“What Happens When Rampant Asset Inflation Ends?”

Bekanntlich befinden wir uns seit Jahren in einem sich ausweitenden Ponzi-Schema. Die Notenbanken haben das befeuert, offiziell, um die Wirtschaft zu beleben und um das System vor dem Einsturz zu bewahren. Nun kommen die Helikopter, wie schon oft bei bto diskutiert. Wie weit wir es getrieben haben, zeigen diese Charts:

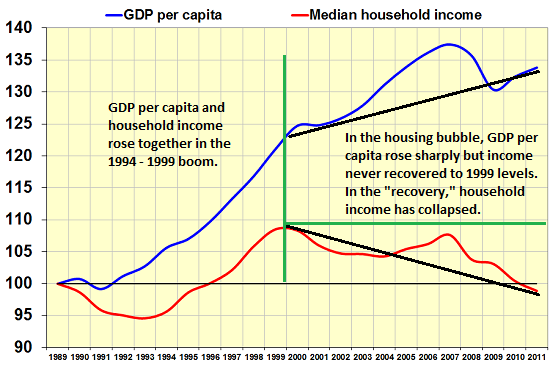

- “In effect, central banks and states have masked the devastating stagnation of real income by encouraging households to take on debt to augment declining income and by inflating assets via quantitative easing and lowering interest rates and bond yields to near-zero (or more recently, less than zero).”

Quelle: Zero Hedge

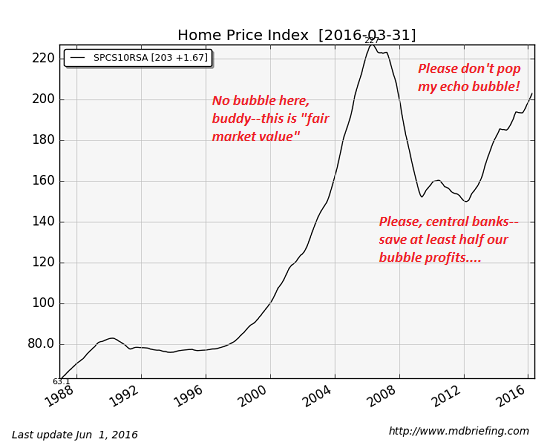

- “The ‚wealth‘ created by asset inflation generates a ‚wealth effect‘ in which credulous investors, pension fund managers, the financial media, etc. start believing the flood of new ‚wealth‘ is permanent and can be counted on to pay future incomes and claims. Asset inflation is visible in stocks, bonds and real estate. – bto: Und das führte damit zu der von Piketty und Co. bedauerten Entwicklung von Vermögen und Vermögensverteilung.

Quelle: Zero Hedge

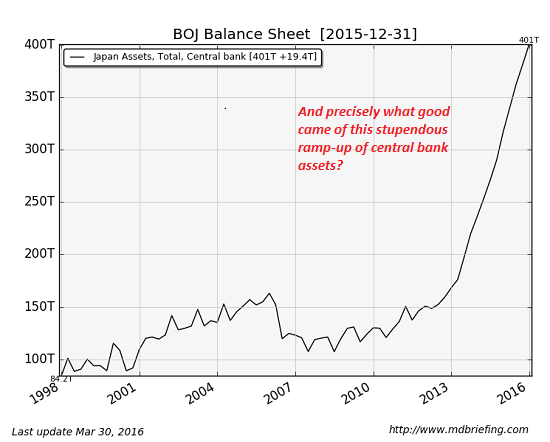

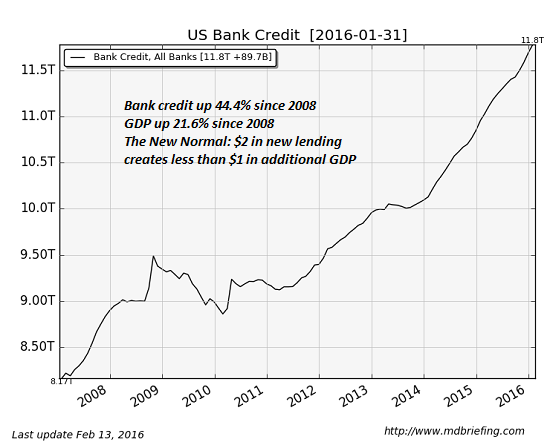

- The sources of asset inflation are highly visible: soaring central bank balance sheets, credit expansion that far outpaces GDP growth and ZIRP (zero interest rate policy). – bto: was übrigens der Realwirtschaft wirklich nichts bringt.

Quelle: Zero Hedge

- “In effect, gambling on additional future asset inflation is the only game in town. Institutional money managers are buying bonds that yield less than zero not because they’re pleased to lose money, but because they anticipate rates dropping further.”

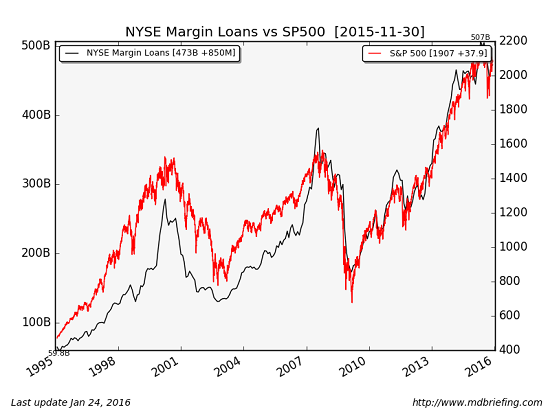

- “With the cost of borrowing less than zero once the loss of purchasing power is factored in, it makes sense to borrow money to increase speculative asset purchases to leverage up any gains from future asset inflation. Look at how margin borrowing and stock prices move in lockstep:“

Quelle: Zero Hedge

“There are only two ways to keep asset inflation alive: one is for central banks and states to buy up major chunks of all asset classes, i.e. hitting every higher bid regardless of the risks of such a strategy, and the second is to pay households to borrow money to chase future asset inflation, for example, paying households to buy a house with a mortgage.” – bto: also Helikopter-Geld.

→ Zero Hedge: “What Happens When Rampant Asset Inflation Ends?”, 4. August 2016