Wie 1982 – nur mit negativem Vorzeichen

In der vergangenen Woche hat sich mit dem Hedgefonds-Manager Stan Druckenmiller, einer der berühmtesten Vertreter der Finanzmärkte (hat mit Soros damals gegen das englische Pfund spekuliert), sehr kritisch zu Wort gemeldet. Mittlerweile sind Redetext und Folien frei verfügbar:

Der Titel seiner Präsentation lautet: „The Endgame“. Ich zeige hier nur eine Auswahl, die aber genügt um Druckenmillers Beschreibung der Eiszeit zusammenzufassen.

Zunächst erinnert er daran, dass das Umfeld an den Kapitalmärkten sich deutlich geändert hat: „… in February of 1981, the risk free rate of return, 5 year treasuries, was 15%. Real rates were close to 5%. We were setting up for one of the greatest bull markets in financial history as assets were priced incredibly cheaply to compete with risk free rates and Volcker’s brutal monetary squeeze forced much needed restructuring at the macro and micro level. It is not a coincidence that strange bedfellows Tip O’Neill and Ronald Reagan produced the last major reforms in social security and taxes shortly thereafter. Moreover, the 15% hurdle rate forced corporations to invest their capital wisely and engage in their own structural reform“.

„If this led to one of the greatest investment environments ever, how can the mirror of it, which is where we are today, also be a great investment environment? Not a week goes by without someone extolling the virtues of the equity market because ‚there is no alternative‘ with rates at zero. The view has become so widely held it has its own acronym, ‚TINA‘.“

