“A Warning About Chasing This Bull Market”

Letzte Woche besprach ich die Studie, die zeigt, dass die US-Börse von den fundamentalen Fakten getragen ist und man sich demzufolge keine Sorgen machen soll. Solange die Gewinnquoten hoch bleiben, ist alles o. k. Hohe Bewertungen auf hohen Gewinnquoten hängen miteinander zusammen und da nicht abzusehen ist, dass sich an den Gewinnquoten, getragen von Superstar-Firmen und Monopolisierung, etwas ändert, ist keine Änderung der Lage zu befürchten.

Dennoch gibt es auch weiterhin mahnenden Stimmen. So hier:

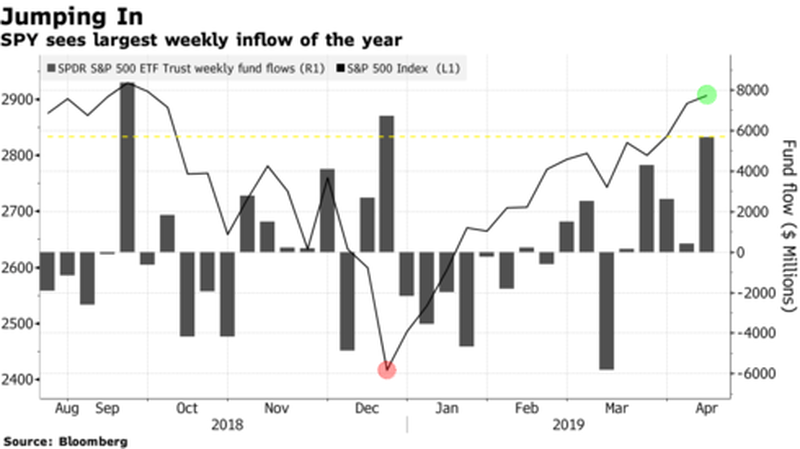

Zunächst die offensichtliche Feststellung, dass es wieder Party-Time ist: “investors are currently rushing to get back into the market, after bailing out in December, with a near reckless disregard for the consequences.” – bto: was dann schön mit den Zuflüssen in Indexfonds unterstrichen wird. Wobei man sagen muss, dass sie auch Ende Dezember gekauft haben und im März verkauft. Vermutlich wird hier etwas mehr hineininterpretiert, als man wirklich sehen kann.

Quelle: Real Investment Advice

Schauen wir uns an, welche Indikatoren Sorgen bereiten könnten:

