BlackRock beweist: Alle, die sich mit der Materie auskennen, wissen, dass nur radikale Maßnahmen aus der Eiszeit führen

Viele meiner Leser wiesen mich auf dieses Paper und die begleitenden Pressestatements der Vertreter von BlackRock hin. Der weltgrößte Vermögensverwalter sorgte schon kürzlich für Aufmerksamkeit, als er in der FINANCIAL TIMES (FT) und in anderen Medien von der EZB forderte Aktien, aufzukaufen, um so die Wirtschaft vor Deflation und Rezession zu bewahren. Ein, wie ich an dieser Stelle feststellte, problematischer Vorschlag, der zudem das Geschmäckle hat, dass der Vermögensverwalter so kostenlos eine Absicherung seiner Position nach unten bekommt. Wirkung für die Realwirtschaft höchst zweifelhaft.

Doch kommen wir zu dem Paper, das den Titel „Dealing with the next downturn: From unconventional monetary policy to unprecedented policy coordination” trägt. Eine Frage, die – wie alle Leser von bto sehr gut wissen – erhebliche Relevanz hat. Doch was sind denn die revolutionären Ideen von BlackRock in einer Welt von Negativzins, lauten Helikoptergeräuschen und einer „Modern Monetary Policy“ (MMT), die, obwohl weder „modern“, noch „monetär“ von Ökonomen und Fachleuten – ich erinnere an Ray Dalio – gefeiert wird? Das schauen wir uns jetzt an:

- „After a decade of unprecedented monetary stimulus around the world, actual inflation and inflation expectations still remain stubbornly low in most major economies. (…) There are two potential reasons for why inflation is so low. First, the links between activity and inflation – the Phillips curve relationship – appears to have weakened in the post-crisis period. (…) Second, there is a self-fulfilling aspect to inflation: what people expect inflation to be in the future is a key driver of inflation today. (…) Other major economies start to look like Japan where years of weak growth and deflation were not countered sufficiently by monetary or fiscal policy – let alone both.” – bto: mag sein. Es könnte allerdings auch sein, dass die Zombifizierung einer zunehmend überschuldeten Welt das Realwachstum dämpft. Weniger Nachfrage und unzureichende Kapazitätsbereinigung führen zu einem deflationären Druck. Das dürfte hinter dem japanischen Szenario für alle stecken.

- „(…) central banks have pivoted towards lower rates and more stimulus, eroding the limited policy remaining even before the next downturn strikes. In the eurozone, this means the ECB is poised to go even more negative. Such a pre-emptive pivot to loosen policy – when the expansion is slowing but growth remains positive – reflects central banks’ concerns about the risks to growth, persistent inflation undershoots and their reduced room for policy manoeuvre. (…) 10 years into an expansion that was designed to restore the normal working of monetary policy, we are already eroding the limited policy space left.” – bto: Das hat eine offensichtliche und klare Ursache. Wir haben eine Krise, ausgelöst durch zu viele Schulden, mit noch mehr Schulden bekämpft und damit die Fallhöhe für die Fortsetzung der Krise erhöht.

- „The secular decline in neutral interest rates (…) has reduced the distance from the effective lower bound (ELB) and thereby how much the central bank can cut in a downturn. (bto: weshalb IWF & Co. jetzt ja das Bargeld abschaffen wollen, damit man es doch noch tiefer treiben kann.) (…) We believe this (…) reflects the role played by an increase in global risk aversion, (…) motivated persistently higher precautionary savings by both the public and private sectors, dragging down the neutral rate.” – bto: kein Wort zu dem offensichtlichen Thema: Wenn wir massiv neue Schulden machen und diese Schulden nichts anderes als neues Geld sind, muss der Preis des so massiv neu geschaffenen Geldes fallen. Das ist inhärent logisch und die Zinsen müssen sinken, weil sie schon tief sind. Ergo ist auch klar, dass es nur eine Lösung gibt: die Reduktion der Schulden!

