“The Myth Of The ‚Passive Indexing‘ Revolution”

Passive Fonds sind besser als aktive. So zumindest der breite Konsens. Ich habe verschiedentlich meine Skepsis dazu geäußert, so in meiner WirtschaftsWoche-Kolumne:

→ „Von Schafen und Wölfen“

Heute etwas eher Grafisches zum Thema passive Fonds statt aktiver Fonds von Zero Hedge.

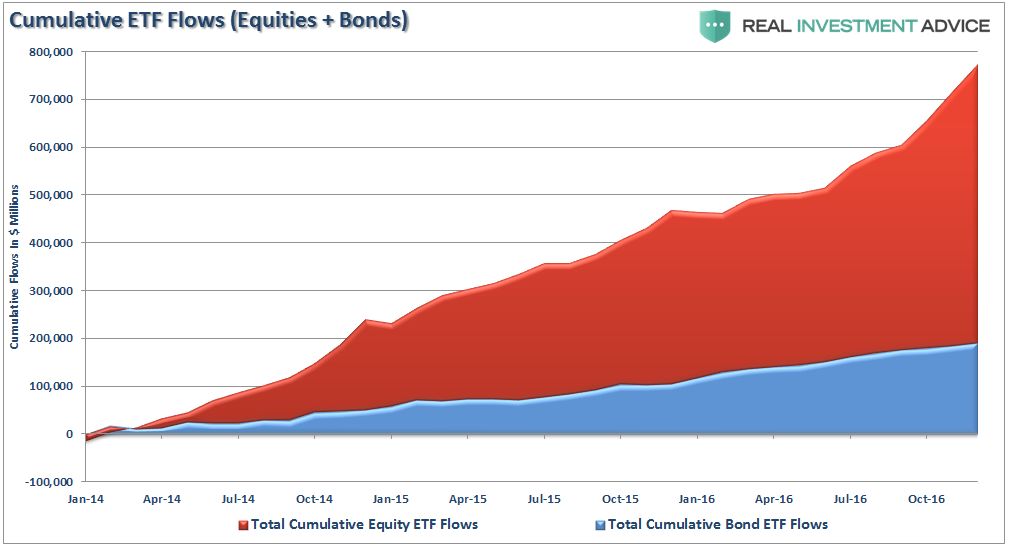

Zunächst die Feststellung, dass Indexfonds boomen:

Quelle: Zero Hedge

Danach die Zusammenfassung der Gründe:

- “Expenses: The management fees on passive funds are extremely low as the funds do not require investment analysis. In fact, an excel spreadsheet with a few lines of macro coding can replace a traditional portfolio manager. The WSJ article found that fees are almost eight times higher for active funds than passive ones (.77% vs. .10%).” – bto: weshalb nach Kosten fast alle aktiven Manager underperformen.

- “Relative Performance: Not surprisingly, in a market that has been fueled by massive Central Bank interventions, passive funds have outperformed actively managed funds. In the aforementioned article, the WSJ found that over the last five years a meager 11.2% of U.S. large-company mutual funds (actively managed) outperformed the Vanguard 500 passive index fund. Of course, this is due to expense difference as noted above.” – bto: Das macht es aus Sicht der Investoren nicht besser.

- “Technology Shifts: The advancement for algorithmic and computerized trading is leading to a migration of assets into ETF’s which are ideal for computer-driven allocation models.” – bto: Ein Computer könnte auch aktiv sein.

- “Media: One of the biggest reasons for the flows from actively managed mutual funds into ETF’s has been the increased press and media attention on ETF’s. As the markets have pushed higher, and the performance and expense differential exposed, the media has berated investors for not being invested regardless of the risk. Therefore, investors have been ‚psychologically pushed‘ to buy ETF’s as the ‚fear of missing out‘ has accelerated.” – bto: naja. Die Medien berichten jedoch etwas, das faktisch stimmt, siehe Punkte 1 bis 3.

bto: Ein Effekt ist jedoch, dass die Märkte damit immer anfälliger für Herdenverhalten werden, was ich auch bei bto und in der WiWo-Kolumne besprochen habe.

Dann machen die Autoren eine wichtige Unterscheidung: “Passiv” ist nämlich nicht passiv: “Today, more than ever, advisors are actively migrating portfolio management to the use of ETF’s for either some, if not all, of the asset allocation equation. However, they are NOT doing it ‚passively‘. For example, in our own portfolio management practice, we offer an entirely ETF driven asset allocation model which is actively managed against the variety of ‚risks‘ that arise from asset rotation to inflation, interest rate risks, momentum shifts and inter-market analysis.” – bto: Man managt also sehr wohl aktiv, aber eben auf Assetklassen-Ebene und nicht mehr innerhalb der Assetklassen: “(…) all indexing approaches aren’t all that ‚passive‘. They’re just different forms of active management that have been sold to investors using clever marketing terminology like ‚factor investing‘ and ‚smart beta‘ in order to differentiate the brands.“