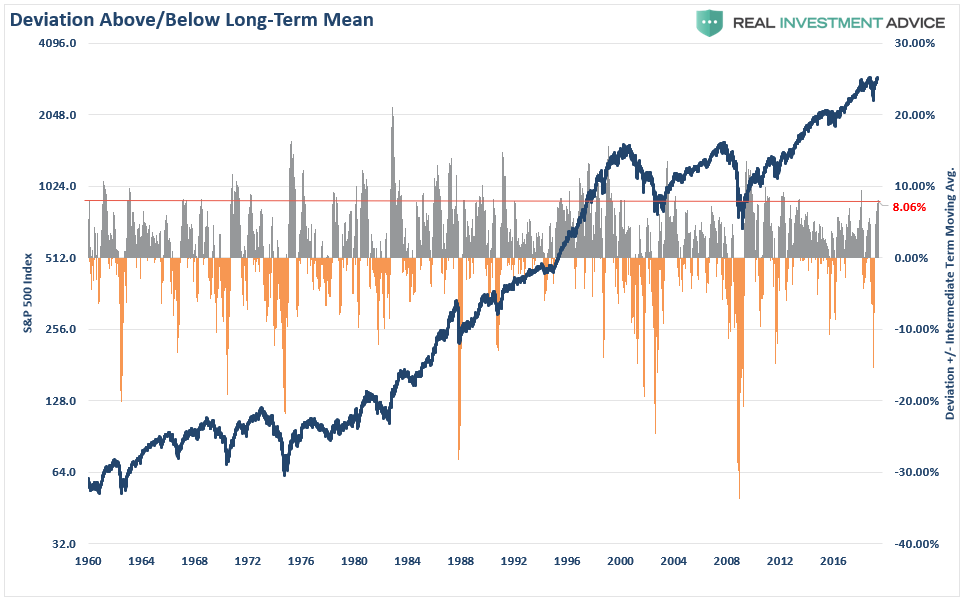

Warnzeichen Nr. 1: Die Abweichung vom Durchschnitt

- “(…) in investing, prices must be both above and below the ‘average price’ over a set period of time for there to be an average. To many degrees ‘price’ is bound by the laws of physics, the farther from the ‘average price’ the current price becomes, the greater the pull back to, and generally beyond, the average. (…) Currently, the market is more than 8% above its longer-term daily average price. These more extreme deviations tend not to last an extraordinarily long time. Furthermore, reversions from these more extreme deviations tend to be rather quick.” – bto: oder auch nicht. Wir wissen, dass die Märkte länger abweichen können. Dennoch hier die dazugehörige Abbildung:

Quelle: Real Investment Advice

Quelle: Real Investment Advice

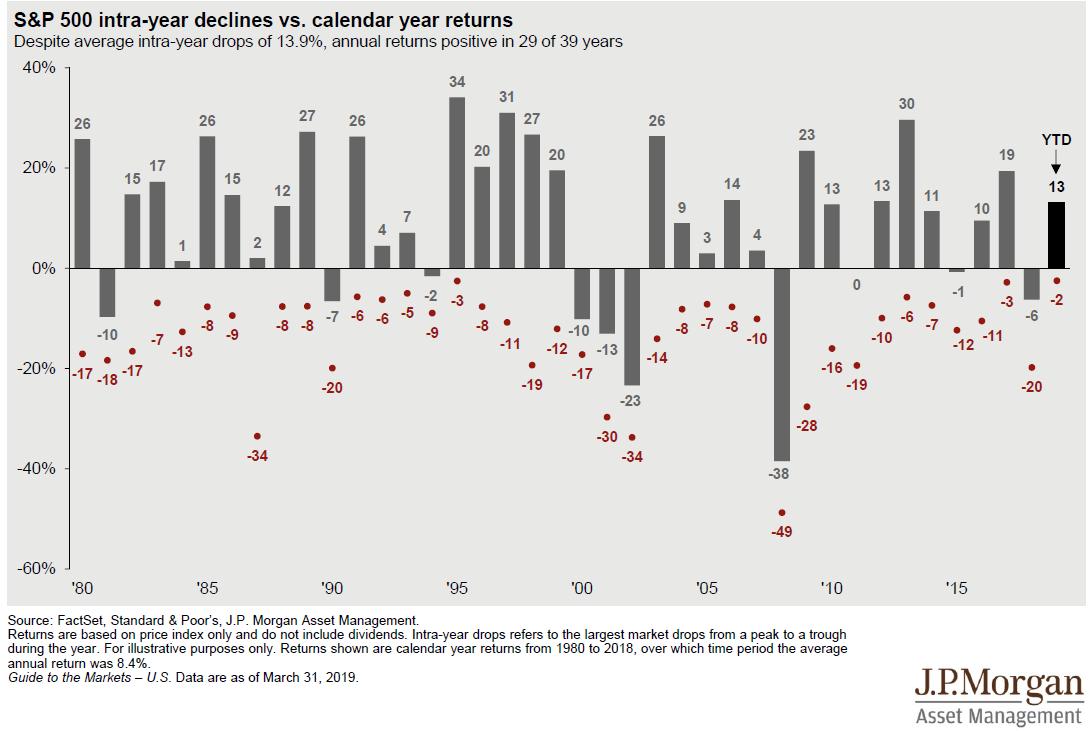

- “Currently, investors have become extremely complacent with the rally from the beginning of the year and are quick extrapolating current gains through the end of 2019. As shown in the chart below this is a dangerous bet. In every given year there are drawdowns which have historically wiped out some, most, or all of the previous gains. While the market has ended the year, more often than not, the declines have often shaken out many an investor along the way.” – bto: Auch ohne einen Crash ist der Mark erfahrungsgemäß keine Einbahnstraße.