- “Rising risk aversion also makes perceived safe assets more alluring and compresses their yields relative to other assets. This is why investors are pushing interest rates ever lower and flattening out yield curves. Nominal yields on long-term government bonds are at new record lows – the entire German bund yield curve is now negative – or back near historic ones in the US. The term premium – the compensation that investors typically demand for bearing the greater risk of long-term bonds – is negative again. Interest rates in Europe and Japan may already be near their ultimate floor as long as there is still physical cash.” – bto: Wer angesichts der demografischen Entwicklung in Deutschland die Staatsanleihen für risikofrei hält, muss fest mit der Monetarisierung rechnen. Alles andere ist Traumtänzerei.

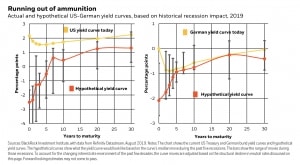

- “The chart on the left below shows the current US Treasury and German bund yield curves compared with a hypothetical one based on the median curve moves during the recessions of recent decades, adjusted for structural changes to neutral rates. (…) To get a similar move now, short-term rates would need to drop to around -2% in both countries.”

Quelle: BlackRock

- Und dann kommt die – nicht mehr so neue – Leier mit den Staatsausgaben. Die kommen doch auch, denn warum sonst wird es gerade unter dem Titel des Klimaschutzes vorbereitet? „Fiscal policy can do more heavy lifting when monetary policy alone is no longer enough. (…) The low interest rate environment increases fiscal space not only by making it cheaper to borrow, but also makes it possible for some governmentsto grow out of the increased debt.” – bto: und der nicht unbescheidenen Annahme, dass die Wachstumsprognosen der Ökonomen und Politiker besser sind als die in den Zinsen ausgedrückte Erwartung der Märkte.

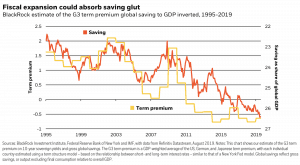

- Und man kann sich nach Auffassung von BlackRock ruhig auf dauerhaft tiefe Zinsen einstellen: “(…) the deep-rooted forces underlying the global saving glut will not change quickly on their own or will need material changes to be affected. (Schliesslich ist) Austria’s 50-year bond maturing in 2062 is one of the best performing financial assets this year.” – bto: Es ist ja auch völlig normal, dass man einem Land wie Österreich auf 100 Jahre Geld praktisch umsonst leiht …

- Allerdings meint auch BlackRock, dass die Gefahr besteht, dass seine (erfolgreiche) Fiskalpolitik das Geld dann doch teurer macht, was natürlich blöd wäre, würden doch dann die Anleihen im Kurs deutlich nachgeben: “(…) a significant increase in borrowing by governments globally could absorb part or all of this saving glut, pushing real interest rates towards or even above growth. The rise in public debt levels over the last four decades and the expansion of the welfare state (notably spending on retirement and health care) has been a meaningful force pushing neutral rates higher. Rachel and Summers (2019) estimate that higher public debt levelsalone have added 150 to 200 basis points to neutral rates, while the expansion of social welfare spending added another 250 basis points– preventing an even steeper fall in neutral rates.” – bto: Hier kommen Schulden vor, aber nur als Kostentreiber, nicht als Ursache.

Quelle: BlackRock

- “(…) high existing debt levels mean fiscal policy is vulnerable to even transitory interest rate spikes. Such a surge in rates could damage the fiscal policy space. This could arise from a so-called sudden stop: a temporary drying up of liquidity due to concerns about debt sustainability or losing reserve currency status. (…) Record debt levels might also stoke expectations that taxes will be raised, or benefits reduced, in the future. Such expectations could reduce current private sector spending and reduce the effectiveness of any public spending increase, a phenomenon known as Ricardian equivalence.” – bto: Klartext: Man kann sich als Politiker nicht darauf verlassen, dass die Märkte mitspielen.

- “Fiscal spending alone doesn’t guarantee an efficient or productive allocation of resources. (…) And austerity is not just a debate in some countries – deficit limits are hardwired into law in a number of countries.” – bto: Beides stimmt. Politiker dürften nicht die besten Investoren sein und in der Tat gibt es in einigen Ländern – wie Deutschland – entsprechende Begrenzungen. Also auch doof aus Sicht von BlackRock.