Quelle: Druckenmiller

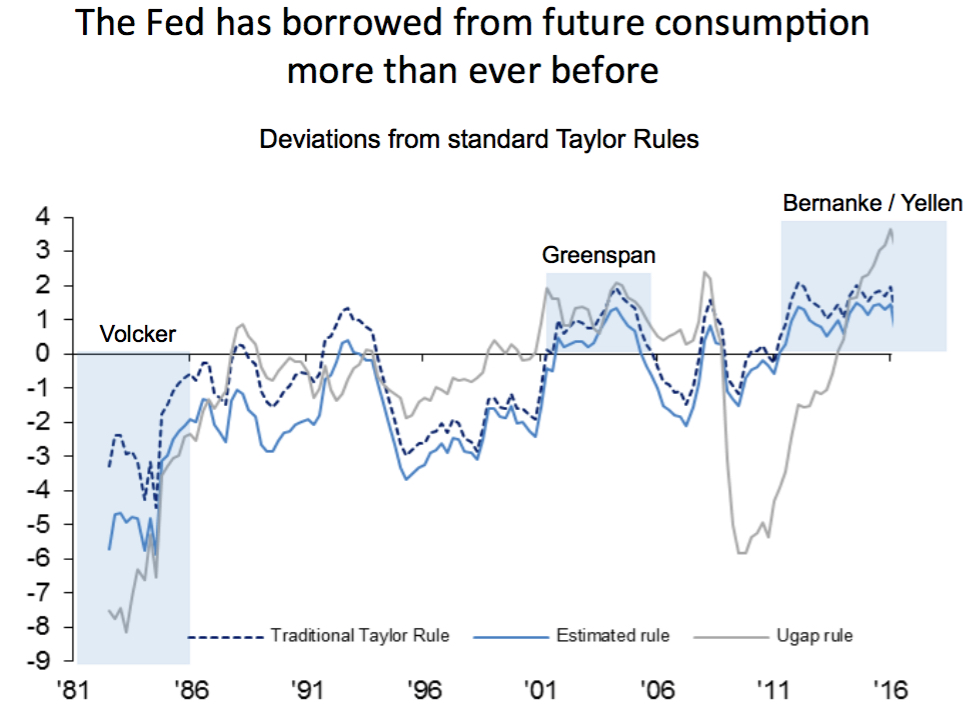

Als die unweigerliche Krise in Folge der parallel massiv gestiegenen Verschuldung – dem Leverage im System, den auch ich immer wieder anspreche und deshalb nicht erneut zeige – griff die Fed ein, um ein Desaster zu verhindern: „By most objective measures, we are deep into the longest period ever of excessively easy monetary policies. During the great recession, rates were set at zero and they expanded their balance sheet by $1.4T. More to the point, after the great recession ended, the Fed continued to expand their balance sheet another $2.2T. Today, with unemployment below 5% and inflation close to 2%, the Fed’s radical dovishness continues. If the Fed was using an average of Volcker and Greenspan’s response to data as implied by standard Taylor rules, Fed Funds would be close to 3% today. In other words, and quite ironically, this is the least “data dependent” Fed we have had in history. Simply put, this is the biggest and longest dovish deviation from historical norms I have seen in my career. The Fed has borrowed more from future consumption than ever before“.

Quelle: Druckenmiller

Das zeigt sich dann übrigens in der Performance an den Kapitalmärkten. Sowohl in den USA wie auch in Europa sind vor allem die Bewertungen gestiegen, während die Gewinne schon seit Jahren rückläufig sind. Hatte ich bei bto schon gezeigt, deshalb hier von Albert Edwards das entscheidende Bild dazu:

Quelle: Albert Edwards

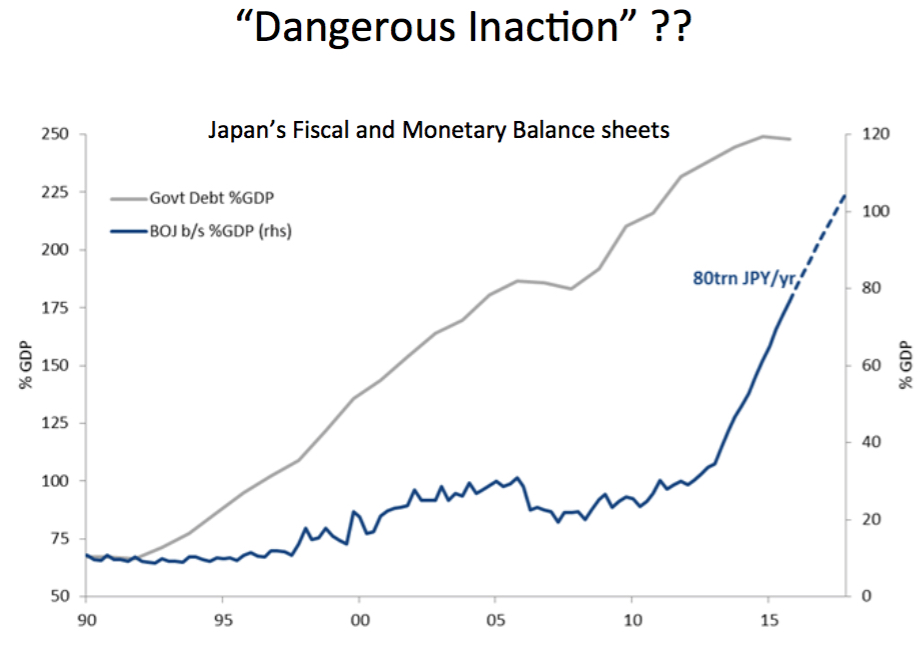

Doch damit nicht genug: „But the sub-par economic growth we are experiencing in the 8th year of a radical monetary experiment and in Japan after more than 20 years has blown that theory out of the water. And smoothing growth over a cycle should not be confused with consistently attempting to borrow consumption from the future. The Fed has no end game. The Fed’s objective seems to be getting by another 6 months without a 20% decline in the S&P and avoiding a recession over the near term. In doing so, they are enabling the opposite of needed reform and increasing, not lowering, the odds of the economic tail risk they are trying to avoid. At the government level, the impeding of market signals has allowed politicians to continue to ignore badly needed entitlement and tax reform.“ – bto: wie bei uns!