Quelle: Real Investment Advice

Quelle: Real Investment Advice

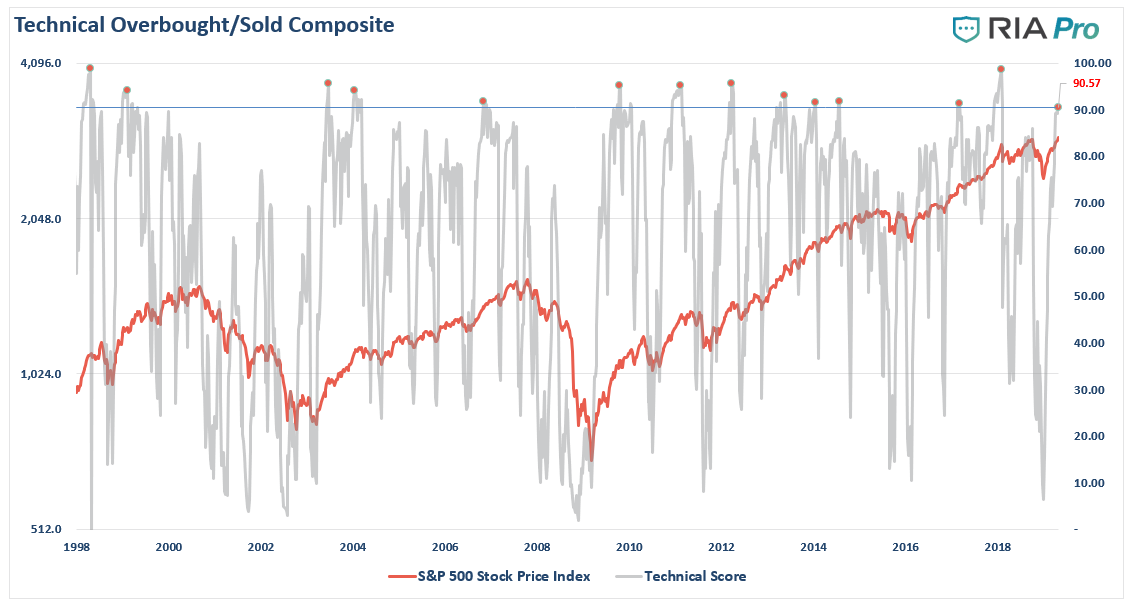

Warnzeichen Nr. 2: Markttechnik

- “Currently, the overbought condition of the market is near points which have denoted more significant corrections.” – bto: In der Tat sind solche Analysen gut geeignet, um Wendepunkte vorherzusagen. Wenn alle investiert sind, fehlen per Definition die Käufer.

Quelle: Real Investment Advice

- “The market/sector analysis shows the rather extreme price deviation in Technology, Discretionary, and Financials. Also, relative performance shows that it has primarily been Technology and Real Estate providing a bulk of the ‘alpha’ year-to-date.” – bto: Diese Sektorkonzentration haben wir auch im letzten Jahr gesehen, am Ende mit einer extremen Fokussierung auf die FANGs. Dies ist ebenfalls zumindest ein Warnsignal.

Quelle: Real Investment Advice

Warnzeichen Nr. 3: Dollarstärke

- “When the Fed embarked on QE, they wanted to ensure that the money created to buy Treasuries and mortgages was being held by the banks as excess reserves and not being used to form loans. (…) To help them keep the money on the sidelines and better control the Fed Funds rate, the Fed decided to pay banks interest on excess reserves (IOER). The IOER rate was set above the Fed Funds rate (the rate banks lend reserves to other banks on an overnight basis). The thought being that banks would rather collect a higher interest rate and take no risk than lend out money to other banks at a lower interest rate. (…) The IOER premium over Fed Funds served its purpose in keeping excess reserves constant and in capping the Fed Funds rate from 2011 to 2017. However, as shown below, its effectiveness started eroding with the advent of QT in October of 2017.” – bto: Das war mir in diesem Zusammenhang noch nicht bekannt. Wir haben also als Ergebnis sichere Erträge der Banken. Doch wenn das nun nicht mehr gebraucht wird, wo liegt das Problem?

- Die Antwort kommt hier: “We believe the liquidity drain associated with QT created a shortage of dollars among foreign banks. (…) Regardless of the reasons, a dollar shortage can become a dollar crisis if not addressed.

Warnzeichen Nr. 4: Gewinne

Die Aussage ist klar: Obwohl die Unternehmen immer noch die Vorhersagen “schlagen”, tun sie dies nur noch, weil zuvor die Erwartungen gesenkt wurden. Die Gewinne stagnieren oder sind bereits rückläufig, wenn man genauer hinschaut.

Alles kein Grund zur Panik, aber zur Vorsicht schon.