auszulösen. Das haben wir (erneut) gesehen.

- “As I noted in February, ‘I continue to expect the S&P 500 to lose about two-thirds of its value over the coming years. Avoiding profound market losses over the completion of this cycle would require a permanently high plateau in valuations, at their present hypervalued extremes, and the absence of even one episode of significant risk-aversion in the future.’” – bto: genau der Einbruch, der nun passiert ist.

- „Even if earnings are clobbered over the coming year, that’s a very small fraction of the entire stream.“ – bto: Das ist ein wichtiger Punkt, der natürlich dafür spricht, nach den deutlichen Verlusten über Käufe nachzudenken.

- Aber: “What’s likely to do harm to investors over the completion of this market cycle isn’t the impact of a year or two of lost cash flows. The likely source of actual damage is the roughly 65% loss in value (from the February high) that would be required simply to bring the most reliable valuation measures to their run-of-the-mill historical norms. The extreme financial valuations that preceded this crisis have made substantial additional stock market losses likely.” – bto: was zu der historischen Betrachtung von Authers passt.

- “The other source of potential disruption will be a certain amount of bankruptcy that was largely baked in the cake, as years of Fed-induced yield-seeking speculation enabled companies to issue a mountain of junky paper in the form of BBB bonds, leveraged loans, and covenant-lite debt.” – bto: Das stimmt, aber die Fed ist ja hier bereits eingesprungen und rettet – wie es in der FINANCIAL TIMES (FT) stand – jetzt Privat- Equity-Unternehmen und Spekulanten.

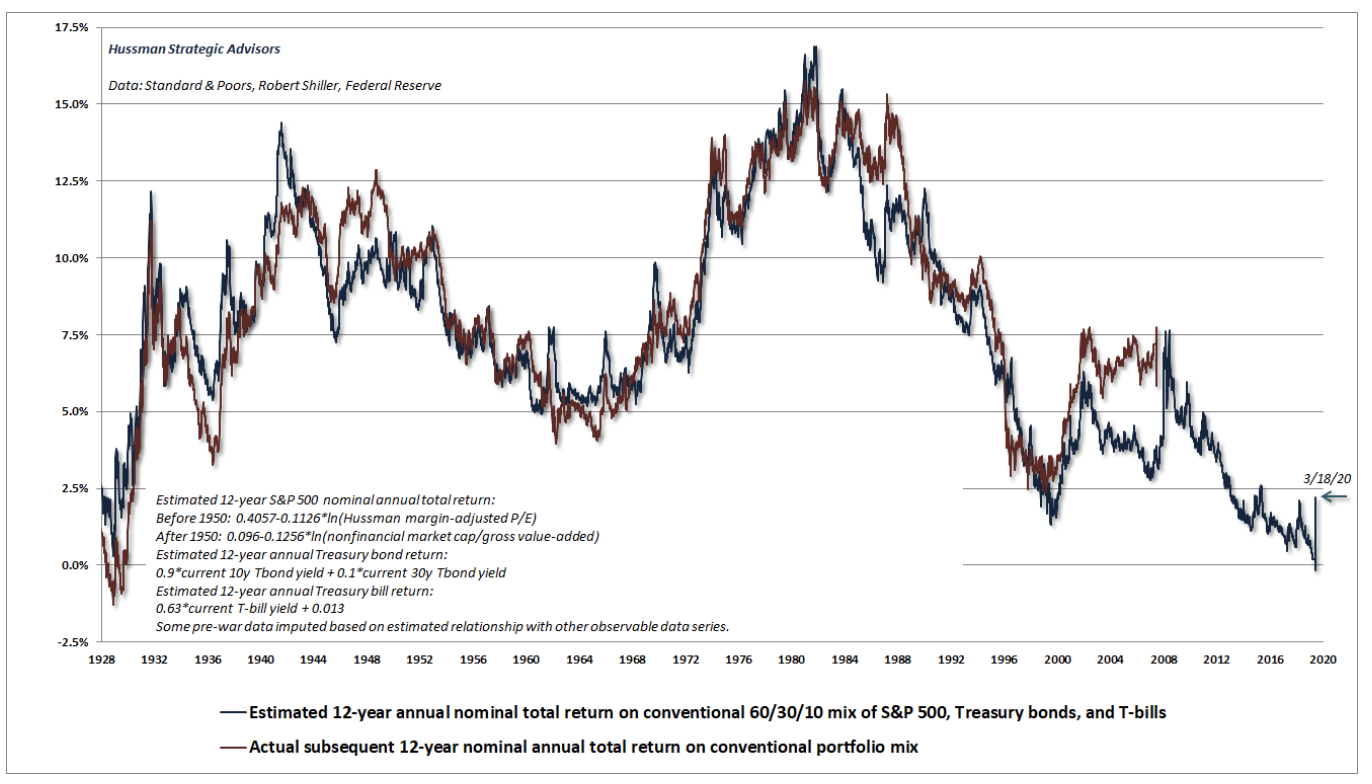

- “Valuations provide a great deal of information about long-term investment prospects, as well as the extent of potential market losses over the completion of a given market cycle. The chart below, for example, shows our estimate of likely 12-year average annual nominal total returns for a conventional portfolio mix invested 60% in the S&P 500, 30% in Treasury bond, and 10% in Treasury bills. I noted in mid-February that this estimate had declined below zero for the first time in history. Even the September 1929 market extreme did not do that. The little arrow at the right side of the chart shows the impact of the recent market selloff on these return prospects (as of 3/18/20 at about 2400 on the S&P 500).” – bto: Das Virus ist hier der Auslöser, aber wir sehen, dass wir von einem sehr hohen Niveau der Bewertung herkommen.

- “If you’re a long-term investor, the recent decline has pushed likely 10-12 year S&P 500 total returns back above zero. For investors who are comfortable with estimated 10-year SPX returns of about 1.4% annually, we’re here. While this estimate is better that the S&P 500 prospects we estimated, in real-time, at both the 2000 and recent February market extremes, S&P 500 valuations are presently similar to those at the 2007 market peak, and still far from what we’ve typically observed at cyclical lows. (…) The S&P 500 is currently at about the same level it was in January 2019. Though market valuations are about 24% lower than they were at the 2000 and February 2020 highs, they’re actually about the same level we saw at the October 2007 market peak, and still about double the historical norm.” – bto: Es rentiert sich, dies immer vor Augen zu halten. 1,4 Prozent lohnen das Risiko meines Erachtens noch nicht.

Damit spricht viel für eine zumindest vorsichtige Vorgehensweise.