„While the debt in the 1990’s financed the construction of the internet, most of the debt today has been used for financial engineering, not productive investments. This is very clear in this slide. The purple in the graph represents buybacks and M/A vs. the green which represents capital expenditure. (…) Last year, buybacks and M&A were $2T. All R&D and office equipment spending was $1.8T. And the reckless behavior has grown in a non-linear fashion after 8 years of free money. In 2012, buybacks and M&A were $1.25T while all R&D and office equipment spending was $1.55T. As valuations rose since then, R&D and office equipment grew by only $250b, but financial engineering grew $750b, or 3x this! (…) The corporate sector today is stuck in a vicious cycle of earnings management, questionable allocation of capital, low productivity, declining margins, and growing indebtedness. And we are paying 18X for the asset class.“

Quelle: Druckenmiller

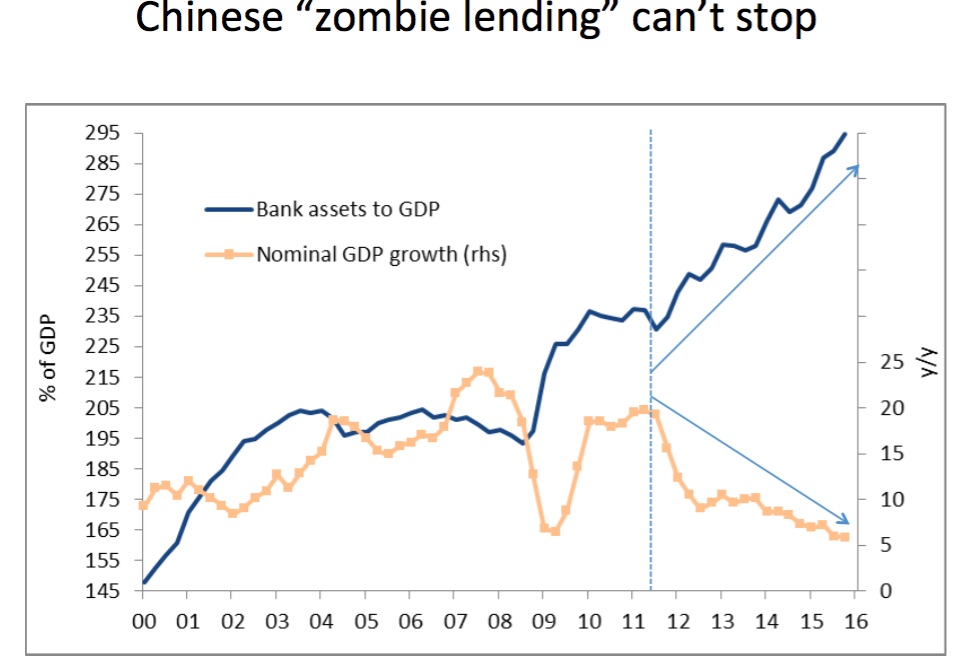

„In response to the global financial crisis, China embarked on a $4 trillion stimulus program. (…) this only aggravated the overcapacity in the investment side of their economy. Not surprisingly, this only provided a short term pop in nominal growth. While we were worried about bank assets to GDP in 2012, incredibly, credit has increased by 70% of GDP in the 4 years since then. Just to put this in perspective, this means that since 2012 the Chinese banking sector has allowed credit to grow by the amount of the entire Brazilian GDP per year! (…) Incredibly, all this credit growth has been accompanied by a fall in nominal GDP growth from 15% to 5%.“

Quelle: Druckenmiller

„I have argued that myopic policy makers have no end game, they stumble from one short term fiscal or monetary stimulus to the next, despite overwhelming evidence that they only produce an ephemeral sugar high and grow unproductive debt that impedes long term growth. Moreover, the continued decline of global growth despite unprecedented stimulus the past decade suggests we have borrowed so much from our future for so long the chickens are coming home to roost.“

Quelle: Druckenmiller

„If we have borrowed more from our future than any time in history and markets value the future, we should be selling at a discount, not a premium to historic valuations. It is hard to avoid the comparison with 1982 when the market sold for 7x depressed earnings with dozens of rate cuts and productivity rising going forward vs. 18x inflated earnings, productivity declining and no further ammo on interest rates.“

Am Schluss empfiehlt er dann Gold.

→ Zero Hedge: Albert Edwards: „Let Me Tell You How This All Ends“, 8. Mai 2016