Best-of bto 2019: Wie endet die Schuldenblase? Inflationär, deflationär, geordnet?

Wenn man erkannt hat, dass wir uns dem Ende einer jahrzehntelangen Schuldenorgie nähern, in der wir Konsum vorgezogen und heftig spekuliert haben, ist die Frage nach dem „Was-nun?“ nur konsequent. Und dieses „Was-nun?“ ist dann auch relevant für die geeignete Lösung, mögliche Szenarien und damit auch für die richtige Strategie, um mit seinem Vermögen darauf zu reagieren, siehe “Eiszeit in der Weltwirtschaft”. Deshalb Martin Wolf von der FINANCIAL TIMES (FT). Ein unstrittig heller Kopf, der aber letztlich auch nur die Szenarien beschreiben und seiner Hoffnung Ausdruck verleihen kann:

- “Some warn that the world of high debt and low interest rates will end in the fire of inflation. Others prophesy that it will end in the ice of deflation. Others, such as Ray Dalio of Bridgewater, are more optimistic: (…) it will be neither too hot nor too cold, (…) at least in countries that have had the fortune and wit to borrow in currencies they create freely.” – bto: Letzteres bedeutet eine andere Art der Entwertung von Schulden und Forderungen. Wenn es stimmt, befinden wir uns im Euroraum, wie auch von mir immer wieder beschrieben, in einer wenig komfortablen Lage. Wir müssen 19 Länder unter einen Hut bringen und es wird eine Weile dauern, bis die deutsche Regierung einer Monetarisierung – und um die geht es auch Dalio – zustimmen wird. Und wohl noch länger werden wir darauf warten müssen, dass wir den Blödsinn der „schwarzen Null“ aufgeben.

- “William White, former chief economist of the Bank for International Settlements, presciently warned of financial risks before the 2007-09 financial crisis. (…) warned of another crisis, pointing to the continuing rise in non-financial sector debt, especially of governments in high-income countries and corporations in high-income and emerging economies. Those in emerging countries are particularly vulnerable, because much of their borrowing is in foreign currencies.” – bto: Und White ist sicherlich der smarteste. Hier ein paar seiner Beiträge auf bto:

→ William White sah es damals kommen – und warnt weiterhin

→ „William White: ‚Notenbanken können nicht zurück‘“

→ „Ultra Easy Monetary Policy and the Law of Unintended Consequences“

- Zunächst das Szenario Inflation: “Much of what is going on right now recalls the early 1970s: (…) a long period of stable and low inflation has calmed fears of an upsurge, even though unemployment has fallen to low levels. [In the US, it is at its lowest level since 1969.] Some suggest that the Phillips curve — the short-term relationship between unemployment and inflation — is dead, because low unemployment has not raised inflation. More likely, it is sleeping. (…) In some ways, a rise in inflation would be helpful. A sudden jump in inflation would reduce debt overhangs, notably of public debt, just as the inflation of the 1970s did.” – bto: das sicherlich. Die Frage ist, ob der Vergleich passt. Damals hatten wir nicht den enormen Schuldenüberhang wie heute. Zwar waren auch damals Assets teuer, aber längst nicht so teuer wie gegenwärtig. Insofern ist es schwieriger, Inflation zu erzeugen.

- Aber selbst die Inflation wäre nicht so schmerzfrei wie erhofft: “Yet higher inflation would also lead to a rise in long-term nominal interest rates, which tend to front-load the real burden of debt service. Short-term rates would also jump as they did in the early 1980s. Risk premia would rise. High-flying stock markets might collapse. Labour relations would become more strife-prone, as would politics. This disarray would hit unevenly, causing currency disorder. The loss of confidence in public institutions, notably central banks, would be severe. In the end, the likely stagflation would end in severe recession, as in the 1980s.” – bto: Das unterstreicht, dass die Inflation nicht schmerzfrei ist. Vermutlich würde sie den ohnehin bestehenden Trend gegen das Kapital und die Besitzenden verstärken.

- Nun zur Deflation (was wohl eher eine deflationäre Depression wäre): “This might begin with a sharp negative economic shock: a worsening trade war, a war in the Middle East or a crisis in private or public finance, possibly in the eurozone, where the central bank is relatively constrained.” – bto: So ist es. Gerade bei uns braut sich das größte Problem zusammen aus einer Kombination einer dysfunktionalen Währungsunion, schlechter Demografie und noch schlechterer Politik.