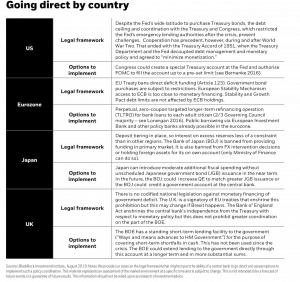

- “This means that in a downturn the only solution is for a more formal – and historically unusual – coordination of monetary and fiscal policy to provide effective stimulus. Already many of the monetary policy tools adopted since the crisis – QE including private sector assets – have fiscal implications. Special facilities such as the eurozone’s Outright Monetary Transactions (OMT) during the sovereign crisis also show how the central bank can throw its balance sheet behind fiscal solutions. Any additional measures to stimulate economic growth will have to go beyond the interest rate channel and ‘go direct’ – when a central bank crediting private or public sector accounts directly with money. One way or another, this will mean subsidising spending – and such a measure would be fiscal rather than monetary by design. This can be done directly through fiscal policy or by expanding the monetary policy toolkit with an instrument that will be fiscal in nature, such as credit easing by way of buying equities. This implies that an effective stimulus would require coordination between monetary and fiscal policy – be it implicitly or explicitly.” – bto: Also, das mit den Aktien lassen wir mal gleich weg, es bringt bekanntlich nichts. Ansonsten fordert BlackRock, was ich schon vor einigen Jahren gesagt habe: Gebt das Geld den Bürgern direkt. Natürlich wird man es lieber den Politikern geben, klar ist jedoch so oder so, dass wir es mit einer Politik zu tun bekommen, die das Geld nicht „kreditiert“, sondern verschenkt.

- “The most extreme case of monetary and fiscal coordination is pure monetary financing of government debt. That is, the central bank permanently increases its balance sheet to purchase government debt and facilitate the additional spending or directly inject money into the economy through a so-called helicopter drop. (…) We would highlight two key points on helicopter money. First, the fiscal expansion it represents – for example a tax rebate – needs to coincide with a boost in the stock of money. This ensures that any increase in interest rates is limited and there is no crowding out of private investment. Second, this boost to the stock of money has to be permanent. Otherwise, the money might not be spent if the increase is expected to be reversed in the future. If these conditions are met and helicopter money is delivered in sufficient size, it will drive up inflation – in the long run, the growth of money supply drives inflation.” – bto: Und das tut sie auch heute, siehe Assetpreise.

- “Monetary financing of fiscal expansion is not new – indeed it is as old as the first case of hyperinflation. (…) That highlights the main drawback of helicopter money: how to get the inflation genie back in the bottle once it has been released. (…) History as well as theory suggests large-scale injections of money are simply not a tool that can be fine tuned for a modest increase in inflation.” – bto: wie denn auch. Wenn die breite Bevölkerung merkt, dass die Nullen auf dem Bankkonto und die bunten Zettel quasi vom Himmel fallen, trauen sie dem Braten nicht mehr.

- “There is growing political discontent across major economies – and central banks are one of the targets. Widening inequality has fostered a backlash against elites. There are many drivers of inequality, including at its root technology, winner-take-all dynamics and globalisation. The GFC and the resulting forced bailout of financial institutions deemed too big too fail has added fuel to this backlash. Not acting during the GFC would have almost certainly led to a Great Depression-like outcome – much higher unemployment and even worse inequality. Yet that counterfactual provides no solace to those feeling left behind. And the monetary policy tools themselves might have increased inequality – and are certainly perceived to have done so – by pushing up the prices of assets owned by only a fraction of the population.” – bto: Hier stimme ich zu, wobei ich denke, dass die Krise eben aufgeschoben, nicht verhindert wurde.

- “A drift away from central bank independence – where the overall monetary policy stance is dominated by short-term political considerations – could quickly open the door to uncontrolled fiscal spending. The risk is real. This slippery slope leads to arguments that monetary policy can finance fiscal deficits – and that there is only a tenuous link between inflation and money-financed deficits, as some proponents ‘Modern Monetary Theory’ (MMT) claim.” – bto: wobei ich diese eben fast ehrlicher finde. Sie wollen das machen, was schon andere gemacht haben, mit dem Ziel, das Geld rasch zu entwerten und so das eigentliche Problem, die Überschuldung, zu lösen.