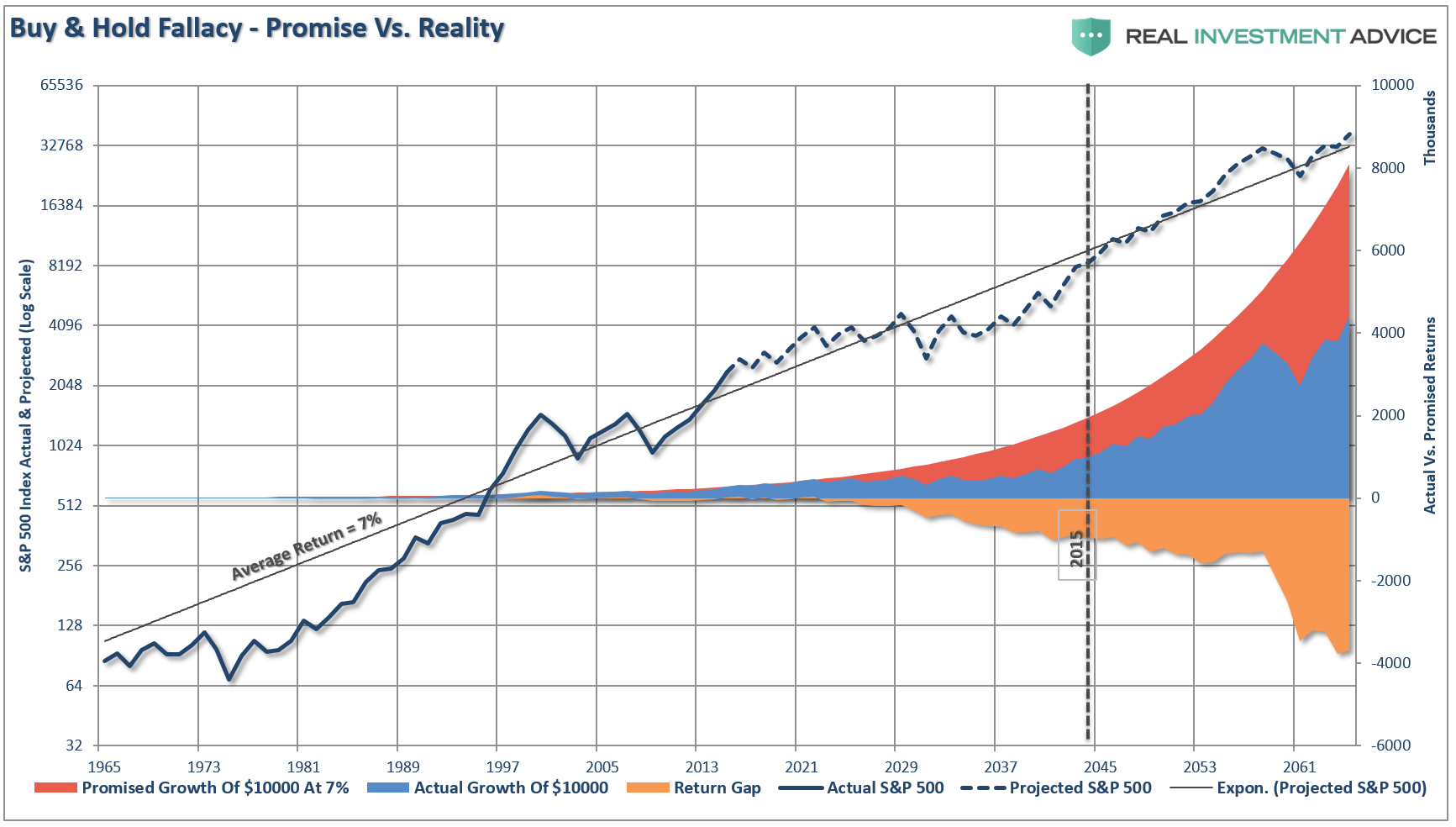

- “The idea of ‚passive‘ investing is ‚romantic‘ in nature. It’s a world where everyone just invests some money, the markets rise 7% annually and everyone one’s a winner. Unfortunately, the markets simply don’t function that way:”

Quelle: Zero Hedge

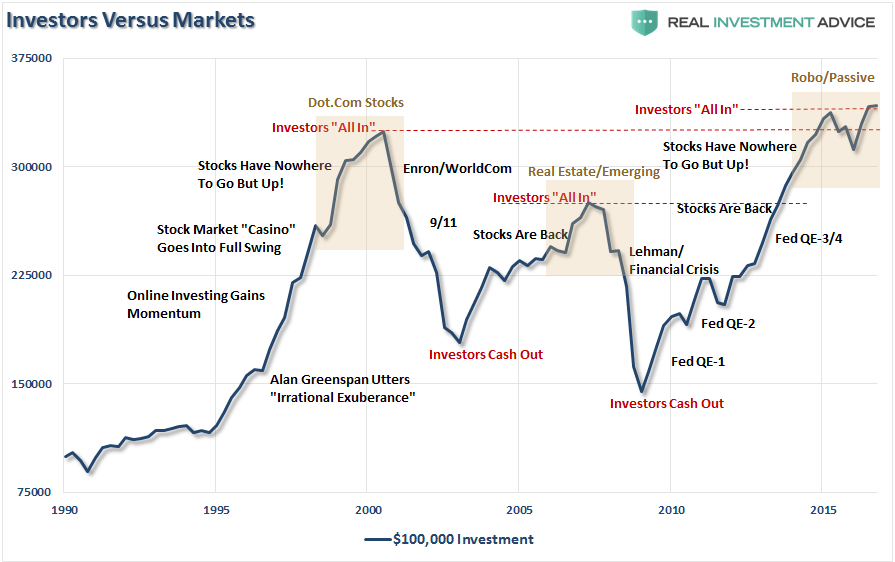

- “‚Embracing passive investing is exactly this sort of >cover your eyes and buy< sort of attitude. Would you embrace the very same price-insensitive approach in buying a car? A house? Your groceries? Your clothes? Of course not. We are all very price-sensitive when it comes to these things. So why should investing be any different?‘“

Quelle: Zero Hedge

- Und weiter: “The problem is that once prices begin to fall the previously ‚passive indexer‘ becomes an ‚active panic seller‘.” – bto: Und wie das stimmt!

Fazit von Zero Hedge: “Just remember, everyone is ‚passive‘ until the selling begins.” – bto: Da muss ich nichts mehr hinzufügen.

→ Zero Hedge: “The Myth Of The ‚Passive Indexing‘ Revolution”, 23. Januar 2017