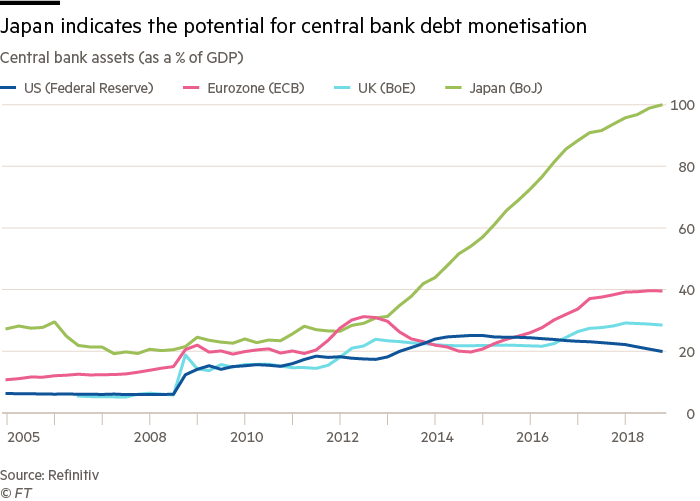

- “The result could be a deep recession, even a lurch into deflation, so worsening the debt overhang. The big difficulty would be knowing how to respond given that interest rates are already so low. Conventional policy (lower short-term rates) and conventional unconventional policy (asset purchases) might be insufficient. A range of other possibilities exist: negative rates from the central bank; lending to banks at lower rates than the central bank pays on their deposits (was nichts anderes al seine Subvention der Banken ist, kann man auch einfacher und effizienter organisieren); purchase of a much wider range of assets, including foreign currencies; monetisation of fiscal deficits; and ‚helicopter drops‘ of money.” – bto: Ich denke, wir werden all dies erleben. Ich bin, vor die Wahl gestellt, mehr bei dem Deflationsszenario. Und die Instrumente werden schon vorbereitet.

Quelle: FT

- “Much of this would be technically or politically problematic, and would require close co-operation with the government. Meanwhile, if governments acted too slowly (or not at all) a depression might ensue, as in the 1930s, via mass bankruptcy and debt deflation.” – bto: Ich denke, wir laufen in Europa ernsthaft in die Gefahr. Generell dürfte es aber so radikale Monetarisierung mit sich bringen, dass wir die Chance haben, dass es nicht so schlimm wird, wie in den 1930er-Jahren.

- “Mr Dalio argues, a golden mean is possible. Fiscal and monetary policy would then co-operate to generate non-inflationary growth. Changes in fiscal incentives would discourage debt and encourage equity. Government policy would shift income towards spenders, reducing our current reliance on debt-fuelled asset bubbles for sustaining demand. (…) Even if real interest rates rose, perhaps because productivity growth strengthened durably, the impact of robust non-inflationary growth on the debt burden would almost certainly outweigh a move to somewhat higher interest rates.” – bto: Ja, wer wünscht sich das nicht. Mehr Umverteilung hilft (in Ländern wo diese noch nicht funktioniert, wie in den USA), die Idee Eigenkapital besserzustellen und Schulden weniger attraktiv zu machen, bringt Assetpreise unter Druck und damit Schuldner. Gefährlich und deshalb unwahrscheinlich vor der Bereinigung. Danach eher. Woher das Produktivitätswachstum jetzt kommen soll, ist mir nicht klar.

- “We would (…) be moving out of ‚secular stagnation‘ into something less bad. That shift might be tricky. But it would be to a better world. It is not necessary to repeat the mistakes of either the 1930s or the 1970s. But we have made enough mistakes already and are, collectively, making enough more right now to risk either outcome, possibly both. A breakdown of the global economic and political order seems conceivable. The impact on our debt-encumbered world economy and increasingly fraught global politics is impossible to calculate. But it could be horrendous.” – bto: So ist es. Bleibt der Eindruck, dass Martin Wolf – wie jeder vernünftig denkende Mensch – auf Szenario 3 hofft, es aber nicht für das Wahrscheinlichste hält. Da geht es ihm dann so wie mir.