- “We believe a more practical approach would be to stipulate a contingency where monetary and fiscal policy would become jointly responsible for achieving the inflation target. To be sure, agreeing on the proper governance for such cooperation would be politically difficult and take time. That said, here are the contours of a framework:

- An emergency fiscal facility – that we refer to as the standing emergency fiscal facility (SEFF)– would operate on top of automatic stabilisers and discretionary spending, with the explicit objective of bringing the price-level back to target.” – bto: Ich nehme an, das ist als Notfall-Geldgeschenk an den Staat gedacht.

- “The central bank would activate the SEFF when interest rates cannot be lowered and a significant inflation miss is expected over the policy horizon.” – bto. genau. Wie unabhängig ist denn eine EZB unter Führung von Madame Lagarde?

- “The central bank would determine the size of the SEFF based on its estimates of what is needed to get the medium-term trend price level back to target and would determine ex ante the exit point. Monetary policy would operate similar to yield curve control, holding yields at zero while fiscal spending ramps up – see the yield at zero in the middle chart below.” – bto: selten so gelacht. Ex ante Austrittszeitpunkt! Klar, kennen wir ja schon als erfolgversprechendes Rezept. Der zweite Punkt hingegen ist entscheidend. Die Zinsen werden dann unten gehalten, um mit finanzieller Repression die Gläubiger zu enteignen/die Schulden zu entwerten.

- “The central bank would calibrate the size of the SEFF based on what is needed to achieve its inflation target.” – bto: Ich bin beeindruckt, was die von der Zentralbank so alles können (sollen). Ich denke, dies übersteigt die Fähigkeiten völlig und wird in das Desaster und somit zum Ende der „unabhängigen“ Zentralbanken führen.

- Mit MMT wollen sie dann aber doch nichts zu tun haben, obwohl es doch irgendwie so aussieht: “Our proposal stands in sharp contrast to the prescription from MMT proponents. They advocate the use of monetary financing in most circumstances and downplay any impact on inflation. Our proposal is for an unusual coordination of fiscal and monetary policy that is limited to an unusual situation – a liquidity trap – with a pre- defined exit point and an explicit inflation objective. Quasi-fiscal credit easing, such as central bank purchases of private assets, could be operated by the SEFF rather than the central bank alone to separate monetary and fiscal decisions.” – bto: alles klar. Die einen sagen von Anfang an, worauf das hinausläuft, bei den anderen werden es dann die Umstände erzwingen oder es läuft so aus dem Ruder. Das Ergebnis wird identisch sein.

- “Spelling out a contingency plan in advance would increase its effectiveness and might also reduce the amount of stimulus ultimately needed. As former US Treasury Secretary Henry Paulson famously said during the financial crisis: ‘If you’ve got a bazooka, and people know you’ve got it, you may not have to take it out.’” – bto. Und damit ist BlackRock bei Dalio und anderen, die wissen, dass a) die Schulden aus der Welt müssen, b) dies am schmerzfreiesten über Inflation geht c) und dass für sie persönlich dieser Weg der Beste ist, können sie doch damit umgehen.

Quelle: BlackRock

So, BlackRock reiht sich in den Chor jener, die das Heil in noch mehr Stimulus sehen. Dabei unterschlagen sie

- den Punkt der völlig aus dem Ruder gelaufenen weltweiten Verschuldung als Ursache der Probleme;

- erwähnen den Punkt der abnehmenden Produktivität neuer Schulden mit keinem Wort;

- gleiten elegant über den Punkt hinweg, dass in Japan seit Jahren erhebliche Staatsdefizite faktisch von der Bank of Japan finanziert werden, ohne den gewünschten Erfolg zu haben;

- die demografische Entwicklung;

- die schlechte Entwicklung der Produktivität, die auch hinter dem geringen Wachstum steht.

In Wahrheit ist es doch so: Wir stehen vor der größten deflationären Schuldendeflation der Geschichte. Das ist ein Albtraum, aber die logische Folge der jahrzehntelangen Misswirtschaft. Sichtbar an immer höheren Schuldenständen bei abnehmender realwirtschaftlicher Wirkung und immer weiter von der Realwirtschaft entfernten Vermögenspreisen. In der verzweifelten Suche nach einem Ausweg gehen wir “all-in”. Ob es genügt? Ich denke, nur, wenn wir die Hyperinflation erzeugen, die sich alle (heimlich) wünschen.