China steht auch hinter dem Weinboom

Bekanntlich halte ich wenig von Kunst, Uhren, Wein und Oldtimern für die Geldanlage. Kunst mag für den einen oder anderen aus Erbschaftssteuergründen attraktiv sein, unter Renditegesichtspunkten ist es das nicht. Zumindest wenn man nicht das Glück hat, auf das richtige Pferd zu setzen: → Lieber trinken

Hinter dem Boom steht übrigens wieder China. Was angesichts der Probleme in dem Land potenziell zu einem echten Thema auch für diese Märkte werden könnte, wenn es das noch nicht ist. Die FT berichtet:

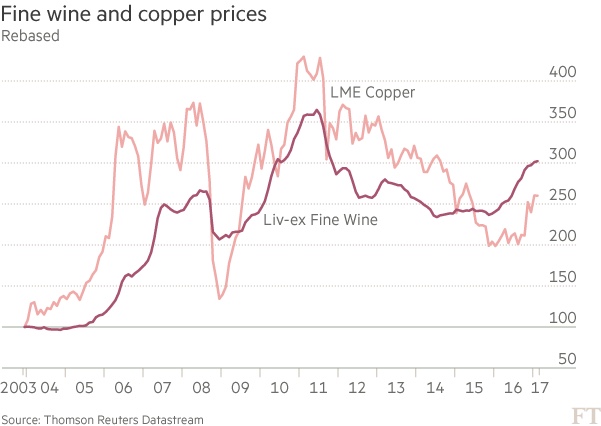

- “As the cognoscenti flock to Bordeaux next month for the first tasting of wine from the most recent harvest, they could do worse than consult Dr Copper on the outlook for the fine wine market.” (…) [Kupfer und Rotwein] “share a key characteristic: they are affected by the liquidity in the Chinese economy“. – bto: wie übrigens auch die Immobilienmärkte von Vancouver bis London.

- “China is the biggest consumer of copper, (…) also among the top five wine importers, the world’s largest consumer of red wine and the top buyer of Bordeaux reds.” – bto: Wer also damit spekuliert, setzt in Wahrheit auf die chinesische (Schulden-)Wirtschaft.

- “Both the copper price and the Liv-ex 100 Fine Wine index, which reflects the movements of 100 of the most sought-after fine wines, the bulk of which are Bordeaux, have been moving in tandem for more than a decade and rebounded from multiyear lows in 2016.” – bto: So leicht kann es sein. Einfach auf den Kupferpreis achten.

Quelle: FINANCIAL TIMES

- “The wine market was driven by speculators based in Hong Kong (…) Fine wine and copper prices peaked in 2011, with worries about an economic slowdown in China depressing the red metal, while Beijing’s austerity campaign and clampdown on corruption led to a sharp drop in wine prices.” – bto: Sobald aber wieder gedruckt wird, ist es alles klar.

- “In a 2011 paper, IMF economists Serhan Cevik and Tahsin Saadi Sedik looked at the oil and fine wine markets, noting they had ‚shown remarkable similarity‘. ‚Fine wine prices are sensitive to macroeconomic shocks, just like crude oil and other commodity prices,‘ they said.” – bto: Es ist auch ein spezieller und (relativ) kleiner Markt.

- “(…) both markets are sending positive signals on China. Copper is up 6 per cent this year and the broad consensus is for it to add to those gains. (…) a recent survey of Liv-ex members shows they expect the fine wine market to rise a further 8 per cent in 2017. Investors in both markets will be tempted to monitor the action in the other. Anyone interested in China will keep an eye on both.” – bto: Und das sollten wir alle sein!

bto: so viel zum „krisensicheren“ Investment in alternative Anlagen.

→ FT (Anmeldung erforderlich): “Fine wine and copper bound by China link”, 22. März 2017